Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

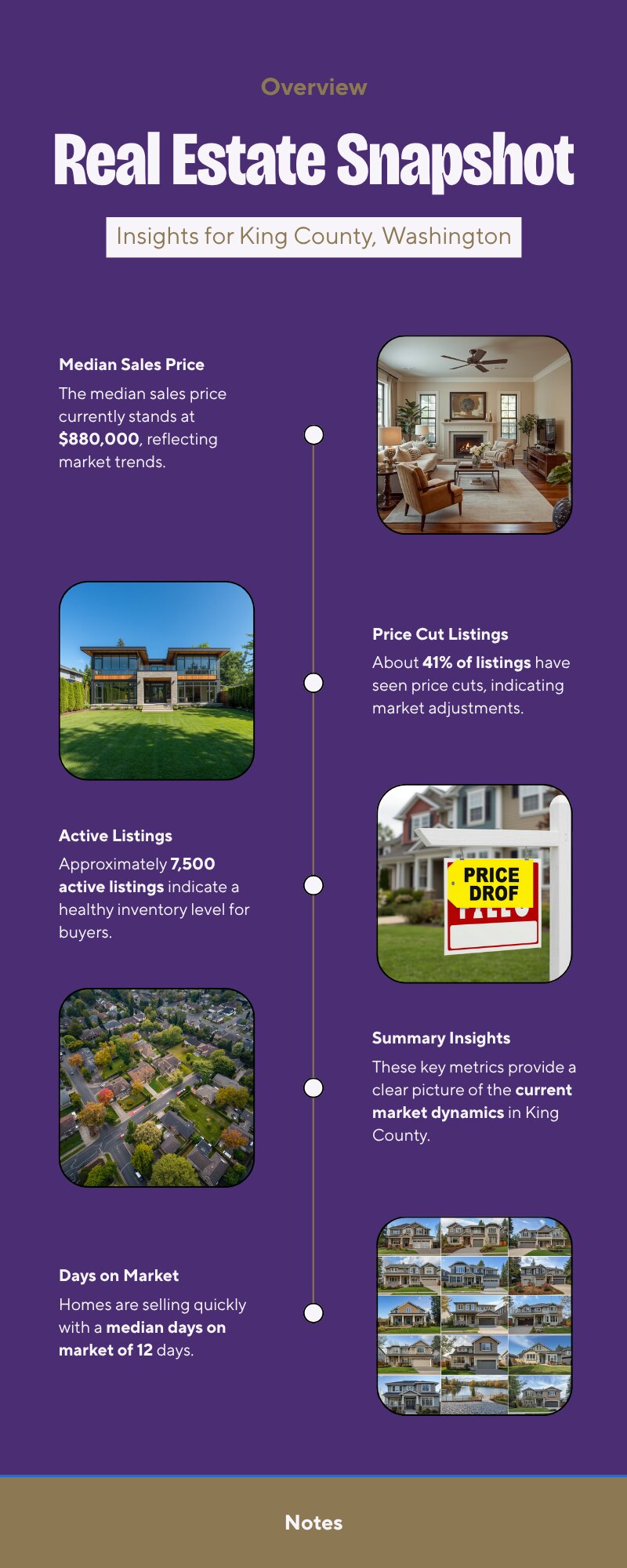

41% of Renton Sellers Just Cut Their Price. Here’s What That Means for You.

South King County buyers finally have leverage — and most sellers don’t know it yet.

The number that caught my attention this week was 41%. That’s the share of active listings in Renton where sellers have reduced their price in the last 14 days. Nearly half. In a market where the median home still sells in 12 days and buyers are committing at full asking price on average, that gap tells a very specific story — and it’s one worth understanding before you make your next move.

This is not a market in freefall. King County is still a seller-leaning balanced market. But the sellers who are winning right now are the ones who priced with current data from day one. The ones who guessed — or who are still thinking it’s 2022 — are the ones cutting their prices two weeks in. That divergence is the story of this week’s market, and it matters whether you’re buying or selling.

Here’s what the data is showing across King County this week.

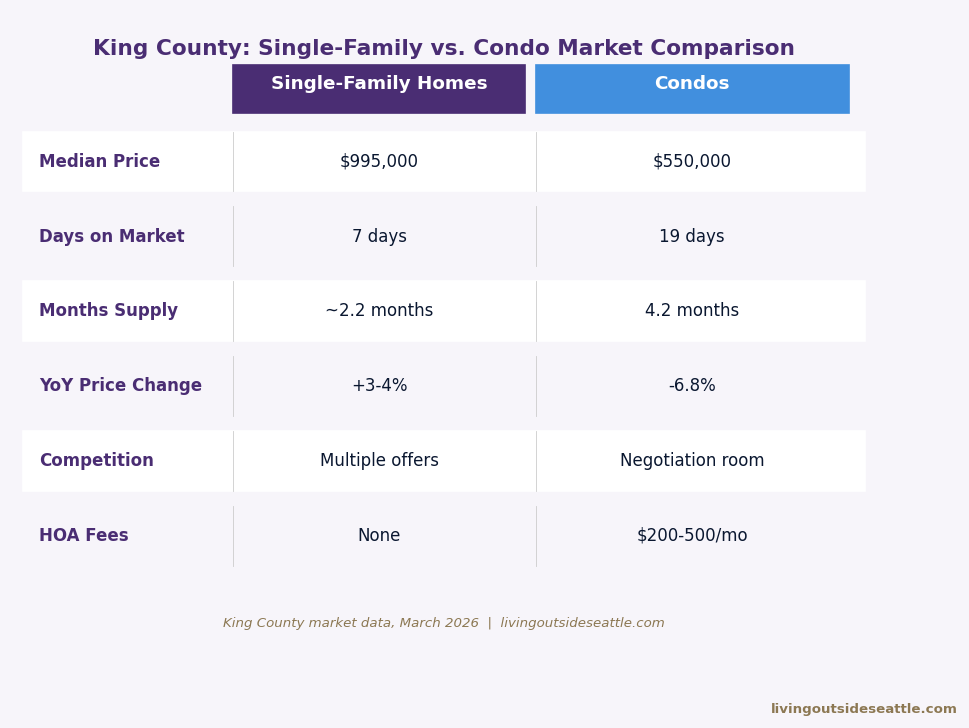

The Big Picture: King County at a Glance

The county-level numbers are holding steady. Inventory has plateaued after the big spring surge, mortgage rates have been stable, and homes are still moving — just more selectively than before.

Source: NWMLS | May 2026

The 12-day median days on market tells you demand is still real. But the price reduction number tells you that demand has a sharp edge — it shows up fast for homes that are priced right, and it stays away entirely from homes that are not. That split is wider right now than it has been in years.

Mortgage rates have held a tight band between 6.0% and 6.3% all month. That’s not exciting news, but it’s actually good news for anyone trying to plan. Buyers know what their payment will be. Sellers know what their buyer pool looks like. Predictability at 6% is a lot more useful than volatility at 5.5%. If you want to understand what rates are actually doing to purchasing power right now, I broke that down in detail in my King County mortgage rates guide for 2026.

Neighborhood Breakdown

Renton

Renton is the clearest example of the price-drop divergence playing out in real time. The median price is holding at $788,000, but that number masks what’s happening beneath it. Over 41% of active listings have cut their prices in the past two weeks. That’s not a sign of a collapsing market — it’s a sign that a lot of sellers came in hot and the market pushed back.

For buyers, this is exactly the kind of data that creates real negotiating room. If you’re looking in Renton and a home has been sitting for more than two weeks, there’s a real chance that seller is ready to talk. If you’re a seller in Renton and you haven’t listed yet, this data tells you one thing clearly: price it right on day one, or join the 41%.

If you’re thinking about listing in Renton this spring, I put together a detailed breakdown of when and how to sell in Renton that’s worth reading before you set your number.

Source: NWMLS | May 2026

Kent

Kent’s median price sits at $695,000 with healthy active inventory. Homes that aren’t staged or priced strictly to current comps are sliding past the 30-day mark quickly. That’s a meaningful threshold — once a home hits 30 days on market, buyers start wondering what’s wrong with it even when nothing is.

The buyers who are winning in Kent right now are the ones who have done their homework and know what the real comps support. If you’re a first-time buyer trying to figure out whether now is the right time to buy in Kent, I worked through the actual math in this post: First-Time Home Buyer in Kent WA — Buy Now or Wait?

Federal Way & Auburn

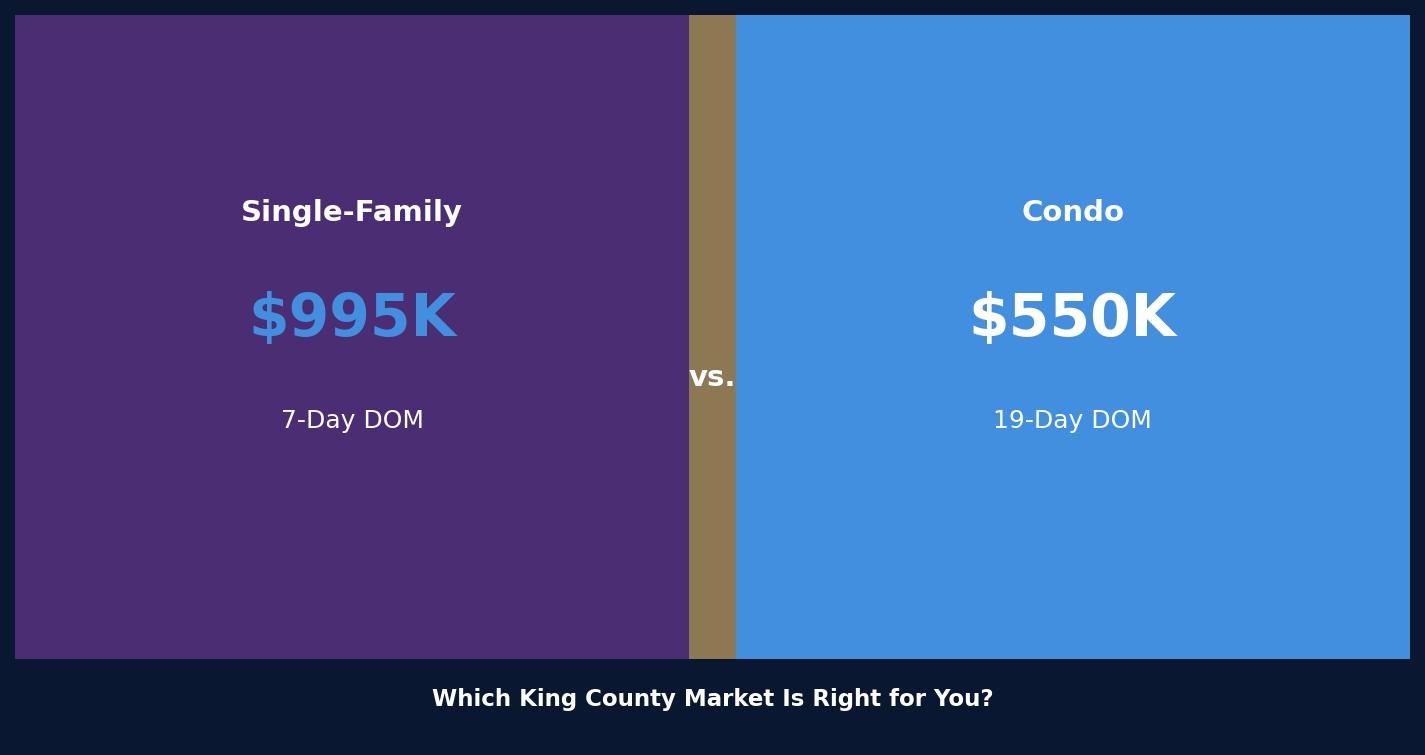

These two cities are carrying a lot of buyer traffic right now, and for good reason. Federal Way is holding 8.9% year-over-year price growth with a $615,000 median. Auburn is running competitive under $650,000, with well-priced homes moving in about 10 days. The flight to affordability south of Seattle is far from over — these cities are absorbing buyers who got priced out of Renton and Kent, and the demand is showing up in the numbers.

For first-time buyers, this is where your dollar goes furthest in King County right now. For sellers in Federal Way and Auburn, the traffic is real — but so is the competition. Presentation and pricing still decide everything.

The Eastside: Bellevue, Sammamish & Issaquah

The Eastside continues to move at a different speed. Bellevue’s turnkey homes under $2 million are averaging 6 days on market, driven in large part by the OpenAI expansion pulling in high-income relocating buyers. Sammamish sits at a $1.62 million median and remains your lowest-inventory Eastside market — move-in-ready homes there are still vanishing in 5 days. Issaquah is running around $904,000 median with strong showing activity, particularly in the Issaquah Highlands.

If you’re tracking luxury inventory, the one note is that Bellevue homes over $3 million are starting to accumulate. High-end buyers there are getting more options than they’ve seen in a while.

What This Means If You’re Buying

The market right now rewards buyers who are prepared. Here’s what that looks like in practice.

In South King County, especially Renton and Kent, the price reduction data is telling you something important: there is negotiating room on a meaningful number of active listings. If a home has been sitting for two weeks or more and carries a price cut, that seller has already signaled they are willing to move. Going in with a well-supported offer below asking is not aggressive — it’s logical, and the data backs it up.

Rate stability at 6.0–6.3% also gives you something buyers haven’t had for a while: the ability to plan. You can calculate your actual payment with confidence right now. That predictability is a tool — use it. Lock your pre-approval, know your number, and be ready to move when the right home comes up.

What This Means If You’re Selling

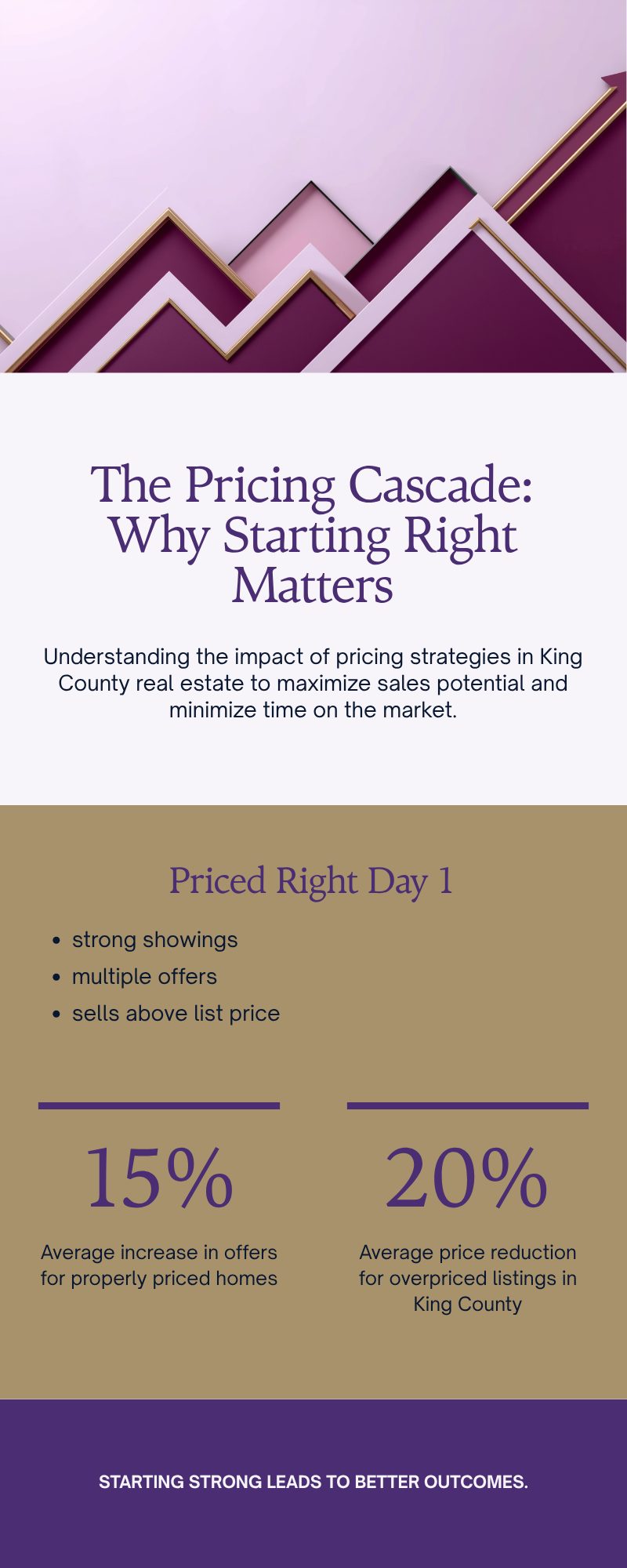

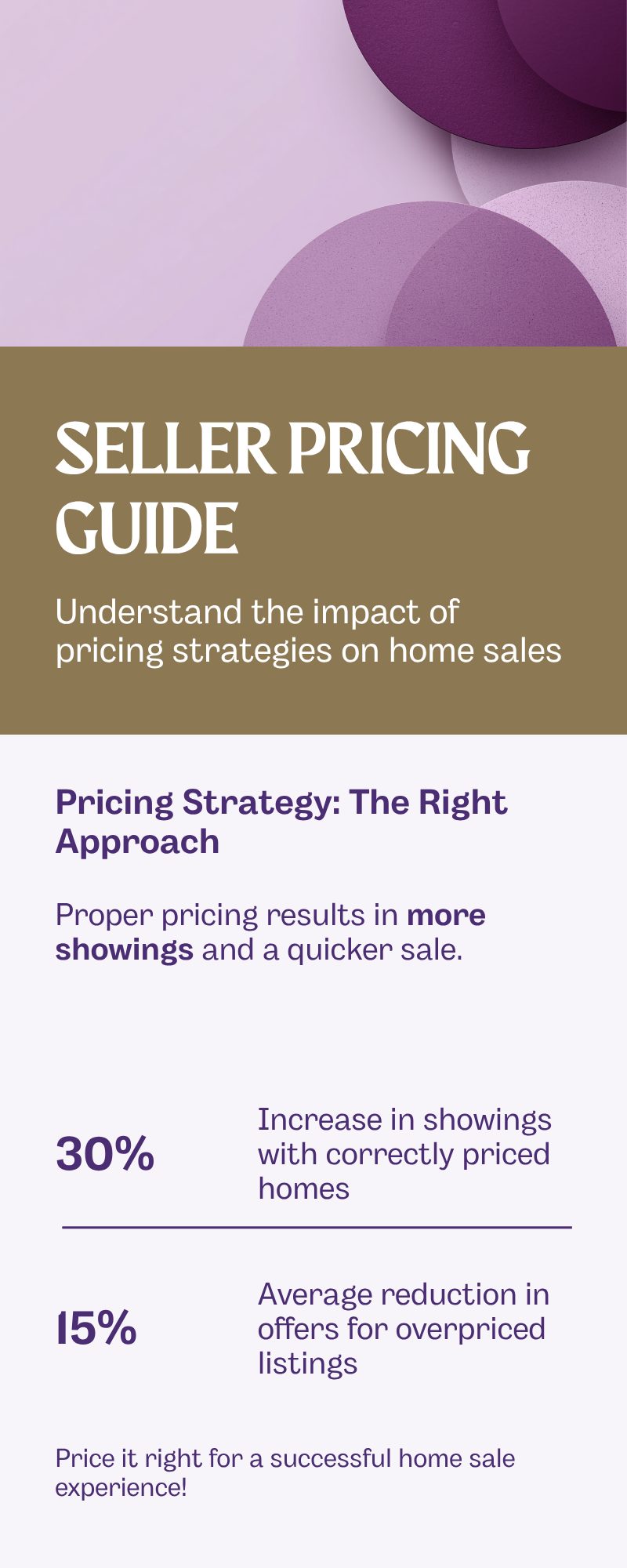

If you are thinking about listing, the most important thing I can tell you this week is this: the market will give you a fast, clean sale — but only if you price for 2026, not 2022.

The homes in the top 10% of the market right now — turnkey, well-staged, priced to current comps — are still getting multiple offers. The homes with minor deferred maintenance or aggressive pricing are sitting and collecting price cuts. There is almost no middle ground this week.

Staging and pricing from day one are the two decisions that separate fast sales from price cuts right now.

Staging matters more than it did two years ago. When buyers have more choices than they did in 2022, the bar for “good enough” goes up. A home that might have gone under contract in a weekend in 2022 now needs to actually compete.

If you’re not sure how to find your real number in this market, I put together a full breakdown of how to price your home to sell in King County in 2026. It covers exactly what the comps process looks like and where most sellers make the mistake.

The BPO Advantage

Here’s why this specific market moment makes pricing precision so critical.

Right now, 4 out of 10 sellers in South King County guessed wrong on price. They listed, sat, and cut. Every day a home sits on market, it loses negotiating leverage. Buyers start asking what’s wrong with it. The final sale price ends up lower than it would have been on day one with the right number.

My BPO work — professionally assessing property values for banks and lenders every single day — means I don’t guess. I know what the banks think a home is worth because I run those same calculations constantly. When I tell you what your home should list at, it’s not an opinion built on what you hope to net. It’s an institutional-grade assessment built on the same methodology that lenders use to protect their money.

Institutional-grade pricing analysis — the same methodology banks and lenders use.

In a market where the difference between a week-one sale and a 30-day price cut can be $20,000 to $40,000, that kind of precision isn’t a nice-to-have. It’s the job.

What to Watch Next Week

Keep an eye on how the 41% price reduction figure moves in South County. If it climbs toward 50%, that’s a signal that the buyer pool is thinning in Renton and Kent and sellers will need to adjust more aggressively. If it starts coming back down, it means the market is self-correcting and properly priced homes are getting absorbed.

The rate window at 6.0–6.3% has been unusually stable. Any movement in bond markets could shift that, so if you’re a buyer who has been waiting for the right moment to lock a pre-approval, this week is as good a moment as you’ve had all spring.

Your guide to life outside Seattle.

253-350-0045 ·

greg@livingoutsideseattle.com ·

www.livingoutsideseattle.com