Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

First-Time Home Buyer in Kent WA: Buy Now or Wait?

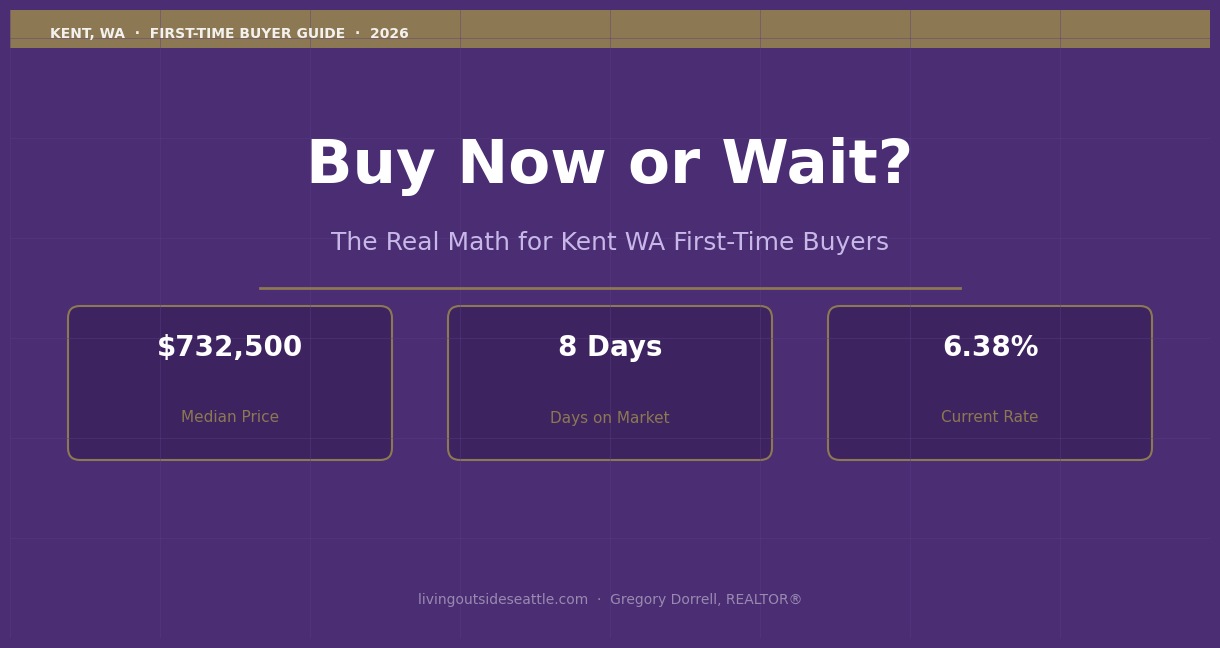

This is the conversation I’m having with nearly every first-time home buyer in Kent, WA right now. The mortgage rate is 6.38 percent as of late March 2026, which is high enough to sting but not high enough to stop you from buying. Should you go in now and refinance later when rates drop, or should you wait?

Let me walk you through the actual math, because the answer isn’t as obvious as it sounds.

Kent WA Housing Market: What First-Time Buyers Face Right Now

Kent is one of the most affordable single-family home markets in our region right now. In March 2026, the median sale price was $732,500 with a median days on market of 8 days. That DOM gives you breathing room, but not endless time. It’s the sweet spot where you can be thoughtful without leaving money on the table.

If you’re a first-time buyer looking at Kent, you’re probably looking at a mortgage in the $650,000-$800,000 range. At 6.38 percent, that’s a real monthly payment to think about.

So the question becomes: should you lock in now and hope rates drop so you can refinance, or should you wait and see what rates do?

The answer depends on five things: refinancing costs, break-even timeframe, price appreciation, how long you plan to stay, and your financial stress tolerance.

How Much Does It Cost to Refinance in Washington State?

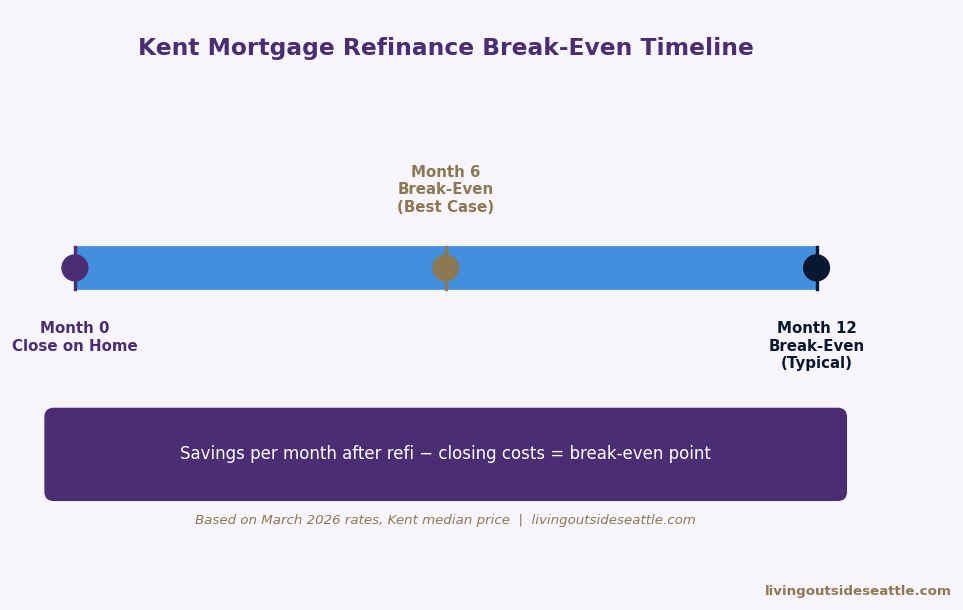

Refinancing isn’t free. When you refinance, you pay closing costs again. These typically run $3,000-$5,000 depending on loan amount, lender, and your credit profile. Some of that cost gets rolled into the new loan, but you’re still out of pocket for some portion upfront.

Let’s say you buy a $732,500 home now at 6.38 percent with a 30-year mortgage. Your principal and interest payment is roughly $4,430 per month. Your property tax, insurance, and HOA (if any) add another $800-$1,200 depending on neighborhood.

If rates dropped to 5.38 percent, your new principal and interest payment would be roughly $3,970 per month. That’s a savings of about $460 per month.

Here’s where it gets real: it takes you about 6-7 months of that $460 monthly savings to break even on $3,000-$3,500 in refinancing costs. If you stay in the home for 2+ years, you’re always ahead by refinancing. If rates only drop to 5.88 percent, your break-even stretches to 10-12 months.

The key variable is how far rates actually drop. A 1-percentage-point drop makes sense. A 0.5-percentage-point drop takes longer to break even. More than 1 point is great, but nobody knows if that happens.

Does Kent Home Price Appreciation Change the Buy-Now Math?

Here’s what many people miss: the monthly payment math ignores price appreciation. If you wait and prices appreciate while you’re sitting on the sidelines, that price gain might exceed what you save on interest rate reduction.

In Kent specifically, I’ve evaluated hundreds of properties across the market as a BPO field inspector. What I see is that Kent’s price-per-square-foot has stayed relatively stable compared to higher-priced markets like Sammamish or Bellevue. That stability is good for your peace of mind but suggests modest appreciation, not explosive growth.

Let’s run a scenario. If Kent median prices appreciate 3 percent annually, that $732,500 home is worth $754,675 in a year. You’ve built $22,175 in equity through price appreciation alone (assuming you put 10 percent down and financed $659,250).

If you waited and refinanced from 6.38 percent to 5.38 percent after a one-year delay, you’d save $460 per month for the remaining 29 years of the loan, which is roughly $160,000 in total interest savings. But you lost out on the $22,175 in price appreciation equity you could have built by owning for that year.

The math gets complex fast. The point is that waiting isn’t free, either.

Will Mortgage Rates Drop in 2026? What Kent Buyers Should Know

Let me be honest: nobody knows where rates go from here. I’m looking at a 30-year fixed at 6.38 percent in late March 2026, up 40 basis points in just four weeks due to Middle East tensions and oil price volatility. That’s how unpredictable the environment is.

Rates could drop. They could stay stable. They could move higher. Betting your purchase decision on a rate forecast is a bet I wouldn’t make. Betting your purchase decision on affordability, neighborhood, and your life circumstances makes more sense.

Why Kent WA Is Still a Strong Market for First-Time Buyers

As a first-time buyer, you’re probably not in a position to wait indefinitely. You might be ready to move for a job, growing out of an apartment, or just tired of renting and building equity for someone else.

Kent is a solid first-time buyer market because it’s affordable relative to higher-priced East King County alternatives, it has decent schools, and it has real community character. Homes are priced in a range where a $75,000-$100,000 down payment (if you’ve saved that) gives you real traction.

Kent first-time buyers also have access to Washington State Housing Finance Commission programs — including Home Advantage, which offers down payment assistance that can meaningfully reduce the upfront cost. first-time buyer programs Washington state These programs don’t eliminate the rate question, but they do change the affordability math enough to be worth knowing about before you assume ownership is out of reach.

The timing question isn’t as important as the fundamentals question: is this the right home for me in the right neighborhood at a price I can afford and sustain?

Buy Now or Wait in Kent WA: The Decision Framework

If you can afford the 6.38 percent rate and a refinance in a few years won’t stress you financially, buy now. You lock in price certainty, you start building equity immediately, and you get the benefit of owning the home you actually want instead of waiting for a hypothetical rate drop.

If rates drop significantly (1+ percentage point), you refinance and you’re ahead. If rates stay flat or move higher, you’re still in a home in Kent that you wanted to be in. The worst case is rates drop modestly (0.25-0.5 percent), your break-even timeline gets longer, and you live in a home you like while waiting for that refinance window to open. That’s not a tragedy.

If you can’t afford the 6.38 percent rate right now and you’re counting on a refinance to make the numbers work, wait. Don’t overextend yourself on the assumption that rates drop. That’s how people get into trouble.

If you’re genuinely uncertain whether you want to stay in Kent for 2+ years, or if your job situation is volatile, wait. Refinancing assumes you stay in the home long enough for the savings to matter.

Kent WA Real Estate Market Advantages for First-Time Buyers

The 8-day DOM means you don’t have to rush, but you also don’t have months and months to deliberate. There’s real inventory (homes actively for sale), which means you have choices. That’s good for a buyer. You can be selective about neighborhood, condition, and price without feeling like you’re leaving deals on the table.

Homes in Kent that are priced right and in good condition are still moving fast. That tells me that buyers see value in the market right now, and that value is real.

Frequently Asked Questions: First-Time Home Buyers in Kent WA

What is the median home price in Kent WA in 2026?

As of March 2026, the median single-family home price in Kent, Washington is $732,500. The median days on market is 8 days, slightly longer than the King County average of 7 days, giving first-time buyers a bit more time to make decisions without losing competitive homes.

Should I buy a house now or wait for mortgage rates to drop?

If you can comfortably afford the current payment at 6.38% and plan to stay in the home 2+ years, buying now in Kent gives you immediate equity building and price certainty. If rates drop 1 percentage point or more, you can refinance — and with a $700K loan, that saves roughly $460/month after a break-even period of 6-12 months. If you can’t afford the current rate, waiting is smarter than overextending.

How much does it cost to refinance a mortgage in Washington state?

Refinancing in Washington state typically costs $3,000-$5,000 in closing costs depending on loan size, lender, and your credit profile. Some lenders offer “no-cost” refinances that roll fees into the rate. The break-even point — when your monthly savings exceed what you paid in closing costs — is typically 6-12 months for a 1-percentage-point rate drop.

Are there first-time buyer programs available in Kent WA?

Yes. The Washington State Housing Finance Commission (WSHFC) offers the Home Advantage program, which provides down payment assistance and competitive first mortgage rates for qualifying buyers. Some programs allow down payments as low as 3-5%. Talk to a lender about income limits and qualification requirements before assuming you don’t qualify.

Your guide to life outside Seattle.

253-350-0045 ·

greg@livingoutsideseattle.com ·

www.livingoutsideseattle.com

Gregory Dorrell is a REALTOR® with Coldwell Banker Bain specializing in East and South King County real estate. This content is for informational purposes and does not constitute professional real estate, financial, or mortgage advice. Consult with your lender, financial advisor, and a licensed professional before making real estate decisions.