Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

What Is a Mortgage Rate Buydown? A King County Buyer’s Guide

You’ve probably seen it in listings: “Seller offering 2-1 rate buydown.” Most buyers scroll past it without fully understanding what it means. That’s a mistake, especially in a King County market where 6.38% is the going rate and every monthly dollar matters.

A rate buydown is one of the most useful negotiating tools available right now. Here’s how it works, what it actually costs, and when you should ask for one.

What a Mortgage Rate Buydown Actually Is

A buydown is a way to reduce your mortgage interest rate, either for a set period or permanently, by paying money upfront. Think of it as prepaying interest now to lower your payment later.

There are two main types.

A temporary buydown reduces your rate for the first one, two, or three years of the loan, then steps back up to the full rate. The most common version is the 2-1 buydown. A permanent buydown, often called paying “points,” reduces your rate for the entire life of the loan in exchange for a lump sum at closing.

Right now in King County, the 2-1 buydown is the version worth understanding because it’s the one sellers are offering.

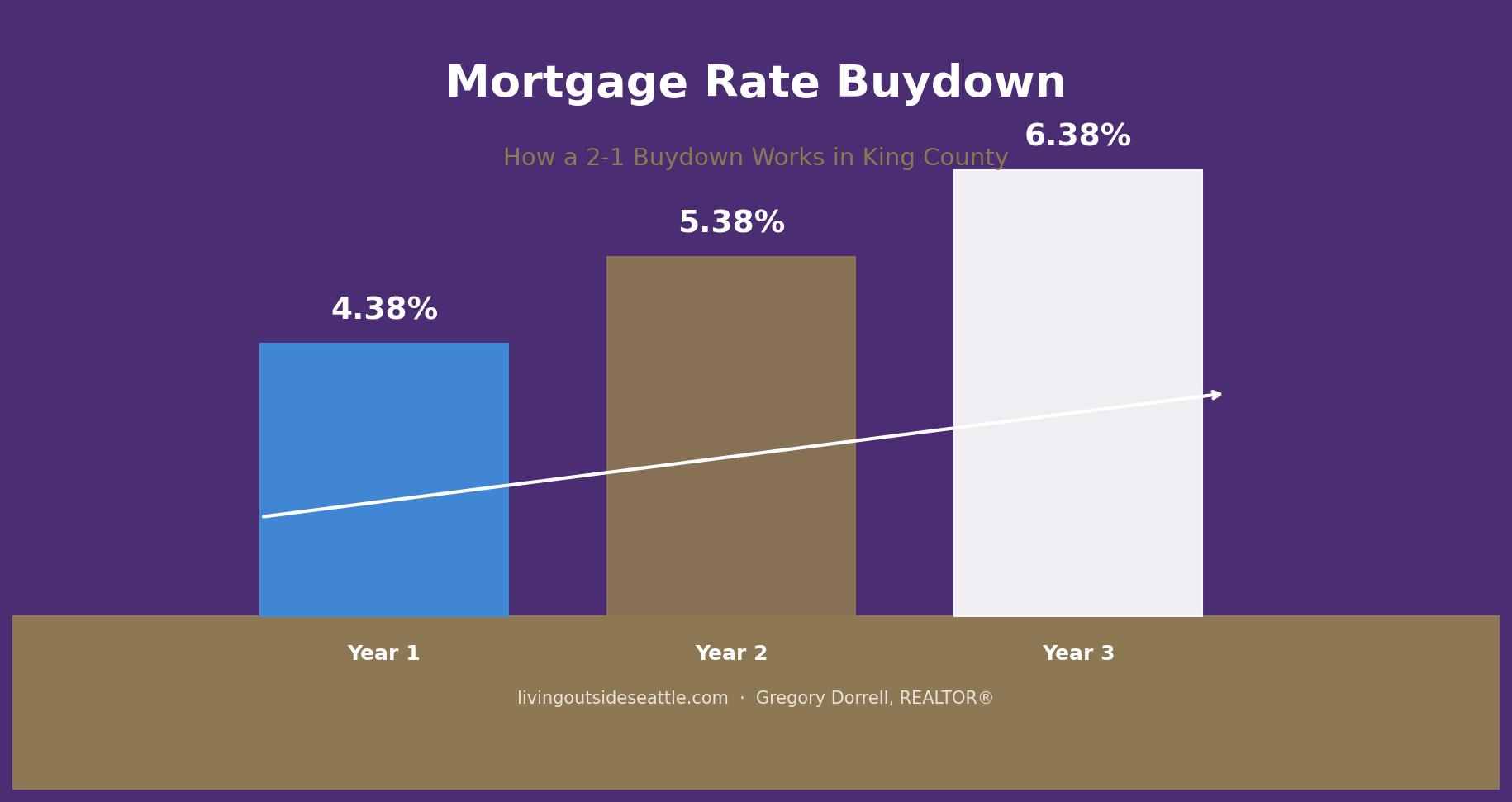

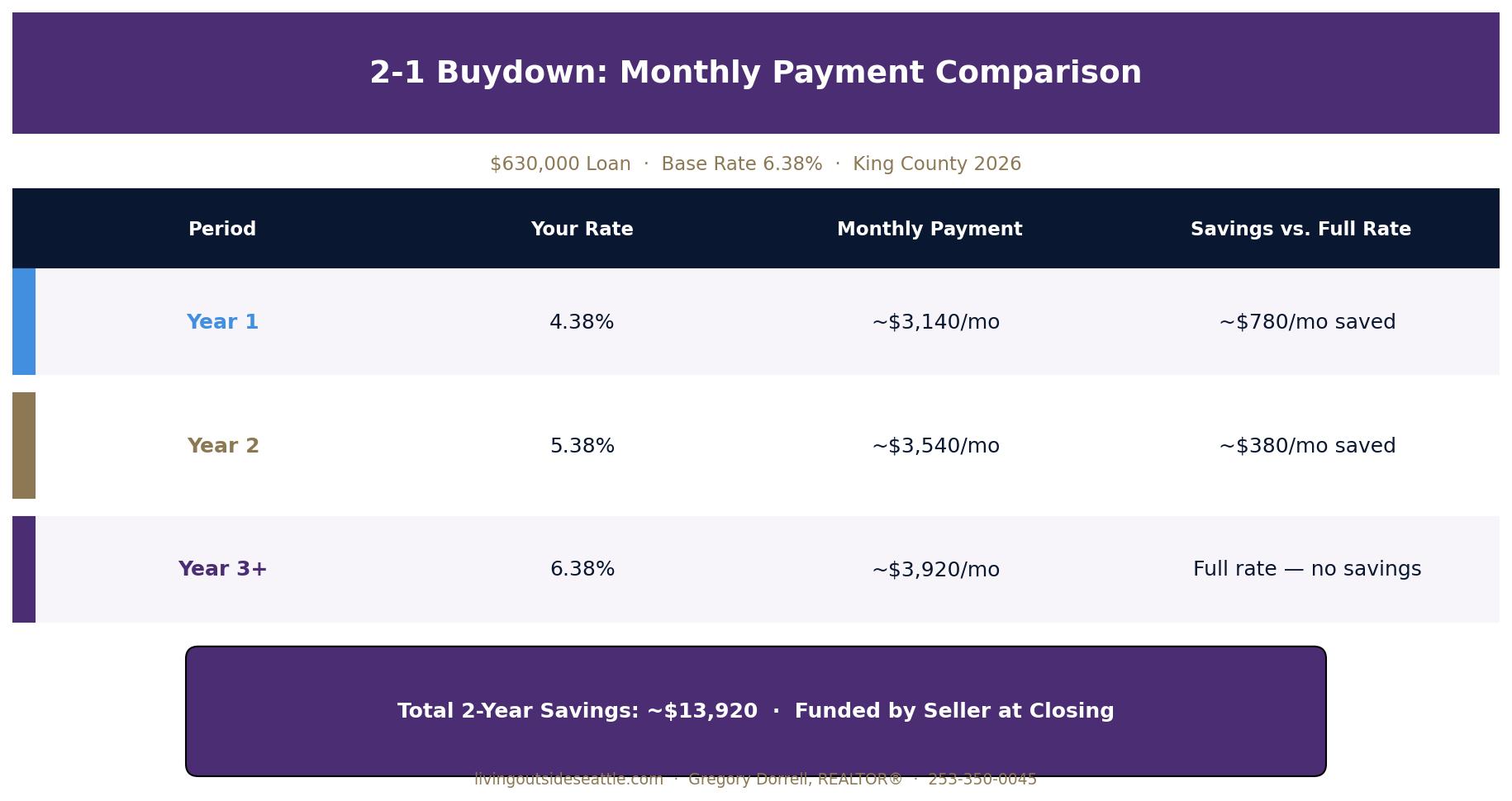

How the 2-1 Buydown Works: The Real Numbers

The “2-1” refers to the rate reduction in each year. On a 6.38% base rate:

| Year | Your Rate | Payment on $630K Loan | Savings vs. Full Rate |

|---|---|---|---|

| Year 1 | 4.38% | ~$3,140/mo | ~$780/mo |

| Year 2 | 5.38% | ~$3,540/mo | ~$380/mo |

| Year 3+ | 6.38% | ~$3,920/mo | $0 |

Figures are approximate based on a $630,000 loan (10% down on $700,000 home) at a 6.38% base rate.

Over the first two years, that’s roughly $13,920 in payment savings on a $630,000 loan. The seller funds this difference upfront at closing, usually from their sale proceeds. You get lower payments for two years without doing anything extra.

The cost to the seller to fund a 2-1 buydown on a $630,000 loan is approximately $13,920. That’s what they’re crediting to you. It comes off their bottom line, not yours.

Temporary vs. Permanent Buydown: Which Makes More Sense?

A permanent buydown (paying points) costs roughly 1% of the loan amount per 0.25% rate reduction. On a $630,000 loan, buying your rate down from 6.38% to 6.13% costs about $6,300. To 5.88% costs $12,600. The rate stays lower for 30 years, so if you keep the loan long enough, it pays off.

The break-even math matters here. I run this analysis for clients regularly. If you pay $6,300 to save $95 per month, you break even in about 66 months, just over five years. If you plan to stay longer than that, a permanent buydown pencils out. If you think you’ll refinance when rates drop, a temporary buydown often makes more sense since you get the near-term relief without the permanent cost.

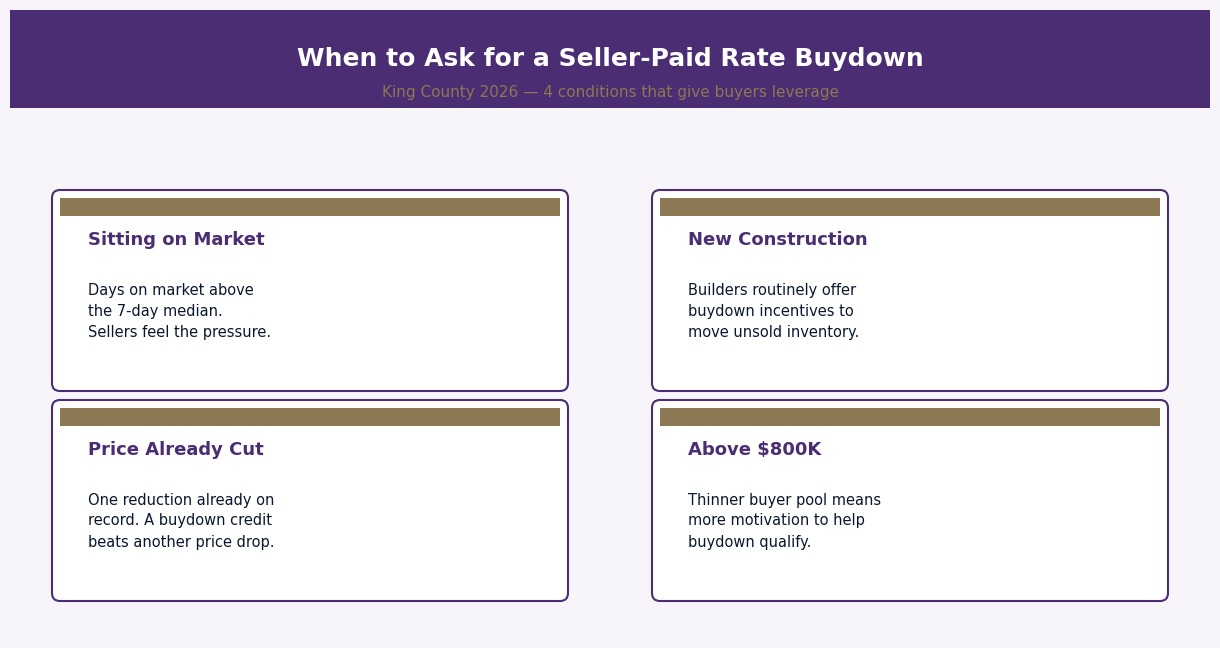

When to Ask for a Seller-Paid Buydown

Not every seller will offer a buydown, and not every market gives you the leverage to ask. Here’s when the conditions are right.

King County had 5,071 homes for sale in March 2026, up 37.5% year-over-year. Monthly supply sits at 2.2 months for single-family homes. That’s still a seller’s market, but it’s softer than it was. With inventory rising and buyer pools shrinking due to rate pressure, sellers have more motivation to help buyers qualify than they did two years ago.

The best candidates for a seller-paid buydown are homes that have been sitting on market longer than the median 7 days, new construction where builders frequently offer incentives, and price ranges above $800,000 where the buyer pool is thinner. If a seller has reduced their price once already, they may prefer a buydown credit over another price cut since it helps more buyers qualify without lowering the headline sale price.

You can also negotiate a buydown as part of a competitive offer structure. Instead of offering over asking, you offer asking price and request a seller credit toward a buydown. This can be more attractive to certain sellers who care about the sale price on paper.

What a Buydown Cannot Do

A buydown lowers your payment, but it does not change your qualifying rate. Lenders qualify you at the full note rate, 6.38% in this example, not the reduced Year 1 rate. This is an important distinction. If you can barely qualify at 6.38%, a 2-1 buydown makes your first two years more comfortable, but it doesn’t help you get approved. That’s a conversation to have with your lender before you start shopping.

A buydown also does not protect you if rates rise further. If rates climb to 7.5% by Year 3, your payment goes back to the 6.38% note rate regardless. You’re not getting a floating benefit; you’re getting a fixed discount on a fixed rate.

The Bottom Line for King County Buyers

If you’re purchasing in the next 60 days and the seller has any negotiating room, asking for a 2-1 buydown is worth the conversation. The worst they can say is no. The best case is $13,000 to $14,000 in payment savings during your first two years of ownership while you settle in, build equity, and wait for a refinance opportunity.

Frequently Asked Questions: Mortgage Rate Buydowns

Who pays for a 2-1 buydown?

Usually the seller, though buyers can also pay for it out of pocket or roll it into closing costs if the lender allows. In today’s King County market, seller-funded buydowns are the most common scenario. The seller provides a credit at closing that the lender holds in an escrow account and draws from each month to cover the difference between your reduced payment and the full rate payment.

What happens if I refinance during the buydown period?

The unused portion of the buydown funds is typically applied to your loan payoff at refinance. You don’t lose the money, but you do lose the future payment savings. This is why the 2-1 buydown works well in a market where refinancing is likely within a few years. You use the savings in Year 1 and Year 2, then refinance when rates drop rather than reverting to 6.38% in Year 3.

Can I use a buydown with FHA or VA loans?

Yes. Both FHA and VA loans allow temporary buydowns, including the 2-1 structure. The same mechanics apply. FHA and VA borrowers are often in the first-time buyer and lower-down-payment segments where the Year 1 payment relief makes the biggest difference in monthly cash flow.

Is a permanent buydown better than a 2-1 buydown?

It depends on how long you plan to keep the loan. Run the break-even calculation: divide the cost of buying down the rate by the monthly savings. If your break-even is 5 years and you plan to stay for 10+, the permanent buydown wins. If you expect to refinance within 3 years, the 2-1 temporary buydown makes more sense.

How much does a permanent buydown cost in King County?

One point equals 1% of the loan amount. On a $630,000 loan, one point costs $6,300 and typically reduces your rate by about 0.25%. To drop from 6.38% to 5.88% would cost approximately 2 points, or $12,600. Your lender can quote you exact pricing since rates and point costs vary daily.

Your guide to life outside Seattle.

Coldwell Banker Bain | WA License #111862

253-350-0045

·

greg@livingoutsideseattle.com

·

www.livingoutsideseattle.com

Gregory Dorrell is a licensed real estate broker (WA License #111862) with

Coldwell Banker Bain. This post is provided for informational purposes and does

not constitute financial or investment advice. Mortgage rates, buydown costs, and

lender policies vary and are subject to change. Consult with a licensed mortgage

lender for current pricing and qualification guidance.