Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

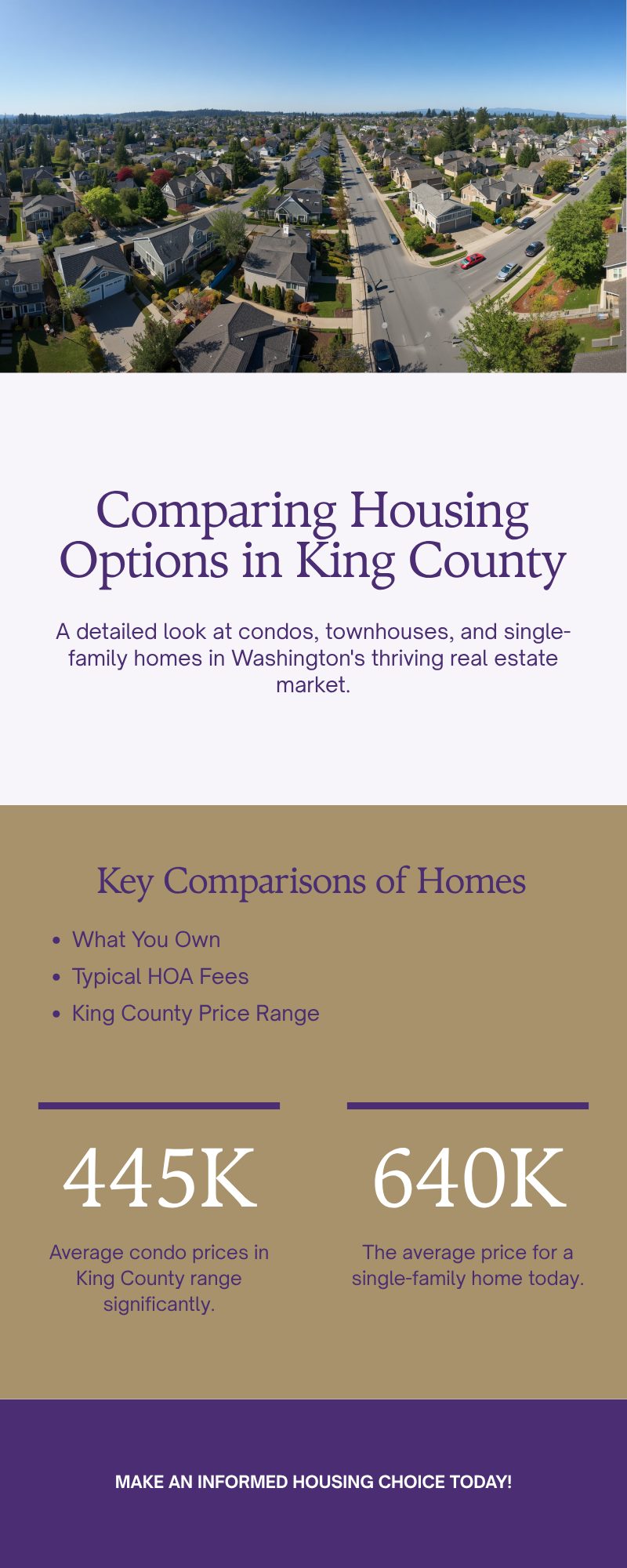

You’ve got three completely different products at three completely different price points. Here’s what actually separates them — and which one fits your situation in King County right now.

When most buyers start looking at homes in King County, they type a budget into Redfin and let the results decide the property type for them. That usually works fine until they’re deep into a transaction and suddenly discover that their condo doesn’t qualify for the loan they planned on, or that the townhouse HOA has a pending special assessment they didn’t know about.

The property type decision matters a lot more than most people realize. It affects what you pay every month, how quickly you can sell when the time comes, what your lender will let you borrow, and what you’re actually responsible for maintaining. I’ve walked buyers through all three, and the ones who end up happiest are almost always the ones who understood the differences before they started shopping — not after.

So here’s the full comparison. Condos, townhouses, and single-family homes. What you own, what you pay for, how they appreciate, how they finance, and who each one is actually right for in the King County market.

Property type comparison for King County buyers — ownership structure, HOA fees, and who each is right for.

What You Actually Own

This is where most people have fuzzy thinking, and it matters more than any other single factor.

Single-Family Home

When you buy a single-family home, you own the building and the land underneath it. Full stop. No HOA involved in most cases, though some planned neighborhoods do have one for shared amenities. If the roof leaks, that’s on you. If you want to paint the front door a different color, go for it. Your lot is yours to build a deck on or plant a garden in. That full ownership is exactly what makes SFHs appreciate the way they do. Land in King County is genuinely scarce, and land ownership transfers that value directly to you.

Townhouse

When you buy a townhouse, you typically own the structure and the land it sits on. Townhouses in King County are usually fee-simple, meaning you own your unit from the ground up. You share walls with neighbors, and there’s usually an HOA covering the common areas — shared driveways, landscaping, maybe a small courtyard. But the land is yours. That’s a meaningful difference from a condo, and it means townhouse appreciation tends to track closer to single-family than to condo over time.

Condo

When you buy a condo, you own the interior of your unit and a share of common areas. The land, the roof, the exterior walls, the lobby — all of that belongs to the HOA. Maintenance of those shared elements comes out of your monthly dues and out of a reserve fund that the HOA is supposed to be building over time. That arrangement is convenient right up until the roof needs replacing and the reserve fund is underfunded. More on that below.

The Price Gap Is Real in 2026

In King County as of early 2026, you’re looking at roughly these price ranges depending on what you’re buying and where.

Single-family homes in South King County — Renton, Kent, Auburn, Maple Valley — are running between $640,000 and $850,000 for typical resale product. The countywide median is hovering around $880,000. Anything under $600K in the SFH category tends to be smaller footprints or locations where the trade-off is commute time or school district.

Townhouses in those same South King County cities are typically coming in between $450,000 and $650,000. New construction townhomes near light rail corridors or in Kent’s East Hill area have been active in the $500K–$600K range. They’re a real path for buyers who want a two-car garage and a backyard without the $800K price tag.

Condos are the most variable. King County’s condo median dropped sharply — from around $690,000 in early 2025 to closer to $445,000–$577,000 in early 2026, depending on location. That’s a significant decline driven by a real imbalance in supply and demand for condos right now. More inventory, softer buyer demand, and a financing environment that makes condo purchases harder have all contributed. If you want to understand what current mortgage rates mean for your monthly payment across these price ranges, that post walks through the exact math.

How They Finance — This Is the Part That Surprises People

Financing a single-family home is the most straightforward of the three. Conventional loans, FHA, VA — all of these work with minimal restrictions. With strong credit and 3–5% down, you can access the full range of loan products.

Townhouses generally finance similarly to single-family homes, with one caveat. If the townhouse is part of a condo regime — meaning the ownership is structured legally as a condo even though it looks like a townhouse — lender scrutiny increases. Always ask your agent how the title is structured before assuming it finances like an SFH.

Condos are where financing gets genuinely complicated, and buyers often don’t find out until they’re already in contract.

Lenders classify condos as either warrantable or non-warrantable. A warrantable condo meets guidelines set by Fannie Mae and Freddie Mac — the HOA is financially healthy, owner-occupancy is above a certain threshold, no single entity owns too large a percentage of units, and the building isn’t in litigation. Those loans behave pretty normally. The interest rate runs about 0.125–0.375% higher than a comparable SFH purchase, and you can put as little as 3–5% down with good credit.

A non-warrantable condo is a different story. These are condos that don’t meet those standards — maybe the rental occupancy is too high, or the HOA has pending litigation, or the reserve fund is critically underfunded. Lenders who will touch these at all typically require 20–25% down and charge rates 0.5–1.5% higher than the warrantable equivalent. Some lenders won’t touch them at all.

HOA Fees and Hidden Costs: What to Actually Look For

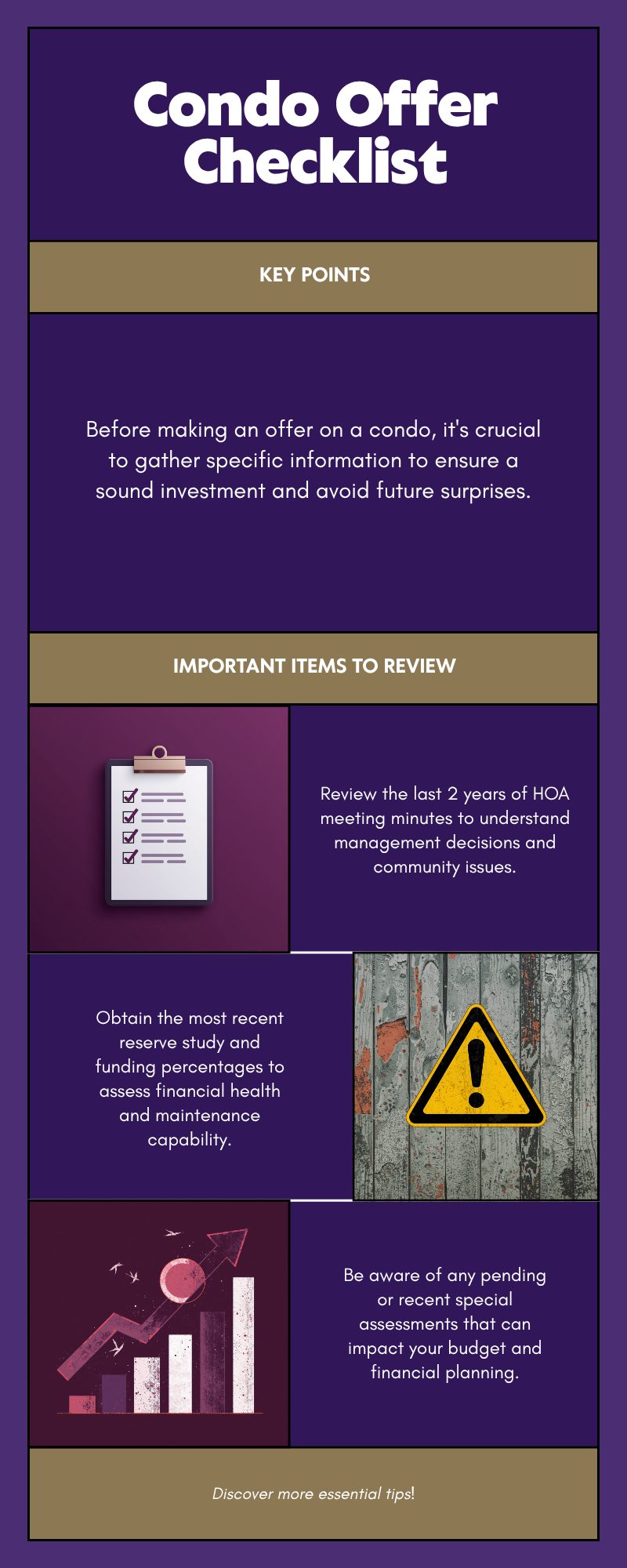

Request these documents before you make an offer on any condo in King County.

Every property type can have an HOA, but the nature and risk of HOA involvement varies considerably.

For single-family homes in planned communities, HOA fees tend to be modest — often $50–$150/month — and cover things like neighborhood common areas or a community pool. These are relatively low-risk from a special assessment standpoint as long as there aren’t major shared structures.

Townhouse HOAs typically run $200–$500/month in King County and cover shared exterior maintenance, landscaping, and common areas. The key question is: what exactly is the HOA responsible for? Some townhouse HOAs cover roof and siding; others leave the exterior entirely to you. Read the CCRs before you make an offer.

Condo HOAs carry the most complexity. Downtown Seattle condos can run $400–$1,000+/month. South King County condos tend to be lower — $250–$550/month — but can spike with age and deferred maintenance. And that brings us to the single biggest risk most condo buyers underestimate: the special assessment.

Washington State law (RCW 64.34.380 for condos) requires HOAs to conduct reserve studies and update them annually. A well-funded HOA sets aside money every month to cover large future expenses — roof replacement, elevator service, parking structure repairs. When an HOA is underfunded, it can’t pay for those repairs out of reserves. The result is a special assessment: a one-time charge to every unit owner, sometimes running $5,000–$30,000+ per unit.

Before you make an offer on a condo, request the last two years of HOA meeting minutes, the most recent reserve study, and the current percent-funded figure. If the reserve study shows less than 70% funding and the minutes mention deferred maintenance or upcoming projects, factor a special assessment into your budget. If they won’t provide these documents, that’s your answer.

Appreciation Patterns: Which One Builds Wealth Faster?

This is the question every buyer wants a clean answer to, and the honest answer is that it depends on time horizon and what you’re comparing.

Single-family homes in King County have the strongest long-term appreciation track record, driven primarily by land scarcity. As the region has grown, land in South King County has become more constrained. Homes in Renton, Maple Valley, and Auburn have all seen substantial appreciation over the last decade. The King County market as of May 2026 still shows SFH inventory tight enough at 2.8 months of supply to support pricing stability, with homes selling at 101.9% of list price on average.

Townhouses tend to appreciate in line with or slightly below SFH rates, depending on the product. New construction townhomes near transit corridors have performed well as demand for lower-maintenance, urban-adjacent living has grown. Fee-simple townhouses — where you own the land — typically hold value better than leasehold or condo-regime townhouses.

Condos are the most volatile of the three. The sharp drop in King County condo prices in 2025–2026 illustrates this clearly. Condos have periods of strong appreciation, particularly during high-demand, low-inventory cycles, but they also fall harder when demand softens. The oversupply of condo inventory right now, combined with the financing friction around non-warrantable buildings, has pushed prices down in ways that SFH and townhouse buyers haven’t experienced. That said, the current condo pricing environment does present a genuine opportunity for buyers who do the due diligence. Buying at a cyclical low in a well-run building in a strong location can produce solid returns. The key word is “well-run.”

The King County Local Angle: How Each Property Type Plays Out Here

South King County gives you examples of all three property types at accessible prices, and the differences matter more in this market than national averages suggest.

In Renton, you’ll find a mix of SFH in the $650K–$850K range, townhomes clustered near the Renton Highlands and Landing area in the $450K–$600K range, and condos in the Renton downtown corridor that have come down considerably in price. The light rail connection at the Renton Transit Center has increased buyer interest in Renton townhouses specifically. If you’re buying in Renton and considering a condo, the warrantability question is especially relevant — several Renton condo buildings are older and require careful reserve fund scrutiny. The Living in Renton guide covers the full neighborhood breakdown.

In Kent, townhomes in the $450K–$550K range have been some of the more active product in 2026. The first-time buyer guide for Kent covers the buy-now-vs-wait math that many Kent buyers are working through, and townhomes tend to be the property type that makes that math work at current rates.

In Auburn and Maple Valley, single-family homes still dominate the inventory. Townhouse product exists but is more limited. If you’re drawn to these communities for the school districts and neighborhood feel, the calculus often pushes toward SFH even if it means stretching the budget a bit further.

East King County — Issaquah, Bellevue, Sammamish — has a strong townhouse market particularly in the Issaquah Highlands and Talus communities, where mixed-use development has produced a large supply of attached product. These are generally well-maintained and have active HOAs with healthy reserves, but due diligence still matters.

What This Means for You as a Buyer

If you’re a first-time buyer in South or East King County in 2026, here’s the practical framework I’d use.

Budget Under $500,000

You’re likely looking at condos or newer townhomes. Condos offer the lowest purchase price but require more due diligence. Prioritize buildings with healthy reserves and warrantable financing status. If you can get into a well-run building at today’s discounted prices, you’re buying in at a favorable point in the condo cycle.

Budget $500,000–$700,000

Townhouses become your primary option for getting into ownership with land included. New and newer construction townhomes in Kent, Renton, and Federal Way fit this range. Prioritize fee-simple structures over condo-regime townhouses, and read the HOA docs before you fall in love with a floor plan.

Budget $700,000+

Single-family homes in South King County become realistic. You’ll find the strongest appreciation track record and the simplest financing path. The trade-off is less lock-and-leave convenience and more maintenance responsibility.

Frequently Asked Questions

What is the difference between a condo and a townhouse in King County?

A condo is a unit in a shared building where you own the interior space and a share of common areas. A townhouse is usually a multi-level attached home where you own the structure and the land it sits on. This difference in land ownership typically makes townhouses appreciate more like single-family homes and finance more like them too.

Is it harder to get a loan for a condo than a house in King County?

Yes, generally. Condos face additional lender scrutiny around HOA financial health, owner-occupancy ratios, and reserve fund adequacy. If a condo is classified as non-warrantable, you’ll typically need a larger down payment and accept a higher interest rate. Single-family homes and fee-simple townhouses don’t have this additional layer of review.

Are condos a good investment right now in King County?

Condo prices dropped significantly in 2025–2026, which means buyers who do careful due diligence can potentially buy at a cyclical low. The risk is that you’re buying into a shared financial structure (the HOA), so the quality of the building’s finances matters as much as the unit itself. In a well-run building, current pricing represents a real opportunity. In a poorly funded building, you’re taking on someone else’s deferred maintenance.

How much are HOA fees for condos vs. townhouses in South King County?

Condo HOA fees in South King County typically run $250–$550/month for older and mid-range buildings. Townhouse HOAs tend to be lower — $150–$400/month — and generally cover less exterior maintenance. Downtown Seattle and Eastside condos can run $400–$1,000+/month. Always include HOA dues in your monthly payment calculation when comparing properties.

What is a reserve fund and why does it matter when buying a condo?

A reserve fund is the HOA’s savings account for large future repairs — roof replacement, elevators, structural work. Washington State requires condos to conduct reserve studies and update them annually. If the reserve fund is significantly underfunded (below 70% of what it should hold), the risk of a special assessment increases. Special assessments are one-time charges to all unit owners that can run thousands to tens of thousands of dollars.

Can I use an FHA loan to buy a condo in King County?

Yes, but the condo building must be on the FHA-approved list. FHA imposes strict requirements on owner-occupancy rates, commercial space ratios, and HOA financial health. Search the HUD database to check a specific building’s approval status before getting too far into the transaction.

The property type you choose is one of the first big decisions in the buying process, and it shapes everything that follows — financing, monthly costs, what you maintain, and what you eventually sell. Understanding the differences upfront saves a lot of mid-transaction surprises.

Your guide to life outside Seattle.

253-350-0045 ·

greg@livingoutsideseattle.com ·

www.livingoutsideseattle.com