Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

King County Mortgage Rates 2026: What Buyers Are Actually Paying Now

King County mortgage rates in 2026 have been anything but predictable. In just 11 days in late March, the 30-year fixed rate jumped from 5.98% to 6.38%. That’s 40 basis points, and I got three calls from buyers who thought I’d made a mistake when they checked the numbers twice.

I’ve spent over 13 years as a field inspector evaluating properties for institutional clients across King County. When I tell you this rate move caught experienced buyers off guard, I mean it. Here’s what happened, what it costs you per month, and what to do about it.

Why King County Mortgage Rates Jumped 40 Basis Points in March 2026

The Federal Reserve didn’t cause this rate spike. The Fed has been holding steady for months. What drove Seattle area mortgage rates up was the bond market reacting to geopolitical events ‚Äî Middle East tensions, oil price volatility, and fear. The kind of volatility that reminds us mortgage rates don’t happen in a vacuum.

Mortgage rates track the 10-year Treasury bond, not the Fed’s benchmark rate directly. When investors rushed into bonds as a safe haven in late March, yields moved, and mortgage rates followed. It’s counterintuitive, but that’s how bond markets work.

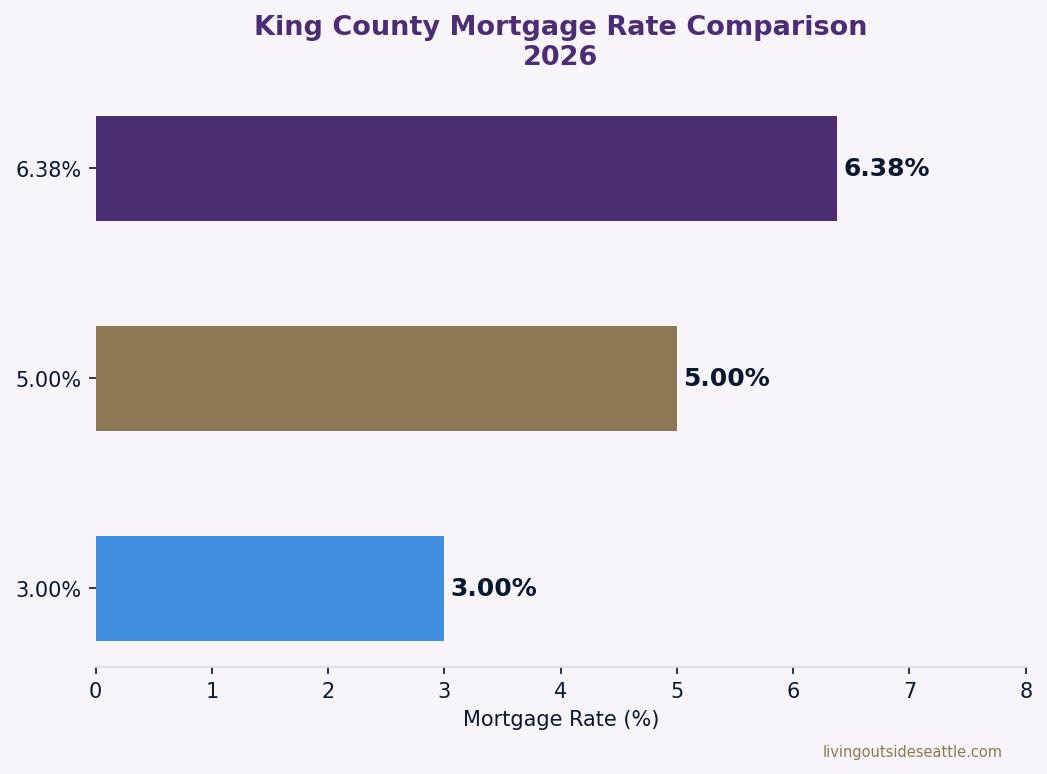

The result: the 30-year fixed rate hit 6.38% as of March 26, 2026. The 15-year fixed settled around 6.03%. And the Seattle area mortgage rate environment shifted fast enough to reshape buyer budgets overnight.

How the Bond Market Controls Your Seattle Area Mortgage Rate

Most buyers assume the Fed controls mortgage rates. It doesn’t, not directly. The Fed sets the federal funds rate, which affects short-term borrowing. Mortgage rates follow the 10-year Treasury yield, which responds to inflation expectations, global risk sentiment, and economic data.

When geopolitical tension spiked in late March 2026, bond investors moved money in ways that pushed mortgage rates up even though the Fed held steady. This is why rates can move 40 basis points between Fed meetings without any Fed action at all.

The Fed’s current position is “wait and see.” They’re watching inflation data and employment before making any moves. No rate cuts are on the near-term table. The bond market is doing the talking, and bond markets respond to global events faster than any central bank can.

For King County buyers, this means rate movements are harder to predict than ever. You can’t just watch Fed announcements to know where your rate is going.

What the Rate Increase Costs King County Buyers Per Month

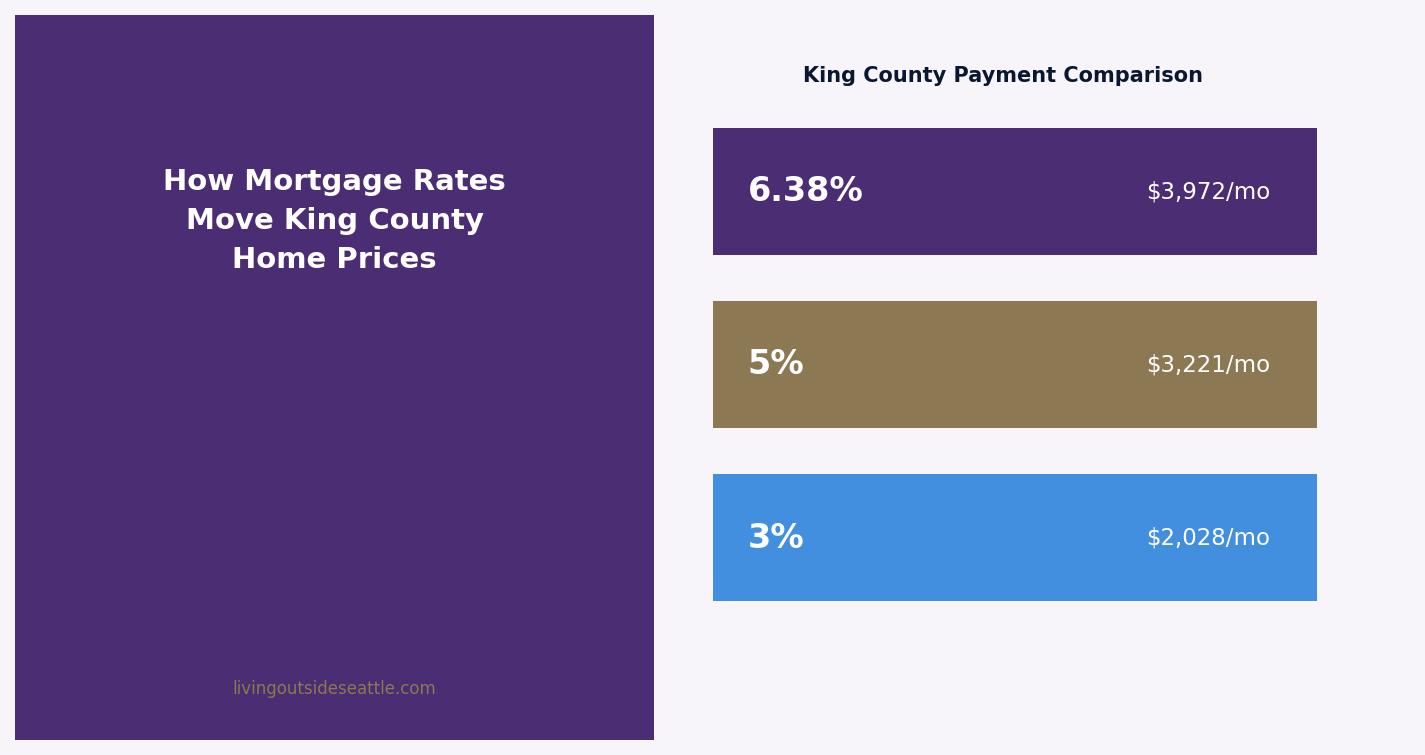

Let’s do the math on a real King County scenario. The median single-family home price in King County was $995,000 as of March 2026. With 10% down, that’s an $895,500 loan.

At 5.98% (late February), the monthly payment was about $5,370. At 6.38% (late March), it’s about $5,500. That’s $130 more per month on the same house.

On a $900,000 loan, each half-point rate increase costs roughly $300 to $350 per month. For buyers with a fixed budget, that $130 to $350 swing might be the difference between qualifying and not qualifying, or between a $700K range and a $650K range. In a market where King County’s median days on market is just 7 days, that payment pressure matters.

For context: the 30-year fixed rate was 6.65% this same week in March 2025. So despite the spike, you’re still borrowing at a lower rate than a year ago. That matters for perspective, even if the recent jump doesn’t feel good.

King County Housing Market Context: Inventory, Supply, and Demand in 2026

Here’s what makes this rate environment unusual. King County had 5,071 homes for sale in March 2026, up 37.5% year-over-year from 3,687 in March 2025. More inventory than we’ve seen in years. Monthly supply sits at 2.2 months for single-family homes, up from 1.4 last year. For condos, it’s 4.2 months, up from 3.3.

Buyers have more options. That’s good. But higher rates are squeezing the qualifying pool, especially at the upper end of the market. The list price ratio is holding at 100%, meaning homes sell at asking price on average. But the pool of buyers who can qualify at 6.38% is smaller than it was at 5.98%.

New listings jumped 16.5% year-over-year to 3,686 in March. That’s a market in transition. More homes, more time on market (though still fast at 7 days median), and fewer buyers who qualify per listing because of rate pressure.

Should You Lock a Mortgage Rate Now or Wait for Rates to Drop?

If you’re buying in the next 30 to 60 days, lock a rate. Here’s why: locking removes uncertainty. You know your payment. You know your deal works at that number. Rate locks typically run 30 to 45 days, so locking now protects you through closing.

Will rates drop? Maybe. But waiting for rates to fall while hoping prices stay flat has never worked consistently for buyers. If rates drop 1% but prices rise 3%, you’ve lost ground on both your monthly payment and your equity position.

Some buyers ask about rate buydowns. If a seller or builder is offering a 2-1 buydown, that’s worth evaluating. You pay less in the first year, a bit more in the second, then market rate from there. rate buydown explainer In a market with growing inventory, seller-paid buydowns are a real negotiating tool.

When Will Seattle Area Mortgage Rates Come Down?

Watch oil prices and geopolitical headlines, not just Fed announcements. That’s what’s been driving rates lately. If there’s a de-escalation in the Middle East or OPEC signals more production, rates could soften. But that’s speculation, and you can’t build a purchase timeline around it.

The Fed is on pause for the foreseeable future. Rate hikes are off the table, which brings some stability. But cuts aren’t imminent either.

For King County buyers in this environment, be realistic about budget. If your payment tolerance is $4,500 per month and rates stay at 6.38%, you’re looking at roughly a $700K purchase price with 10% down. If you were counting on rates dropping to 5.5%, your budget shifts meaningfully.

Frequently Asked Questions: King County Mortgage Rates 2026

What is the current 30-year fixed mortgage rate in the Seattle area?

As of late March 2026, the 30-year fixed rate is 6.38%, up from 5.98% just four weeks earlier. The 15-year fixed is around 6.03%. For reference, rates were at 6.65% this same week in March 2025, so you’re still borrowing at a lower rate than a year ago despite the recent increase.

Why did mortgage rates go up if the Federal Reserve didn’t raise rates?

Mortgage rates track the 10-year Treasury bond, not the Fed’s benchmark rate directly. When geopolitical tension spiked in the Middle East in late March 2026, bond market volatility pushed mortgage rates up even though the Fed held steady. This is why rates can move sharply between Fed meetings without any Fed action.

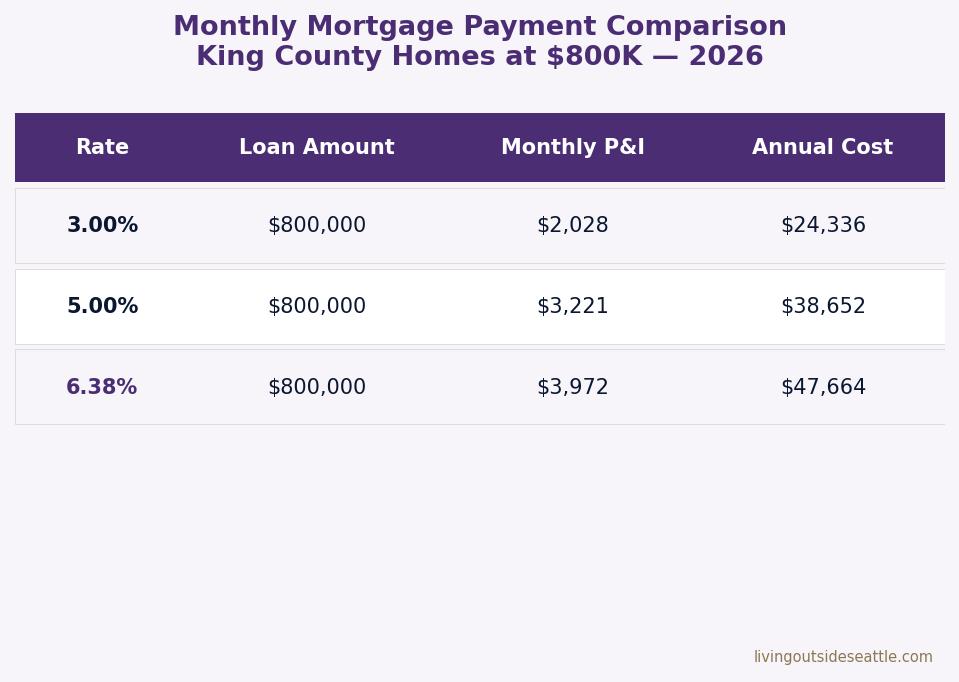

How much does a 0.5% mortgage rate increase add to a monthly payment in King County?

On a $900,000 loan, each half-point rate increase adds roughly $300 to $350 per month. On a $700K purchase with 10% down, the jump from 5.98% to 6.38% added about $130 per month.

What first-time buyer programs are available in King County?

Washington State Housing Finance Commission (WSHFC) offers programs including Home Advantage, which provides up to $10,000 in down payment assistance for buyers earning up to $147,400 in King County. The Covenant Homeownership Program also offers 0% interest down payment assistance for qualifying buyers. Talk to a lender before assuming these programs are out of reach.

Is it still a good time to buy a home in King County with rates at 6.38%?

That depends on your situation. If you’re planning to stay in the home five or more years and can afford the payment at today’s rate, buying now gives you price certainty and equity-building time. If rates drop later, you can refinance. The bigger risk is waiting for rates to fall while prices continue to rise.

Your guide to life outside Seattle.

253-350-0045 ·

greg@livingoutsideseattle.com ·

www.livingoutsideseattle.com

Gregory Dorrell is a licensed real estate broker (WA License #111862) with Coldwell Banker Bain. This post is provided for informational purposes and does not constitute financial or investment advice. Mortgage rates, terms, and availability are subject to change and vary by lender and individual circumstances. Please consult with a mortgage lender for current rates and pre-qualification information.