Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

How to Calculate the Total Cost of Homeownership in King County

Most buyers focus on the mortgage payment. That’s the number that shows up in every rate calculator, every lender pre-approval letter, every Zillow estimate. But in King County, the mortgage is often just 60–70% of what you actually pay each month to own a home. The rest — property taxes, insurance, HOA fees, PMI, and maintenance — adds up fast, and most first-time buyers get surprised by it.

I’ve worked in South and East King County for over 13 years, and I do professional property valuations every single day as a BPO field agent. One pattern I see constantly: buyers who were “pre-approved” for a purchase price they couldn’t actually afford once all the real costs hit their bank account in month two. This guide walks you through the full picture — every cost, with real numbers for King County cities — so you can make a decision you’ll still feel good about a year from now.

What Goes Into Your True Monthly Payment

The mortgage principal and interest (P&I) is the fixed part — it doesn’t change month to month on a 30-year fixed loan. Everything else does, or at least it can. Here’s the full stack of costs to run through before you make an offer.

Principal and Interest (P&I)

The core of your payment, and the number your lender leads with. At current King County rates of around 6.4–6.7% for a 30-year fixed, a $686,000 loan (10% down on a $763,000 Renton home) produces a monthly P&I payment of roughly $4,360. It’s real, but it’s not the whole story.

Property Taxes

Significant in King County — and they just went up. For the 2026 tax year, King County’s total property tax levy is $8.4 billion, a 10% jump from 2025. The average effective rate across the county runs around 0.9%–1.1% of assessed value annually. On a $763,000 home in Renton, that works out to roughly $690–$840 per month ($8,280–$10,080 per year).

Your specific parcel’s levy code determines the exact number — the King County Assessor’s eReal Property search tool will show you the breakdown for any address you’re evaluating. Renton sits on the lower end; Sammamish and Issaquah homeowners typically pay more because of school district levies and city-specific ballot measures.

Homeowners Insurance

Washington State averages $1,474–$1,596 per year — roughly $125–$133 per month. That puts Washington below the national average, which is a piece of good news. Expect to pay more if your home has a wood roof, is older than 30 years, or sits in a wildfire-adjacent zone (relevant in Maple Valley, Enumclaw, or Black Diamond).

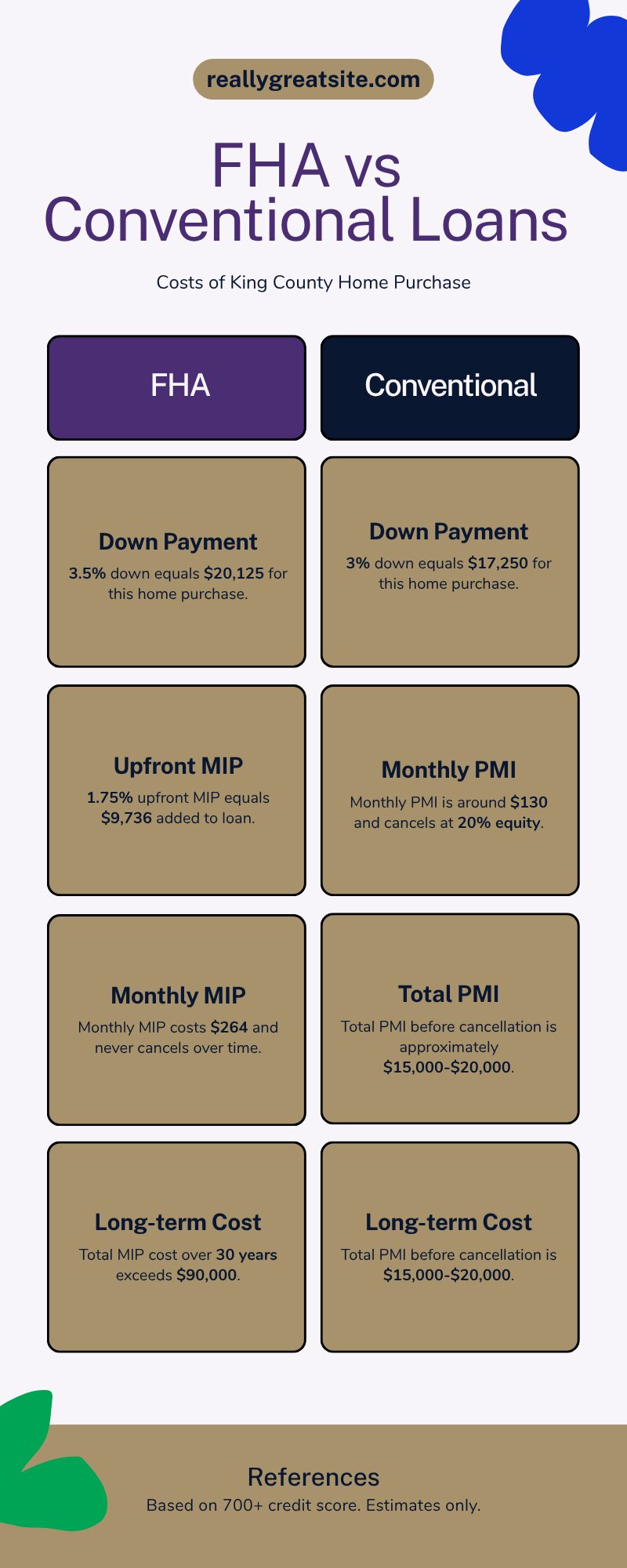

PMI (Private Mortgage Insurance)

Applies if you put down less than 20%. PMI typically runs 0.46%–1.5% of the original loan amount annually. On a $686,000 loan at a mid-range rate of 0.7%, that’s about $400 per month.

PMI drops off once you hit 20% equity — either through price appreciation or paying down the principal. Given King County’s 5-year appreciation history of roughly 5–6% annually, some buyers reach that equity threshold in 3–4 years rather than waiting out the full amortization schedule.

HOA Fees

These vary wildly by property type. Condos in King County typically run $300–$700 per month for a mid-range building — downtown Seattle luxury high-rises can exceed $1,000. Townhomes usually fall in the $150–$350 per month range. Single-family homes in planned communities often run $75–$200 per month for landscaping and common areas.

Many single-family homes in South King County have no HOA at all — which reduces monthly cost but means you carry 100% of exterior maintenance yourself.

Maintenance Reserve

The number most first-time buyers skip — and the one that bites hardest. The commonly cited “1% rule” (set aside 1% of your home’s value per year) is a reasonable floor. Studies show the average homeowner actually spends $8,800 per year on maintenance and repairs. For an older King County home (pre-1990), budget closer to 1.5%–2%.

On a $763,000 home, 1% equals $7,630 per year — about $636 per month set aside. You won’t spend it every month. Some months nothing breaks, then your furnace goes in January.

The mortgage payment is just one piece. For a Renton condo at $422K, all-in monthly costs run about $3,642. For a single-family home at $763K, expect closer to $6,224 per month. Source: King County market data, 2026.

Condo vs. Single-Family: How Total Cost Compares

This is one of the most common calculations I walk buyers through. The sticker price on a condo is lower — but the total monthly cost is often closer to a single-family home than buyers expect, once HOA fees are factored in. Here’s a real-numbers comparison using current King County data.

Condo in Southwest King County — $422,000

10% down ($42,200) / Loan: $379,800 / Rate: 6.5%

P&I: ~$2,400 | Taxes: ~$315 | Insurance: ~$80 | HOA: ~$450 | PMI: ~$222 | Maintenance: ~$175

Total: ~$3,642/month

Single-Family Home in Renton — $763,000

10% down ($76,300) / Loan: $686,700 / Rate: 6.5%

P&I: ~$4,342 | Taxes: ~$715 | Insurance: ~$130 | HOA: $0 | PMI: ~$401 | Maintenance: ~$636

Total: ~$6,224/month

The income difference this requires is significant. At a 28% front-end debt-to-income ratio (typical for conventional loan qualification), the condo scenario requires roughly $156,000 in gross household income. The single-family scenario requires roughly $267,000. Those numbers shift with your credit score, debt load, and lender — but they illustrate why the condo-vs-house decision often comes down to math rather than preference.

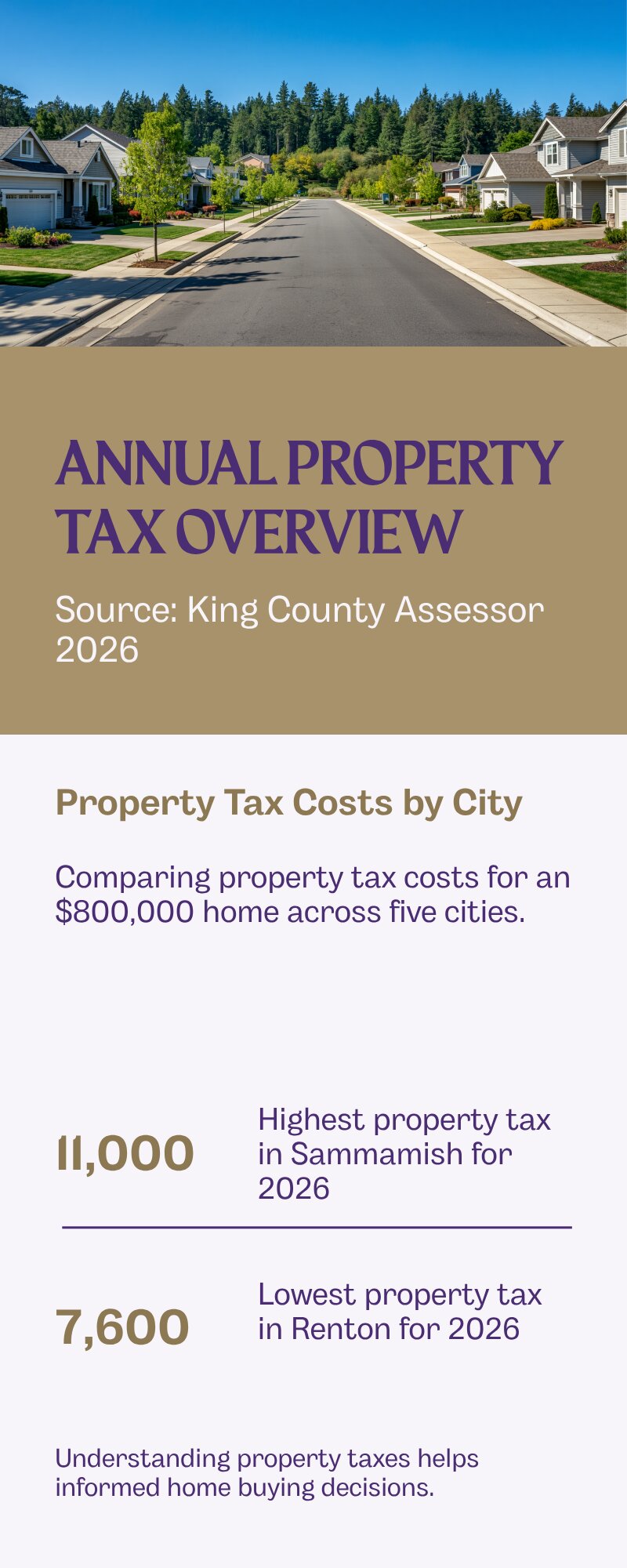

How King County Cities Compare on Total Cost

Property taxes are the biggest variable after the mortgage itself. Here’s a rough comparison of annual tax cost by city for a home around $700,000–$800,000.

Renton

Effective levy rate approximately 0.9%–1.0%. On an $800,000 home: ~$7,200–$8,000 per year ($600–$667/month). Renton sits on the lower end of King County cities, making it one of the better values in South KC for total monthly cost.

Kent & Auburn

Effective levy rates slightly higher than Renton, typically 1.0%–1.1%. On a $700,000 home: ~$7,000–$7,700 per year ($583–$642/month). School district and fire district renewal levies are a consistent factor in both cities.

Issaquah

Higher rates due to Issaquah School District supplemental levies — one of the highest-rated districts in the state, and that comes with a cost. On a $900,000 home: ~$9,000–$10,800 per year ($750–$900/month).

Sammamish

Among the highest effective rates in South/East King County. On a $1,000,000 home: ~$10,000–$12,000 per year ($833–$1,000/month). School district, city, and specialty district levies stack up quickly in Sammamish.

Annual property tax by city for an $800,000 home in King County. Renton and Kent are the most affordable in South KC; Issaquah and Sammamish carry higher levy rates driven by school district and specialty district measures. Source: King County Assessor 2026.

The Costs Most First-Time Buyers Underestimate

Beyond the monthly stack, a few one-time and recurring costs catch buyers off guard in year one.

Closing costs typically run 2%–3% of the purchase price. On a $763,000 home, that’s $15,260–$22,890 due at closing — on top of your down payment. This covers lender fees, title insurance, escrow, and prepaid items like the first year’s homeowners insurance and property tax reserves.

Immediate repair costs are real, especially in South King County where a lot of the housing stock was built in the 1980s and 1990s. Buyers of homes older than 30 years should budget up to $3,200 in unexpected year-one maintenance. A pre-listing inspection won’t catch everything — aging HVAC systems, older water heaters, and deck boards that just barely passed can all become your problem in year one.

HOA move-in fees and reserve contributions are easy to overlook. Some condo and townhome communities charge a one-time move-in fee ($500–$2,000) and require a contribution to the reserve fund at closing. Always request the HOA’s reserve study and financial statements before making an offer. Buildings with reserve deficits have hit some King County buyers with special assessments of $10,000–$30,000 per unit.

Utility cost changes hit harder than people expect when moving from a rental. You’re now paying for water, sewer, garbage, and often gas in addition to electricity. In South King County, expect $300–$500 per month depending on home size and season.

What This Means for Buyers in South and East King County

Running the full cost stack before making an offer is one of the most important steps a first-time buyer can take. The pre-approval letter and the real monthly budget are two different numbers.

My recommendation for buyers in Renton, Kent, and Auburn: run the full stack before falling in love with a specific home. The purchase price is a starting point. The number that actually matters for your quality of life is the total monthly outflow — and whether that leaves you enough runway to build equity, handle surprises, and not feel house-poor by month six.

For condos: the lower sticker price is real, but the HOA fee narrows the gap with single-family more than buyers expect. The King County Condo Buyer’s Guide walks through HOA due diligence in detail — including how to spot a building with a reserve fund problem before you commit.

For buyers still comparing property types, Condo vs. Townhouse vs. Single-Family in King County breaks down the full financial and lifestyle trade-offs side by side.

On the mortgage side: King County Mortgage Rates 2026 has the current rate picture and payment math, and the Mortgage Rate Buydown Guide explains how a seller-paid buydown can reduce your initial monthly cost in a way that pre-approval letters often miss.

Frequently Asked Questions

How much more than the mortgage payment is total homeownership cost in King County?

For most buyers, add $800–$1,500 per month on top of the P&I payment to get the true all-in cost. The biggest additions are property taxes ($600–$900/month on a median-priced home), insurance ($125–$135/month), and a maintenance reserve ($400–$700/month). PMI and HOA apply depending on your situation.

What is the property tax rate in Renton WA in 2026?

Renton’s effective property tax rate is approximately 0.9%–1.0% of assessed value annually, placing it on the lower end of King County cities. For a $763,000 home, expect roughly $6,900–$7,600 per year, or $575–$635 per month.

Do condos have lower total monthly costs than single-family homes in King County?

The purchase price is lower, but HOA fees close the gap. A condo at $422,000 with $450/month HOA ends up with a total monthly cost in the $3,600–$3,900 range. A single-family home at $763,000 (no HOA) runs $5,800–$6,400 per month all-in. The condo is still cheaper — but the difference is smaller than the price tags suggest.

Does PMI go away on a King County home?

Yes. Federal law requires lenders to cancel PMI automatically once your loan balance drops to 78% of the original purchase price. You can also request cancellation at 80%. Given King County’s appreciation history, some buyers hit that equity mark in 3–5 years rather than waiting out the amortization schedule.

What HOA fees should I expect for a King County townhome?

Townhome HOAs in South and East King County typically run $150–$350 per month. Lower-end communities cover exterior maintenance and landscaping only; higher-end communities include water, garbage, roof reserves, and exterior paint schedules.

What maintenance budget should I set for a King County home?

Budget 1%–1.5% of the home’s value per year. On an $800,000 home, that’s $8,000–$12,000 annually ($667–$1,000/month). For homes built before 1990, lean toward the higher end. Major systems — roof, furnace, water heater — can each cost $8,000–$15,000 when they need replacement.

Your guide to life outside Seattle.

253-350-0045 ·

greg@livingoutsideseattle.com ·

www.livingoutsideseattle.com