Living in Kennydale, Renton WA: What You Need to Know in 2026

Kennydale is the best-kept secret in north Renton. It sits on a hillside above Lake Washington, and on a clear day the views reach all the way to the Seattle skyline. The vibe is Family-First Established — mature trees, quiet streets, and neighbors who have lived here for years. In 2026, it remains one of the most consistent value holds in all of King County’s south end.

What Is It Actually Like to Live in Kennydale in 2026?

A weekday morning in Kennydale is peaceful. Streets curve through the hillside, and the canopy of mature big-leaf maple and Douglas fir muffles the sound from 405 below. Most residents leave between 7 and 8 a.m. for Bellevue or Boeing. By 8:30 the streets are quiet. There’s a neighborhood feel that’s hard to manufacture — it’s been here a long time and it shows in the way people take care of their homes.

Weekends, Coulon Park is the social hub. Residents walk down, let the kids swim, and spend Sunday mornings at the water. The neighborhood is close enough to north Renton’s commercial strip on N 3rd Street for groceries or coffee, but far enough up the hill that you don’t hear it. That separation is part of what Kennydale residents pay for.

The people who live here tend to be established families — dual-income households with school-age kids, Boeing engineers, and some retirees who have been here since the 1980s. Most buyers come here because they’ve outgrown somewhere else and want to plant roots.

Gene Coulon Memorial Beach Park gives Kennydale residents direct access to Lake Washington’s shoreline, just minutes from most homes in the neighborhood.

Homes in Kennydale: What the Data Shows

Kennydale’s housing stock runs mostly from 1960s to 1990s construction. Homes are predominantly single-family — ramblers and two-story traditional builds. Typical square footage ranges from 1,500 to 2,800 sq ft on lots between 6,000 and 10,000 sq ft. Many homes have been remodeled over the years, with updated kitchens and baths. The architectural style is Pacific Northwest Traditional — low-pitched roofs, wood or composite siding, and mature landscaping. View homes consistently command a premium here — often $50,000 to $100,000 above comparable non-view homes on the same street.

Market Pulse

Kennydale / 98056

King County

Median Sales Price (May 2026)

~$780,000

~$859,000

Median Days on Market

~18 days

~28 days

Active Listings Change (vs. Jan 2026)

+22%

+30%

Figures are approximate based on zip code 98056 activity. Verify current data at NWMLS.com.

Schools Serving Kennydale

Kennydale feeds into Renton School District. The primary pipeline is Kennydale Elementary, McKnight Middle School, and Hazen High School. Kennydale Elementary is known for strong parent involvement and a community garden program. McKnight has well-regarded arts and humanities electives. Hazen High offers a strong AP course selection and a well-funded athletics program.

Families who move to Kennydale often cite the school community as one of their top reasons for choosing this neighborhood. The pipeline is consistent and parent involvement at each school is above average for south King County. School boundaries in Renton can shift by street address, so always confirm your specific assignment with the district before writing an offer.

Most Kennydale kids walk or are driven to Kennydale Elementary, bus to McKnight for middle school, and drive or bus to Hazen for high school. Hazen’s dual-enrollment options through Renton Technical College give motivated students early college credit.

Getting to Work from Kennydale

Kennydale has two easy 405 on-ramps — NE 44th Street and Park Ave N — that put you on the freeway in under five minutes. Northbound 405 is your fastest path to Bellevue and Redmond. For Seattle, most residents take 405 north to I-5.

Kennydale’s housing stock runs primarily from 1960s to 1990s single-family builds with mature landscaping and, on upper bench lots, territorial views toward Lake Washington.

Destination

Distance

2026 Peak AM Drive

Transit Option

Downtown Seattle

12 miles

25 to 40 min

I-405 N to I-5 N

Amazon (South Lake Union)

14 miles

30 to 50 min

I-405 N to I-5 N

Microsoft (Redmond)

17 miles

25 to 40 min

I-405 N / Stride S2 + Transfer

SeaTac Airport

11 miles

18 to 30 min

I-405 S to SR-167

What I See as a Valuation Expert in Kennydale

When I assess homes in Kennydale for institutional lenders, the first thing I call out is the view line. A home that’s one lot off the ridge and loses the water view can appraise $60,000 to $80,000 less than an equivalent home with a clear lake sightline. That delta is significant. And it persists across market cycles.

The landscaping maturity here is real. Many properties have 30- to 50-year-old trees, established rhododendron plantings, and maintained lawns. That kind of curb appeal is hard to replicate and adds genuine appraised value. When I walk Kennydale, the homes on the upper bench streets — above roughly NE 36th Street — consistently show the strongest comps. Those streets have the best view angles and the least traffic.

Long term, Kennydale is one of the most defensible neighborhoods I work in. It has lake proximity, mature character, and Hazen High School as a school anchor. Those three factors rarely exist together at a sub-$800K median. If rates come down in 2027 and more buyers enter the market, this neighborhood will see competition fast. The 2026 window of higher inventory and less competition is a real opportunity.

Frequently Asked Questions About Kennydale, Renton WA

Is Kennydale a good place to live in Renton? Yes, especially for families who want lake access, mature neighborhoods, and solid schools without paying Bellevue prices. The upper bench view lots command a real premium, but for what you get — hillside position, Coulon Park proximity, and the Hazen pipeline — the value holds well over time.

What are homes like in Kennydale? Primarily 1960s to 1990s single-family construction — ramblers and two-story traditionals on lots of 6,000 to 10,000 sq ft. Most have been updated over the years. Upper bench lots with territorial or lake views add $50,000 to $100,000 in appraised value over comparable interior-lot homes.

What schools serve Kennydale? Kennydale feeds into Renton School District: Kennydale Elementary, McKnight Middle School, and Hazen High School. Always verify your specific address with the district before writing an offer, as boundaries can shift by street.

How far is Kennydale from Seattle? About 12 miles, with a typical peak AM drive of 25 to 40 minutes via I-405 N to I-5 N. Most residents drive. Stride S2 BRT is accessible from South Renton Transit Center for Bellevue connections.

Explore Kennydale Yourself

Drive the upper bench streets on a clear morning. Then walk down to Coulon Park and look back up the hill. You’ll understand the appeal immediately.

King County Condo Buyer’s Guide: What to Check Before You Make an Offer

A standard home inspection only covers your unit. Here’s how to check everything else — so you don’t inherit someone else’s financial mess.

If you’re shopping for a condo in King County, you already know the appeal. The $400K to $550K price range gets you into cities like Renton, Kent, Auburn, and Federal Way where single-family homes now regularly push past $700,000. Condos let first-time buyers get into the market with a lower entry point and no yard to maintain.

But buying a condo isn’t the same as buying a house. When you buy a condo, you’re not just buying the unit. You’re buying into the association that owns everything outside your four walls — the roof, the parking structure, the elevators, the exterior siding. You’re signing on as a stakeholder in the financial health of an organization you probably know nothing about yet.

That’s where most first-time condo buyers get burned. They fall in love with the unit, get excited about the price, and skip the due diligence that would tell them whether the building is a smart buy or a costly surprise waiting to happen. I’ve done BPO assessments on condo buildings across King County for years. The difference between a well-run community and a poorly-run one shows up in the documents — if you know what to look for.

Here’s what you need to check before you write that offer.

The Reserve Study: Your Most Important Document

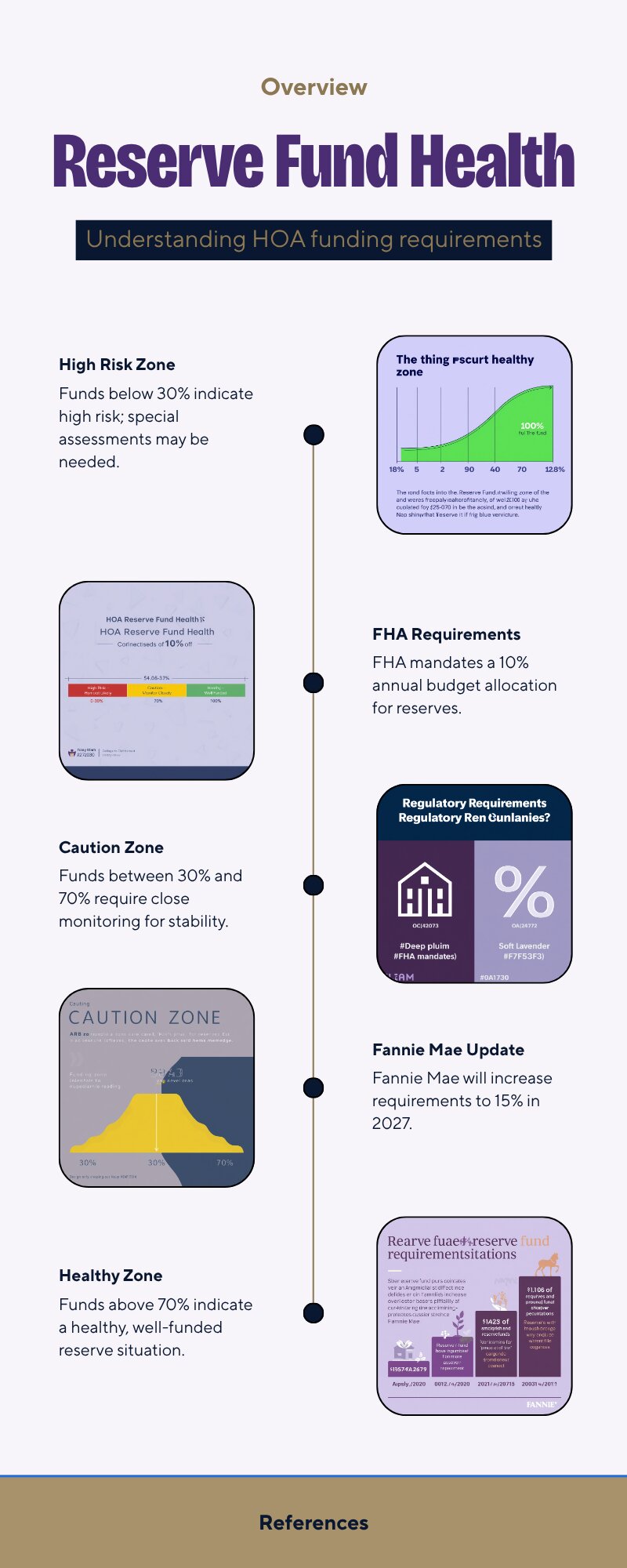

The reserve study is an independent engineering report that tells you two things: what major components the association owns (roof, siding, pavement, elevators, common area systems) and how much money the HOA needs to set aside right now to cover those replacements when they come due.

Think of it like a maintenance budget projected out 20 or 30 years. A well-funded reserve means the HOA has been saving consistently and won’t need to hit owners with a surprise bill when the roof fails. An underfunded reserve means the opposite.

Here’s the number that matters most: the funding percentage. Most reserve studies show this as a percentage of “full funding.” Anything above 70% is generally healthy. Below 30% is a serious red flag. According to the Community Associations Institute, more than 70% of HOAs nationally are considered underfunded. That’s not a comfort — it’s a warning about how common the problem is.

In Washington state, as of 2026, HOAs must include reserve fund information in resale certificates. Still, don’t rely on what the HOA tells you in summary form. Ask for the full reserve study report and read the section on reserve component status yourself.

Anything above 70% is generally healthy. Below 30%, a special assessment is likely — not a matter of if, but when.

Special Assessments: What They Are and How to Spot the Risk

A special assessment is an extra charge the HOA levies on every unit owner to cover a large expense the reserve fund can’t handle. They’re not uncommon. What makes them dangerous is that they can hit without much notice and they don’t care when you bought your unit.

An older 50-unit building might face a $200,000 roof replacement with nothing saved. That works out to $4,000 per unit — potentially due in a lump sum or in payments spread over a couple of years. Special assessments in King County can run $60,000 to $80,000 per unit when major structural or mechanical work has been deferred for years.

Before you make an offer, ask for the last five years of special assessment history. If there’s been one large assessment or multiple smaller ones in that window, ask why. The answer tells you a lot about how the board manages the property. Also ask whether any special assessments have been approved but not yet levied. Washington’s WUCIOA law requires this to be disclosed in the resale certificate — but only for assessments already approved by the board. A vote that hasn’t happened yet won’t show up anywhere except in the board minutes.

Which brings me to the board minutes.

Read the Board Meeting Minutes

Board minutes are a window into everything the summary documents won’t tell you. Most buyers never ask for them. That’s a mistake.

You’re looking for a few things specifically. First, any discussion of upcoming major repairs or capital projects. Second, any mention of litigation — whether the HOA is suing a contractor or a homeowner is suing the HOA. Third, any talk of raising dues significantly, levying a special assessment, or adjusting the reserve contribution downward to balance the operating budget. That last one is a classic sign of financial stress.

Under Washington’s WUCIOA updates effective January 1, 2026, condo associations must now hold open board meetings and provide better documentation to buyers. The resale certificate that comes with any condo sale must include 26 specific items and can only cost you up to $275. You also have a 5-day cancellation right after receiving all required documents. That window is your formal due diligence period — use it.

The Warrantable vs. Non-Warrantable Problem

This is the one that trips buyers up most often, and it has nothing to do with the unit itself. It has to do with the building.

A condo building is considered “warrantable” when it meets Fannie Mae and Freddie Mac lending standards. A warrantable building means you can get a conventional mortgage, FHA financing, or a VA loan — whatever you qualify for. Normal rates, normal down payments.

A non-warrantable building doesn’t meet those standards, and you lose access to the most competitive loan products. You’re looking at higher rates and larger down payments — often 20% or more — because portfolio lenders are taking on more risk. For a $500,000 condo, the difference between a warrantable and non-warrantable rate at current levels can easily add $200 to $250 to your monthly payment.

What Makes a Building Non-Warrantable?

The most common triggers in King County:

Single entity owns 25%+ of units — often an investor who bought in bulk during slower markets.

More than 35% commercial square footage — common in mixed-use buildings in downtown Renton or Federal Way.

Active or pending litigation — even a small dispute can knock a building out of warrantable status.

Ask your lender to run a condo project approval check before you get emotionally invested in a unit.

Many King County condo buildings — especially older mid-rises in Renton, downtown Kent, and Federal Way — fall outside warrantable guidelines. Knowing this upfront shapes your financing strategy before you’re already under contract.

For a full look at what mortgage rates look like right now for King County buyers, see our King County Mortgage Rates 2026 guide. If your condo ends up in the non-warrantable category, a mortgage rate buydown negotiated into the deal can help offset the higher rate.

Rental Cap Rules: What They Mean for Your Investment and Resale

Some condo associations limit how many units can be rented out at any given time. This is a rental cap, and it matters in two ways.

First, if you’re buying as an investor or might need to rent your unit down the road, a rental cap could block you entirely if the cap is already at its limit. Second — and this affects every buyer — a tight rental cap can make your building non-warrantable, which reduces your future buyer pool when you go to sell.

In Washington state, a rental cap must be written into the Declaration (the CC&Rs), not just the rules and regulations. Washington courts have ruled that caps can’t be created by the board alone — they need a supermajority vote to amend the Declaration. Check the current governing documents to see whether a cap exists, what the limit is, and whether it’s currently at capacity.

What a Standard Inspector Won’t Check

Here’s what a lot of condo buyers don’t realize: Washington state home inspectors are not required to inspect common elements, shared structural systems, or common area amenities. The inspector looks at your unit. The roof, the parking structure, the building envelope, the elevators, the main plumbing stack — those fall outside the standard inspection scope.

That means the structural and mechanical health of the entire building you’re buying into rests entirely on the HOA documents, not on any physical inspection you can order.

This is why the reserve study and the board minutes matter as much as they do. They’re the closest thing you have to a building inspection. If the association has been commissioning regular reserve studies and following the funding plan, you can feel reasonably confident. If the last reserve study is eight years old and nobody can find the financials, that’s your answer.

Washington’s new WUCIOA rules (effective 2026) cap the resale certificate fee at $275 and give you a 5-day cancellation window after receiving all required documents.

The Local Angle: What Makes King County Condos Different

King County’s condo market is concentrated in a handful of cities. The sub-$500K inventory you’ll find in Renton, Kent, Auburn, and Federal Way tends to be in older mid-rise buildings — think 1980s and 1990s construction. Some of these buildings have been well-maintained. Many have deferred capital work for years because the HOA fees were kept artificially low to attract owners.

As of the May 2026 King County market update, condo inventory is elevated relative to last year. That’s actually good news for buyers doing due diligence — you have more options and more negotiating room if a building’s documents reveal problems. You can move to the next building rather than feeling pressured to overlook red flags. For more on current conditions, see the King County Real Estate Market Update May 2026.

One thing I always watch from a pricing standpoint: HOA fees relative to market rates for the building’s age and amenities. An older building with fees significantly below market isn’t a deal — it’s a warning sign that the board has been cutting corners on reserves or maintenance to keep fees low. That cost shows up later. Often all at once.

If you’re weighing a condo against a townhouse or a single-family home in the same price range, the Condo vs. Townhouse vs. Single-Family Home in King County comparison guide can help you think through the tradeoffs before you commit to any one property type.

What This Means for You as a Buyer

Getting a condo offer right comes down to this: the unit is the easy part. Every agent will show you the finishes and the view. The due diligence that protects you happens in the documents.

Request the full resale certificate as soon as you’re seriously interested in a building — Washington law now limits the fee to $275 and gives you five days to review after receiving all required items. Use those five days. Read the reserve study funding percentage. Scan the last two years of board minutes for anything that sounds expensive. Pull the special assessment history. Have your lender check the project for warrantability before you fall in love with the floor plan.

If any of those documents are hard to get, incomplete, or missing entirely — that’s important information. A well-run HOA has nothing to hide.

Frequently Asked Questions

How do I get the reserve study and HOA financials as a condo buyer in Washington?

Request them in writing through your real estate agent as part of the offer or as a pre-offer document request. Under Washington’s WUCIOA law, the resale certificate is a required disclosure and must be provided within a set timeline. Your agent can request the full reserve study separately — not all associations include the full report in the standard resale package.

What reserve fund percentage should I look for when buying a condo in King County?

A funding level at or above 70% of “full funding” is generally healthy. Below 50% warrants a deeper conversation with the HOA or your agent. Below 30% is a serious red flag for near-term special assessments. FHA requires HOAs to allocate at least 10% of their annual budget to reserves — Fannie Mae is moving toward 15% effective January 2027.

What makes a condo non-warrantable in Washington state?

The most common triggers are high investor ownership (one entity owning 25%+ of units), active or pending litigation, short-term rental policies, and high commercial space concentration. Your lender can run a condo project approval check to confirm status before you’re under contract.

Can I use an FHA loan on a condo in King County?

Yes, if the building is FHA-approved or spot approval is available. FHA has its own approval process separate from conventional warrantability. Your lender will know whether the specific project is on FHA’s approved list or whether spot approval is an option for that building.

What should I look for in condo board meeting minutes?

Look for any discussion of deferred repairs, upcoming capital projects, special assessment votes (including proposed but not yet approved), litigation, significant dues increases, or decisions to reduce reserve contributions. Any of these can signal financial stress in the association.

Is a condo’s rental cap in the CC&Rs or the rules?

In Washington state, rental caps must be in the Declaration (CC&Rs) to be enforceable — not just the rules and regulations. If you see a rental cap only in the R&Rs and it’s not in the Declaration, its enforceability may be questionable under current Washington case law. Still, treat it as a real restriction until a real estate attorney tells you otherwise.

Buying a condo in King County can be a smart move. The entry-level price points in South King County are some of the last affordable options for first-time buyers in the region. But the savings on purchase price can disappear fast if you walk into a building with underfunded reserves, pending litigation, or a non-warrantable status nobody mentioned upfront.

The documents tell the story. Take the time to read them.

Relocating to King County from Out of State: What You Need to Know

A complete guide to neighborhoods, commutes, school districts, home prices, and how to buy before you move — from a local agent who knows this market by the block.

Most people moving to King County from out of state make the same mistake. They pick a city based on how close it is to downtown Seattle — and end up in a neighborhood that costs more, commutes worse, and feels nothing like what they imagined. I’ve helped enough relocators land here to know that the research most people do from a thousand miles away misses the things that actually matter once you show up.

This guide is the one I wish every out-of-state buyer had before their first house-hunting trip.

The City You Think You Want vs. the City That Actually Fits

When people tell me they’re moving to King County, they usually say “Seattle” or “Bellevue.” Those are fine places — I’m not going to talk you out of them — but they’re not the only options, and for most buyers coming from places like Phoenix, Denver, or the Bay Area, they’re not the right options either.

Here’s the honest breakdown.

Seattle

Urban neighborhoods, walkable coffee shops, quick access to Amazon and the medical corridor. Condos start around $500,000 and single-family homes run $871,000 median. If you’re working downtown and don’t have kids in public school, Seattle makes a lot of sense. If you’re working remotely or your employer is on the Eastside, the math gets harder fast.

Bellevue and the Eastside Tech Corridor

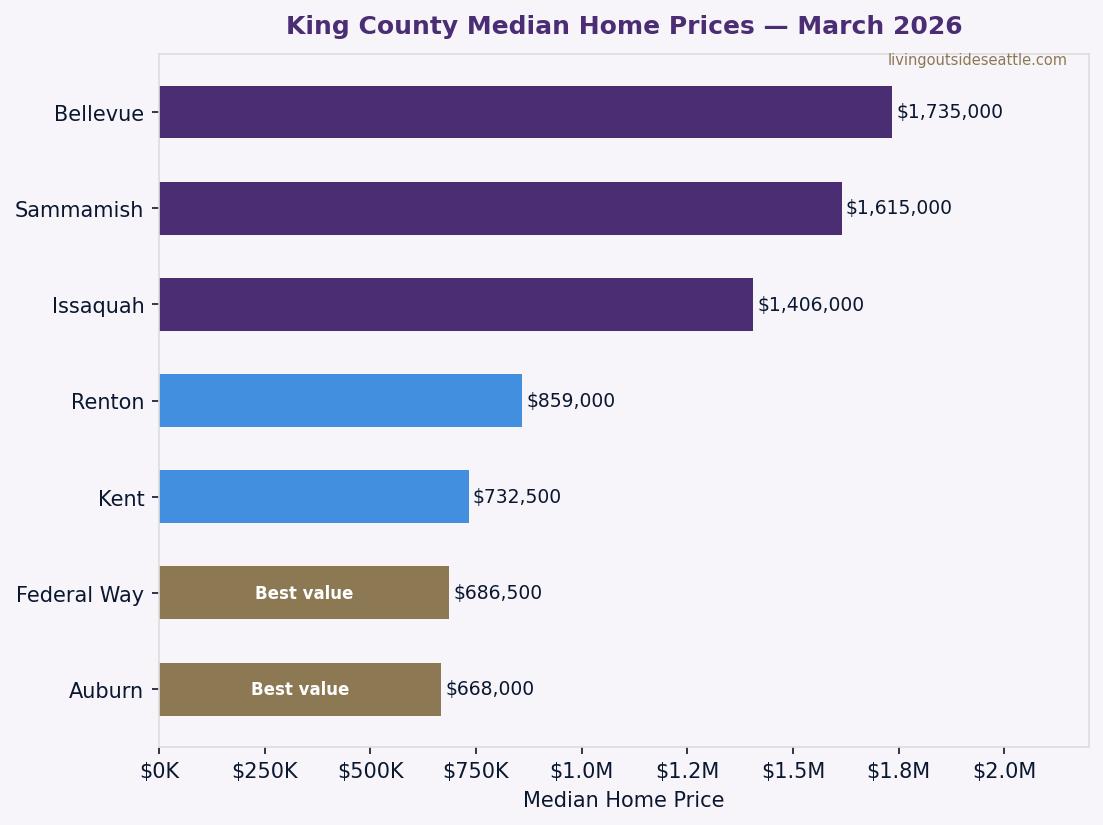

Redmond, Kirkland, and Sammamish are where most Microsoft, Google, and Amazon Eastside employees land. Schools are exceptional. Median prices are high: Bellevue runs $1.2 million and up, Sammamish hovers around $1.3 million. Issaquah sits at roughly $950,000 and still delivers top-tier school district quality for meaningfully less than its neighbors — that’s a real value play on the Eastside.

South King County

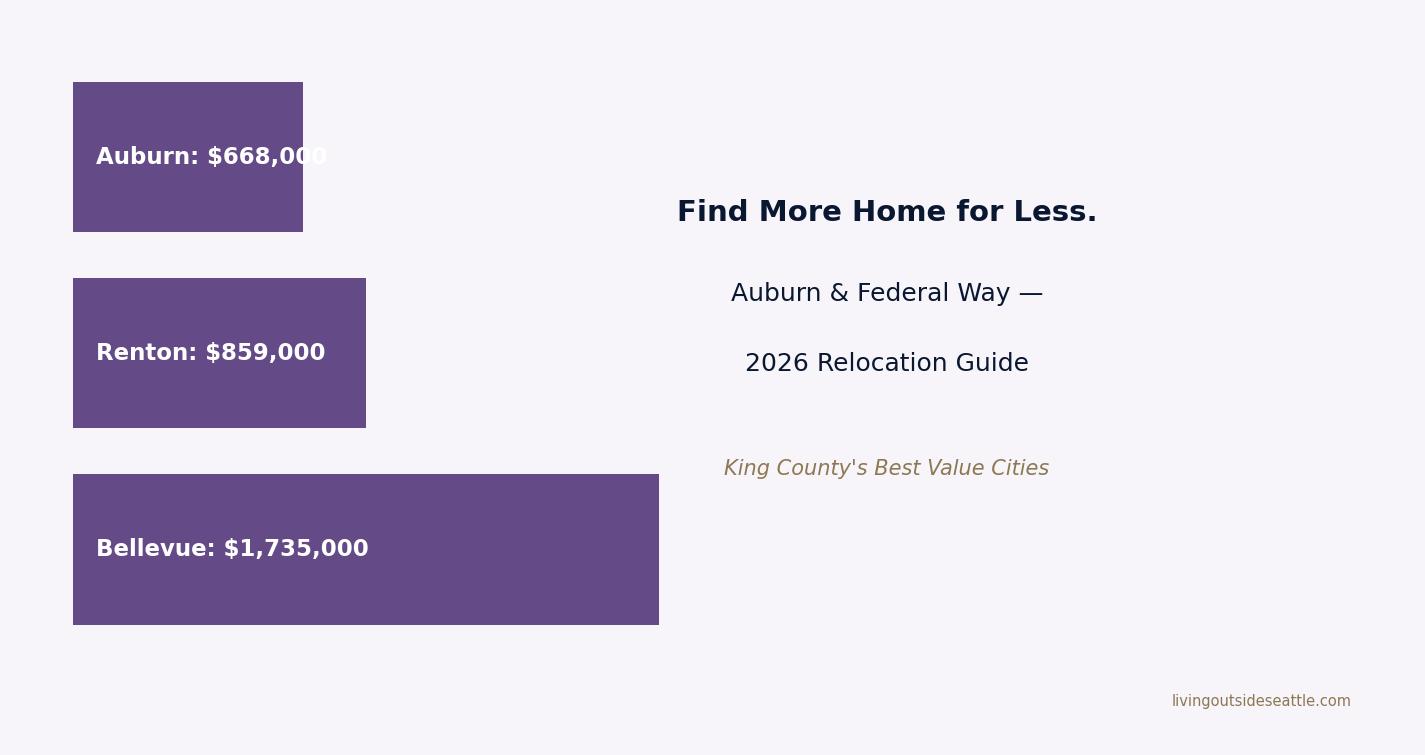

This is where I’d send most relocating families who are sticker-shocked by Eastside prices. Renton: $763,000 median, 12 miles from downtown Seattle, direct freeway access to the Boeing complex and the Amazon Renton campus. Kent: $647,000 median, the largest city in South King County, commuter rail service and one of the most diverse food scenes in the county. Auburn: $609,000 median, opening three new schools and rapidly growing. Maple Valley and Covington offer a quieter, more rural feel with large lots and 30-35 minute drives to employment centers.

None of those cities feel like settling. They feel like what most of the Pacific Northwest actually looks like — big trees, trail access, good neighbors, reasonable prices.

South King County neighborhoods like Renton, Kent, and Auburn offer large lots, trail access, and mountain proximity — at prices well below the Eastside.

What Surprises Relocators Most

I’ve had this conversation dozens of times. Here are the things that catch people off guard.

The gray is real, but it’s not rain. Seattle averages 92 rainy days a year — actually fewer than New York City or Miami. What people don’t expect is the persistent overcast: from October through May, the sky is more often gray than blue. It’s rarely dramatic. It’s just steady. Locals wear hoods, not umbrellas. You get used to it, but it’s worth knowing before you buy a house with a south-facing yard expecting sunshine nine months a year.

Traffic is directional and predictable. The I-405 corridor and I-5 are congested at the same times every day. If your commute runs south-to-north in the morning, you’re going the right direction. The light rail — which now reaches Federal Way and will extend further — is worth building your neighborhood choice around. I always ask relocating buyers: what’s your daily destination, and what time of day? That answer often changes which city we’re looking in.

Washington has no state income tax. This is the one that catches transplants from California off guard in the best way. Washington’s sales tax runs about 10.35% in King County, which is higher than you may be used to. But for most buyers, the absence of state income tax more than makes up for it. At a $200,000 household income, the tax savings versus California run roughly $16,000 a year.

The housing market here moves fast. South King County homes were selling in 6-14 days on average as of spring 2026. Coming from a slower market, buyers often underestimate how quickly they need to be ready to act. I’ve watched buyers from out of state lose homes they loved because they needed two more days to decide. Get pre-approved before you start touring — that’s the single biggest thing you can do to protect yourself.

School Districts: What the Rankings Don’t Tell You

If you have kids, school districts will drive a significant part of your city decision. Here’s how King County’s major districts actually stack up.

Tier 1 (Exceptional, reflected in prices): Bellevue, Mercer Island, Lake Washington, Northshore, and Issaquah school districts all carry top ratings and directly drive home values. If you’re buying in Issaquah, you’re getting Tier 1 schools at prices that are meaningfully below Bellevue and Sammamish — that’s the best value on the Eastside for school-focused families.

Tier 2 (Solid, good value): Federal Way Unified has improved significantly over the past five years and serves a growing commuter population near the new light rail station.

Tier 3 (Uneven — research by school, not just district): Renton and Kent school districts have significant internal variation. Hazen Senior High in Renton ranks #82 statewide, while other Renton high schools rank much lower. When I’m working with a relocating family buying in Renton or Kent, I always map the home address to the specific school assignment before we make an offer. The difference between two houses a mile apart can be significant.

Auburn School District is mid-tier overall but actively investing — three new schools are in development, and the district is growing alongside the city. If you’re buying in Auburn with a 10-15 year horizon, you’re buying into an improving situation.

How to Buy a Home Before You Move

This is the part most relocation guides skip over. Buying a home you’ve never stood inside, in a city you’ve never lived in, with an agent you met on Zoom — it’s genuinely stressful. Here’s how to do it right.

Buying from out of state works — but it takes the right prep. Full pre-approval, a local agent, and at least one in-person trip before closing.

Get fully pre-approved before you tour anything

Not pre-qualified — pre-approved, with income documentation verified and a real credit pull completed. Remote workers should get a Permanent Remote Work Letter from their employer in writing before applying. Verbal confirmation won’t satisfy an underwriter when you’re competing against local buyers who’ve been pre-approved for weeks.

Use virtual tours to eliminate, not to decide

Video tours are useful for crossing homes off the list. They are not reliable for choosing one. If at all possible, plan one trip to King County before your closing date — ideally to tour your top two or three candidates in person, walk the neighborhoods, and get a feel for the commute. If travel truly isn’t possible, ask your agent to do a live video walkthrough during a private showing and narrate everything the camera doesn’t capture.

Understand how Washington closings work

Washington is an escrow state. There are no real estate attorneys at the closing table — an escrow officer and title company facilitate the process. Closings can be done electronically, which makes remote buying workable. You’ll wire funds and sign documents digitally. The process is straightforward once you know what to expect. Also know that Washington’s wet western climate makes moisture intrusion, crawl space condition, and roof health the top three inspection items — do not skip the inspection to be competitive.

The Local Angle: What the King County Market Looks Like Right Now

King County inventory is up roughly 35% year over year as of spring 2026. That’s meaningful. It means relocators have more options, more negotiating leverage, and fewer situations where they need to waive every contingency to win. Inspection contingencies are back on the table in most South King County transactions. Seller concessions — including buydowns and closing cost help — are more common than at any point since 2019.

For a relocator on a tight timeline, this is a much better environment than 2022 or 2023. You’re not walking into a war. You’re walking into a real market where your offer gets read and your questions get answered.

The overall King County median was $880,000 in March 2026. But that number obscures the real value story. If your target is South King County — Renton, Kent, Auburn, Maple Valley — you’re looking at a $609,000 to $763,000 range, with growing inventory and motivated sellers.

2026 median home prices across King County. South King County cities offer the best value for relocators who don’t need to be in Seattle or on the Eastside every day. Source: King County MLS, spring 2026.

Start your neighborhood research with your daily destination, not with a map of the county. Where will you spend Tuesday mornings? That question is more useful than “how far is it from downtown Seattle.”

Build your city shortlist around school district tier, commute direction, and price ceiling — in that order. Then let the neighborhoods inside those cities narrow your search.

Get pre-approved before your first house-hunting trip. In South King County, a well-priced home can go under contract in a week. Showing up financially ready is the difference between buying the house and watching it disappear.

And check the down payment assistance programs available to King County buyers. If your household income is under roughly $175,000, you may qualify for programs that put $10,000 to $55,000 toward your down payment. See the full 2026 down payment assistance guide for eligibility and how to stack programs.

If you’re also weighing where to land specifically in South King County, my guide to relocating to Auburn, Washington covers one of the county’s fastest-growing cities in detail.

Frequently Asked Questions

Is King County expensive compared to other major metros?

King County’s median home price of $880,000 puts it in the top tier nationally — roughly on par with Los Angeles and San Diego. However, the absence of Washington state income tax makes total cost of living comparisons more favorable than the home price alone suggests. At a $200,000 household income, the tax savings versus California run roughly $16,000 a year — which offsets a meaningful portion of the price premium over time.

How long does it take to buy a home in King County?

From pre-approval to closing, most transactions run 30 to 45 days. In competitive South King County neighborhoods, timelines can compress. An out-of-state buyer with full pre-approval and a clear target area can move from first showing to accepted offer in a single trip if the timing is right.

Do I need to be physically present to close?

No. Washington State allows electronic closings. You can sign documents remotely and wire funds from anywhere. Some buyers close on King County homes without ever setting foot in the state prior to moving in — though I strongly recommend at least one visit before making an offer.

What are the biggest mistakes out-of-state buyers make?

Three come up repeatedly: choosing a city based on proximity to Seattle when their actual commute destination is elsewhere; arriving without pre-approval and losing homes they loved; and skipping the inspection to strengthen an offer — a risk that almost never pays off in a western Washington climate.

What school districts are best for families relocating to South King County?

Within South King County, the answer is school-specific rather than district-specific. Renton and Kent both have high-performing individual schools alongside lower-performing ones. When I’m working with a family in those areas, we map every address to its specific school assignment before making an offer. Issaquah School District is the clearest top-tier pick on the Eastside at a relatively accessible price point.

Is now a good time to buy as a relocating buyer?

King County inventory is at its highest level in years, inspection contingencies are standard again in most areas, and seller concessions are available. For a relocating buyer with solid pre-approval and flexibility on timing, this is a more favorable environment than it’s been since before the pandemic. See the total cost of homeownership guide for the math on waiting vs. buying now.

Moving to King County is a big decision. The region is genuinely excellent — trails, mountains, water, good jobs, and communities that feel like home once you’re here. The hard part is choosing the right community before you’ve lived in any of them. That’s what I’m here for.

King County Housing Market Forecast 2026: What Buyers and Sellers Should Expect

The King County housing market has shifted. After three years of near-frantic competition, rising inventory, softening prices in some sub-markets, and mortgage rates that have settled (but not dropped) are reshaping what buyers and sellers can expect in 2026. If you are trying to decide whether to buy, sell, or wait, this is the data you need to see before making that call.

I price homes professionally every day as a BPO field agent. That means I am watching this market in real time, not just reading headlines. Here is my honest read on where King County is heading through the rest of 2026 and what it means for you.

Where the King County Housing Market Stands Right Now

The headline numbers tell a story of transition. As of April 2026, the median home sale price in King County is $835,000 — down roughly 7.5% from the same period last year. Active listings have surged 39% year over year, the largest inventory increase of any major metro in the country. Days on market has stretched from 7 to 12 days countywide.

What does that mean in plain terms? Buyers who spent 2022 and 2023 losing bidding wars on homes now have time to actually look at a house before making an offer. Sellers who priced their home based on last year’s comps are finding out the hard way that the market has moved.

The months of supply figure is the cleanest measure of balance. King County is sitting at roughly 3.2 months right now. A fully balanced market is 6 months. We are not there yet — sellers still have a meaningful edge — but the trend line is clear. This is no longer a “list it and watch offers pile up” market.

King County Housing Market Forecast: What Mortgage Rates Mean for Timing in 2026

Mortgage rates have driven more decisions in this market than any other factor since 2022. The 30-year fixed rate is sitting at roughly 6.6–7.0% as of mid-2026. Most forecasters, including Fannie Mae, project rates will drift toward the low 6% range by year end — possibly 6.0–6.2% by December.

Here is the “so what” for buyers: rates probably are not going to 5% anytime soon. If you are waiting for rates to drop dramatically before buying, you may be waiting into 2027 or beyond. A drop from 6.6% to 6.0% on a $700,000 loan saves you roughly $225 per month. That is meaningful, but it is also erased quickly if prices rebound when rates fall and competition picks back up.

For sellers, rate sensitivity explains why your buyer pool has shrunk. Every half-point increase in mortgage rates prices out a segment of buyers. At 6.6%, a buyer who qualifies for $650,000 at 5.5% now qualifies for roughly $585,000. That is not a small gap when median prices in South King County are in the $640–735K range.

The 30-year fixed rate is at 6.6%+ in mid-2026. Most forecasters project a drift toward 6.0–6.2% by year end — meaningful relief if it holds. Source: Fannie Mae / NWMLS.

South King County: A Different Story Than the Headlines

The countywide numbers can be misleading if you are buying or selling in South King County. Renton, Kent, Auburn, and Maple Valley are holding up differently than the Eastside.

Renton

Median price around $640–671K as of early 2026, with homes selling in about 13 days on average. Prices are up roughly 2% year over year — not the decline you see at the countywide level. Renton’s relative affordability compared to Bellevue and Seattle keeps demand stable even as higher-priced markets soften.

Kent

The most varied market in South King County right now. Entry-level and mid-range homes are moving. Higher-priced homes and properties needing updates are sitting longer. If you are a Kent seller, condition and pricing precision matter more than they did two years ago.

Auburn

Holding at roughly $645K median with about 42 days on market — meaningfully longer than Renton. Auburn’s affordability attracts first-time buyers, but that segment is also the most rate-sensitive, which is slowing absorption.

Maple Valley

Continues to attract buyers who want larger homes, outdoor access, and strong schools. One of the more consistently active pockets of South King County, with new construction in Black Diamond adding adjacent supply.

The pattern across all four: price under $700,000, good condition, well-presented. These homes are still moving. The market is being selective, not frozen.

What the Tech Layoffs Are Actually Doing to King County Real Estate

Amazon cut roughly 16,000 jobs company-wide, and the Puget Sound region absorbed the heaviest share. When you add Microsoft’s reductions, an estimated 16,000–17,000 tech workers in King County have been affected in 2026. That is a real demand shock at the high end of the market.

The impact is not uniform. High-end single-family homes in Bellevue, Kirkland, and parts of Renton’s Highlands that were popular with tech workers have seen price softening and longer days on market. Capital gains tax concerns are pushing some high-net-worth sellers to delay, which keeps certain inventory off the market even as lower-priced inventory rises.

South King County is less exposed to the tech demand shock. Buyers in Renton, Kent, and Auburn tend to be Boeing employees, healthcare workers, educators, and local service industry professionals — a more diversified employment base. That is part of why South KC numbers have held steadier than the Eastside.

What This Means for Sellers in 2026

If you are thinking about listing this year, here is the straight answer: you can still get a strong price, but you have to earn it now. The days of overpricing and waiting for a buyer to blink are over for most of King County.

Accurate pricing from day one

Overpriced homes are sitting. I track price reductions in my BPO work daily, and the pattern is clear — homes that start too high end up selling for less than a well-priced home would have gotten from the start. The first 10 days on market are everything.

Condition matters more than it did

Buyers have options now. If your home needs work and it is priced like it does not, buyers will skip it. Light repairs, fresh paint, and thorough cleaning move the needle far more than expensive renovations.

Timing within the season still matters

The spring selling season (March–June) still produces the best results in King County. We are in the tail end of it right now. If you are ready, there is still a motivated buyer pool. Waiting until fall means competing with another wave of listings when buyer activity historically slows.

In today’s King County market, condition and pricing accuracy matter more than ever. Sellers who prepare their home and price it right are still winning.

What This Means for Buyers in 2026

Buyers have more leverage today than at any point in the last four years. Here is how to use it.

You have time to do proper due diligence. Request inspection contingencies. You are likely to get them in markets where days on market is 12 or more. Two years ago, buyers routinely waived inspection rights to compete. That is no longer necessary in most price ranges in King County.

You can negotiate on price and concessions. With 3.2 months of supply, sellers who need to move are willing to talk. Seller-paid closing cost credits and rate buydown contributions are showing up again. I am seeing this regularly in my work.

Do not wait for rates to drop to “perfect.” Every month you wait on the sidelines is a month of rent paid with no equity building. The break-even math on buying vs. renting in most of South King County favors buying, even at today’s rates, when you factor in equity accumulation and the real likelihood that prices in sub-$700K markets do not fall meaningfully.

King County Sub-Market Snapshot for the Rest of 2026

Here is my honest forecast by market tier through December 2026:

Under $700K — South KC (Renton, Kent, Auburn)

Stable to modest appreciation (1–3%). Buyer demand is steady. Rate sensitivity keeps some buyers on the sidelines but also keeps prices from running up fast. This is the most reliable segment of the market right now.

Choppy. Tech demand softening is felt here. Sellers need to price defensively. Good homes priced right will sell in 2–3 weeks; overpriced homes will sit for months.

$900K+ — Bellevue, Kirkland, Premium Eastside

The most exposed segment. Inventory has grown, demand from tech workers has pulled back, and capital gains sensitivity is keeping some equity-rich sellers hesitant. Expect continued price pressure through Q3.

New Construction

Continues adding supply in Black Diamond, Auburn’s Lakeland Hills, and parts of Maple Valley. This additional inventory matters for resale sellers in those areas — you are competing with builder incentives that individual sellers cannot match.

Frequently Asked Questions

Will home prices drop in King County in 2026?

Countywide, prices are down about 7.5% from the spring 2025 peak. In South King County sub-markets like Renton, prices are still slightly positive. A dramatic crash is not supported by the data — inventory is rising but still well below 6 months supply. Gradual softening at the high end is the more likely path through 2026.

Should I buy now or wait for rates to drop?

If you find the right home and can afford it at today’s rates, buying now is usually the smarter call. When rates drop, competition will pick up and prices will likely respond. You can always refinance into a lower rate. You cannot go back and buy at today’s prices once the market shifts.

Is it still a seller’s market in King County?

In some pockets, yes. South King County under $700K is still closer to a seller’s market. The countywide data and the Eastside above $900K are trending toward balanced. It depends heavily on your specific city, price point, and property condition.

How are tech layoffs affecting real estate in my neighborhood?

The impact is most direct within 10 miles of major tech campuses — parts of Bellevue, Kirkland, Redmond, and parts of Renton. If you are in South King County (Auburn, Kent, Federal Way, Maple Valley), the effect is indirect and more muted.

What is the biggest mistake sellers are making right now?

Overpricing based on what a neighbor sold for 18 months ago. The market has moved. Comp selection requires a skilled eye right now — a small difference in how you select comparables produces a very different number, and getting it wrong costs sellers real money through price reductions and carrying costs.

How many months of supply is King County at?

Roughly 3.2 months as of mid-2026, up from under 2 months a year ago. A balanced market is typically defined as 6 months of supply. We are not there, but the trend has shifted meaningfully toward buyers.

Sammamish Real Estate Market 2026: What Buyers and Sellers Need to Know

If you’ve been watching Sammamish real estate over the past few years, you already know: this is one of the most sought-after communities on the Eastside, and it shows in the price tags. Median home values sit right around $1.6 million in 2026, making Sammamish one of the priciest zip codes in King County.

But the story this year is more nuanced than the headline number. Inventory has crept up, homes are sitting a little longer than they did at the peak, and prices have softened roughly 3 to 4 percent from a year ago. For sellers, that doesn’t mean panic — demand is still real and buyers are still showing up. For buyers, it means more options and a little more room to negotiate than you would have had in 2022 or 2023.

I track this market every week through my BPO work, and what I’m seeing in Sammamish right now is a market recalibrating after years of compressed inventory and rapid price growth. Here’s what the numbers actually mean for you.

What the Numbers Say Right Now

Sammamish median home prices in spring 2026 are tracking around $1.6 to $1.64 million, depending on the data source. Redfin pegs the median sale price at approximately $1,614,000. Zillow’s typical home value sits at $1,638,223. Both numbers are down roughly 3.5 percent from a year ago — a notable shift for a market that spent several years climbing.

Days on market tell a similar story of moderation. Well-priced homes in good condition are still moving fast — some in 5 to 7 days with multiple offers. Homes that are overpriced or need significant work are sitting 18 to 26 days, which would have been unheard of three years ago. The price you set matters more right now than it did when buyers were waving inspection contingencies and offering $200,000 over list.

Inventory has loosened compared to the tightest years, but Sammamish is still operating well below a balanced market, which sits at about 4 to 6 months of supply. Active supply is thin enough that demand pressure remains. This market hasn’t flipped to buyer-favored territory — it’s just stopped being the feeding frenzy it was at the peak.

For sellers, the practical takeaway: you still have leverage, but you need to use it correctly. Overpricing by $50,000 to $75,000 “to leave room to negotiate” doesn’t work the same way it might have in a tighter market. Buyers are comparing more options and walking away from listings that feel off on price.

For buyers, the takeaway is equally clear: you have more choices and more time than you did in 2021 or 2022. You don’t have to waive every contingency. But you should still move with conviction on homes that check your boxes — quality listings still generate real competition.

How Sammamish Compares to the Rest of the Eastside

Sammamish is the most expensive city in King County by median home value. That’s worth understanding before you make your buying or selling decision.

Sammamish holds the highest median home value on the Eastside in 2026, roughly $500K above Issaquah. Source: Redfin, Zillow, Spring 2026.

The premium you pay in Sammamish over Issaquah or Redmond — often $300,000 to $500,000 — reflects a few specific things: newer housing stock (most of Sammamish was built in the 1990s through 2010s), top-rated school districts, lower density, and a community feel that attracts families who want good schools and quiet streets without moving far from the Eastside employment corridor.

That premium has historically held. Even with the current softening, Sammamish has outperformed most Eastside cities over a 5 or 10-year horizon. But sellers need to understand that the premium is earned by condition and positioning — not just geography. A Sammamish home that needs updating competes against Redmond and Issaquah homes that don’t, and buyers will make that comparison. See also: King County Real Estate Market Update May 2026 for broader context.

The School District Factor

If you ask Sammamish buyers why they’re specifically targeting this city, schools come up almost every time. Sammamish sits at the intersection of two of the most respected school districts in Washington State: the Lake Washington School District, serving the north end, and the Issaquah School District, serving the south end. Both consistently rank among the top districts in the state.

The Lake Washington School District includes schools like Skyline High School and Eastlake High School, both of which draw families from across the Eastside specifically for those programs. The Issaquah School District feeds into Issaquah High and Skyline High, with strong AP and IB programs that matter to families relocating from competitive metros.

For sellers, this is a legitimate marketing point — not a soft lifestyle appeal, but a hard financial reality. Buyers moving from California, Texas, or the Midwest to take tech jobs in Redmond or Bellevue will specifically filter for Sammamish when school quality is the priority. That drives demand even when the broader market softens.

What Sammamish Sellers Should Know Right Now

Sellers who enter this market with an accurate price and a prepared home are still doing well. Sellers who overprice expecting the 2021 frenzy to carry them are getting a lesson in how the market has changed.

Sammamish’s newer housing stock — most built between the 1990s and 2010s — is a primary driver of its Eastside price premium.

Pricing Accuracy Is the Most Important Variable

My BPO work has me assessing Eastside property values every week. The gap between correctly priced homes and overpriced homes in Sammamish right now is 3 to 4 weeks of market time. That’s not a small difference. The longer a home sits, the more buyers assume something is wrong with it, and the harder it becomes to get back to your original target price.

When buyers had fewer options, they would accept cosmetic issues and deferred maintenance because they had no choice. Now that buyers have a few more homes to consider, a home that shows well has a real advantage. Fresh paint, clean landscaping, and repaired deferred maintenance items are worth the investment before you list.

The First Two Weeks Set the Trajectory

In a market where overpriced homes are sitting 18 to 26 days, the competitive advantage of launching right is significant. Homes that enter the market priced accurately and prepared well still generate multiple offers. The window to capture that momentum is short — price reductions after two or three weeks on market rarely recreate the same energy.

What Sammamish Buyers Should Know Right Now

Buyers in Sammamish right now have something that didn’t exist for most of the past five years: options. You can see three or four homes before making a decision. You’re less likely to write an offer the day a home lists without seeing it in person first.

That said, Sammamish is not a buyer’s market. It’s a market where qualified, prepared buyers can move strategically — but don’t mistake “less frenzied” for “no competition.” Well-priced homes in good condition on desirable streets still see multiple offers and sell above list.

Get Pre-Approved Before You Tour

At $1.6 million median, you’re looking at a down payment of $320,000 or more at 20 percent, plus significant cash reserves. Sellers at this price point will not take your offer seriously without a solid pre-approval letter from a real lender — not just a pre-qualification estimate.

Know Your School Boundary Priorities First

The north/south split between Lake Washington and Issaquah school districts doesn’t affect every buyer equally, but if you have school-age children, you need to know which side of that line matters to your family before you fall in love with a home that feeds into a different school than you expected. Ask your agent to confirm the school assignment for any home you’re considering.

Don’t Skip the Inspection

Waiving inspections was common during the 2021–2022 frenzy. In today’s Sammamish market, you may not need to. A home inspection at this price point is not the place to cut corners. A few hundred dollars and a few days could save you from a six-figure repair surprise after closing.

In a market where buyers have more options than in recent years, a well-prepared home has a real competitive advantage.

The Local Angle: Sammamish in the King County Context

Sammamish is a pure Eastside story — it shares very little with South King County markets like Renton, Kent, or Auburn in terms of price point or buyer profile. But for buyers who are earlier in their Eastside search and feeling priced out of Sammamish, understanding how the Eastside premium stacks up can help clarify the decision.

If $1.6 million puts Sammamish out of reach but you want the same general area, Issaquah at roughly $1.1 million offers access to the same Issaquah School District, similar Pacific Northwest lifestyle features, and meaningful price savings. Redmond at $1.34 million gets you closer to the Microsoft and Amazon campuses with slightly smaller homes and higher density. To understand what life looks like in Sammamish before you commit, the Living in Sammamish guide covers neighborhoods, commutes, schools, and lifestyle in detail.

For sellers in Sammamish considering their next move, South King County remains a meaningful destination for buyers trading down in size while capturing equity from an Eastside sale. Renton, Kent, and Covington offer price points 60 to 70 percent lower than Sammamish — and the buyer pool for those markets is partly funded by equity releases from Eastside sales.

Frequently Asked Questions

Is Sammamish a good place to buy a home in 2026?

Sammamish remains one of the most desirable communities in King County because of its school districts, newer housing stock, and proximity to Eastside employers. Prices have softened about 3–4% from the 2025 peak, which is a modest improvement for buyers without signaling a market downturn. If you plan to stay 5 to 10 years, buying in Sammamish in 2026 is a reasonable long-term decision.

How much does a home in Sammamish cost in 2026?

The median sale price is approximately $1.6 to $1.64 million, depending on the neighborhood and property type. Single-family detached homes make up the vast majority of the Sammamish market. There is limited condo or townhome inventory compared to cities like Bellevue or Redmond.

How long are homes sitting on the market in Sammamish?

It depends heavily on pricing. Well-priced homes in good condition sell in 5 to 10 days with multiple offers. Overpriced homes or those needing significant updates can sit 18 to 26 days. The gap in outcomes between well-priced and overpriced homes is larger right now than it was at the 2021–2022 peak.

Is Sammamish more expensive than Bellevue?

By median home value, yes. Sammamish’s median of $1.57–1.64 million is higher than Bellevue’s median of approximately $1.45 million. However, Bellevue has significantly more price diversity because it includes condo and urban-density housing. For single-family detached homes on comparable lots, the price difference narrows.

Which school district serves Sammamish?

Most of Sammamish is served by either the Lake Washington School District (north end) or the Issaquah School District (south end). Both are highly rated and are primary draws for families buying in Sammamish. Specific school assignments depend on the property address — confirm with the district before finalizing a purchase.

Is now a good time to sell a home in Sammamish?

Demand is real and inventory remains constrained relative to a balanced market, so sellers still have leverage. The key is entering the market with accurate pricing and a well-prepared home. Sellers who overprice by 5 to 10 percent are finding the market does not bail them out the way it did a few years ago.

How to Read a Comparative Market Analysis (CMA): A King County Seller’s Guide

Two agents. Same house. Two completely different prices. Here’s how to tell which one is right.

Most sellers in King County interview two or three agents before listing. They get a CMA from each one. And more often than not, those CMAs land in different places — sometimes by $20,000, sometimes by $80,000. Then comes the question nobody wants to ask out loud: which agent is actually right?

The answer isn’t always the highest number. And it isn’t always the lowest. It comes down to how each CMA was built, which comps were chosen, and whether the agent is telling you what the market says or what you want to hear.

This guide walks you through how to read a CMA the way a pricing analyst does — what to look for, what to question, and why the methodology behind the number matters as much as the number itself.

What a CMA Actually Is

A Comparative Market Analysis is a written report — sometimes a few pages, sometimes a full presentation — that estimates what your home would sell for on the open market today. An agent prepares it using data from the local MLS: recent sales, current active listings, and homes that went under contract but haven’t closed yet.

The CMA is not an appraisal. It doesn’t carry legal weight and isn’t prepared by a licensed appraiser. But a well-done CMA uses the same core methodology: find comparable sales, adjust for differences, and arrive at a defensible price range. The difference is in who does it and how rigorously.

A CMA is also not a Zestimate. Automated valuation tools are algorithmically generated from public records and don’t account for interior condition, recent renovations, or hyperlocal factors that move prices in King County. They’re a starting point for curiosity, not a basis for pricing your home.

What you’re looking for in a CMA is a specific kind of precision: recent sales that are genuinely similar to your home, adjustments that reflect real market behavior, and a price recommendation with logic you can follow.

The Anatomy of a Good CMA

A complete CMA has five parts — recent closed sales, price adjustments, active listings context, a price range, and days-on-market data. Missing any one of these is a yellow flag.

The Comparable Sales Section

This is the heart of the analysis. A solid CMA uses 3–6 closed sales — homes that actually sold and recorded with the county, not just homes that were listed. Active listings show you the competition; they don’t tell you what buyers actually paid.

Strong comps are sold within the past 90–180 days, within roughly half a mile in dense neighborhoods, similar in size (within 20%), similar in age and style, and similar in condition. The more adjustments required to bridge the gap between a comp and your home, the less reliable that comp is as an anchor.

The Adjustment Section

Here’s where CMAs diverge. Every comp is adjusted up or down to match your home. If the comp had a three-car garage and yours has one, the agent reduces that comp’s adjusted value. If your home has a finished basement the comp didn’t, an upward adjustment goes in. These adjustments should reflect what buyers in your market actually pay for those features — not round numbers made up on the spot.

Check: Are the adjustments reasonable in proportion to the sale price? Do the comps include some that are better than your home (requiring downward adjustments), or are all adjustments upward? If every adjustment inflates the comp’s value, the CMA may be padded.

Active, Pending, and the Price Range

A complete CMA includes the current competition — what’s on the market now and what’s pending. If similar homes have been sitting for 45 days at your proposed price, that’s a data point worth knowing before you list.

The final output should be a price range, not a single number. Within that range, your agent recommends a specific list price based on your goals and market conditions — and that recommendation should come with a clear explanation. “We can always come down” is not an explanation.

Why Two Agents Give You Different Numbers

Two agents can produce legitimately different CMAs because pricing involves judgment calls — which comps to use, how much to adjust for condition, whether the market is moving up or flat. Reasonable professionals can disagree within a range.

But the real reason sellers often see large gaps between CMAs has nothing to do with analytical disagreement. It’s called buying the listing — when an agent inflates their CMA to win your business. They know you’ll be more excited about the higher number. They sign you up at that price, the home sits, and three weeks later they start asking for a price reduction.

By then, you’ve already lost the prime marketing window — the first two weeks when a new listing gets the most attention from buyers. Homes that require price reductions consistently sell for less than they would have if priced correctly from day one. Buyers notice price cuts. They wonder what’s wrong with the house.

If you see these patterns in a CMA, ask questions before you sign a listing agreement.

The BPO Difference: Why Daily Pricing Work Matters

Most agents prepare CMAs occasionally — when they’re pitching a listing. That means they’re doing this analysis once every few weeks, or less.

My background is different. As an active BPO field agent, I assess property values professionally every single day for banks, lenders, and investment portfolios. That means I’m running the same comp analysis — pulling recent sales, making adjustments, arriving at a reconciled value — on multiple properties every morning. Not when a listing appears on my desk. Every day.

What that produces is calibration. I know what buyers in Renton paid for a renovated kitchen last month because I priced three homes in Renton last month. I know how much a lot size premium is worth in Kent right now because I’ve been tracking it continuously, not revisiting it once a quarter.

When I prepare a CMA for a seller, I’m using the same methodology a lender’s appraiser will use when a buyer’s loan comes through. That alignment matters: a home priced with institutional-grade rigor is much more likely to appraise cleanly at contract price — which means fewer renegotiations and a smoother path to closing. For more on how appraisals interact with your list price, see our guide to how to price your home to sell in King County.

The difference isn’t just credentials — it’s frequency. Daily pricing work produces calibration that occasional CMA preparation can’t match.

What a CMA Can’t Tell You

A CMA is backward-looking. It tells you what buyers paid for comparable homes in the past 90–180 days. It doesn’t tell you what the market will do next month, and it doesn’t account for factors that haven’t shown up in closed sales yet — like a shift in mortgage rates, a wave of new inventory, or a major employer making news in your area.

This is why the agent’s current market knowledge matters as much as the data itself. A CMA prepared by someone who isn’t actively watching the King County market day-to-day will miss signals that a daily practitioner picks up on. Always ask the agent: “Has anything happened in the past 30 days that your comps don’t reflect?” Their answer will tell you whether they’re watching the market or just pulling data.

The King County Specifics Worth Knowing

Sub-market pricing is everything. King County covers an enormous range of price points and market conditions. Renton, Kent, Auburn, Covington, and Maple Valley each behave differently from each other and from the Eastside. A good CMA uses comps from the same sub-market — not comps from a neighborhood three cities over that happens to have similar square footage.

Median prices shifted in early 2026. The April 2026 King County median home sale price came in around $835,000 — down roughly 7.5% year-over-year at the county level, though South King County remained more competitive than average. Comps from 12+ months ago may overstate what your home will actually trade for today. An agent who’s pulling year-old data to support a high price isn’t serving your interests.

Days on market is now a meaningful signal. King County homes are averaging around 12 days on market — up from 7 days a year ago. That shift means the “price it high and wait for the right buyer” strategy is riskier than it was in 2022. Buyers have more options, and a home that sits past 30 days starts raising questions that a price cut can’t fully answer.

School district boundaries move prices. In cities like Newcastle that straddle multiple school district zones, a half-mile difference in location can produce a meaningful price difference. Your agent needs to know which side of those lines your home is on — and make sure the comps are on the same side. For more on what goes into getting your home ready to sell, see our guide on how to prepare your home for sale in King County.

Questions to Ask at Your Listing Appointment

When you sit down with an agent to review their CMA, bring these questions:

On the Comps

Why did you choose these specific sales and not others? How recent are they — and are there more recent sales you considered and rejected? How similar is this comp in size, condition, and location to my home?

On the Adjustments

How did you arrive at the adjustment amounts? Are any of your comps adjusted up by more than 20%? Are there any comps where you made downward adjustments, or are all adjustments upward?

On the Pricing Recommendation

What’s your recommended price range, and where do you suggest we list within it? What happens to our negotiating position if we list at the top of your range and don’t get an offer in two weeks? How does your recommended price compare to what a buyer’s lender will appraise it at?

On the Agent

How many pricing analyses have you done in the past 30 days in this specific sub-market? Have you seen any recent shifts in buyer behavior that your closed comps don’t yet capture?

The agent who answers these questions clearly — without hesitation, without pivoting to their marketing plan — is the agent who did the work.

Frequently Asked Questions

How much does a CMA cost?

A CMA from a real estate agent is free. Agents prepare them as part of their listing pitch. If you want an independent opinion not tied to a listing relationship, a licensed appraiser will charge $600–$900 for a formal appraisal.

Is a CMA the same as an appraisal?

No. A CMA is prepared by a real estate agent and used to set a listing price. An appraisal is prepared by a state-licensed appraiser, required by lenders, and used to determine the maximum loan amount. A home can be listed above its likely appraisal value — which creates problems at closing when the buyer’s lender won’t fund the gap.

How many comps should a good CMA include?

Typically 3–6 closed sales, plus 2–4 active or pending listings for competitive context. Fewer than 3 sold comps is a thin basis for a pricing recommendation. More than 8 often means the agent is padding with weak matches to justify a predetermined number.

What if two CMAs are far apart?

Ask each agent to walk you through their comps side by side. The differences usually come down to which comps were selected and how adjustments were applied. If one agent can’t explain their methodology clearly, that tells you something about how they prepared the analysis.

Should I always list at the top of the CMA range?

Only if your goals and market conditions support it. In a market where homes are selling in 7–12 days, pricing at the midpoint of the range often generates more competing offers than pricing at the top — and can produce a higher net sale price. Your agent should walk you through the trade-offs before you decide.

Getting a CMA is easy. Getting a CMA you can actually trust — one built with the same rigor a lender’s appraiser will apply to the same property in 60 days — takes a different kind of preparation. And knowing how to read one puts you in a position to tell the difference.

How to Price Your Home to Sell in King County 2026

Getting the price right from day one is the single biggest decision you will make as a seller. Here’s exactly how to do it in today’s King County market.

The Market Has Shifted — And Pricing Has to Shift With It

A few years ago, you could price a King County home at the top of the range, sit back, and let competing buyers push the number up for you. That strategy worked because there were almost no homes to choose from and buyers were desperate. That market is gone.

As of May 2026, active listings across King County are up roughly 31% year over year. Days on market in King County 2026 have nearly doubled — from 7 days a year ago to an average of 12 days now. That is not catastrophic — this is still not a buyer’s market in the traditional sense — but it is a fundamentally different environment than what sellers experienced in 2022 and 2023. Buyers today are walking a home twice, requesting inspections, and waiting to see what comes up next weekend before they write an offer.

In that environment, your list price is not just a number. It is a signal. And if you send the wrong signal, you will pay for it in ways that are hard to recover from.

Why Overpricing Costs You More Than You Think

This is the part most sellers don’t believe until they’ve lived through it. The instinct to price high makes sense emotionally — you love your home, you’ve put money into it, and you want to leave room to negotiate. But the math does not support it.

Here is what actually happens when a home is overpriced in King County right now. It sits. After 10 to 14 days with no offers, buyers start asking why. They can see the listing history. They know when a home has been on the market too long, and they start to assume something is wrong with it — even when the only problem is the price. The longer it sits, the more that perception hardens.

Then comes the price reduction. When you drop the price after three weeks on market, you do not get a fresh start. You get buyers who feel validated in their suspicion and who are now motivated to negotiate even harder. Research shows that homes requiring a price reduction in King County typically sell for less than they would have if they’d been priced correctly from day one. You gave up both time and money.

The irony is that a correctly priced home in 2026 is your best shot at a bidding situation. When buyers see a home priced at market — not above it — they move with more urgency. Because they know another buyer might too.

Overpricing creates a cascade. Pricing right from day one nets you more.

How to Build the Right List Price: What Comps Tell King County Sellers

The foundation of any good pricing decision is comparable sales — homes that have actually closed, not homes currently listed. Active listings are your competition. Closed sales tell you what buyers in King County are actually paying right now.

What a Useful Comp Set Looks Like in 2026

Recency: Sales closed within the past 60 to 90 days only. Anything older is telling you what the market was, not what it is today.

Geography: Same neighborhood or school district boundary, not just the same city. A home in Covington’s Tahoma School District zone is a different product than one outside it, even if they’re a mile apart.

Size and condition: Similar square footage (within about 200 sq ft), similar lot size, similar age, and — critically — similar condition. A home with original 1990s finishes is not the same product as one with a remodeled kitchen and new bathrooms.

Once you have your comp set, focus on two numbers: the list-to-sale ratio and days on market. King County’s county-wide sale-to-list ratio is running around 101.6% right now — but that average includes many well-priced homes pulling it up. Look specifically at homes that sold without a price reduction. Those are the ones worth modeling.

What the 2026 King County Market Means for Your Strategy

The rate environment adds another layer to this. Mortgage rates are sitting around 6.5% to 6.7% as of late May 2026, and they’ve been creeping up. At that rate, every $50,000 you add to your asking price adds roughly $300 per month to a buyer’s payment. That is not a small number for the families moving through Renton, Kent, Auburn, and Maple Valley — the buyers who make up the bulk of transaction volume in your neighborhoods.

Rate-sensitive buyers are doing the math carefully. They have a payment ceiling, and they are not going to stretch past it for a home that doesn’t feel worth it. That means a home priced $25,000 to $50,000 above market will often not even get shown to the right buyers — because their lender-qualified search range doesn’t reach it.

King County’s inventory increase also means your home is being compared against more options than it was a year ago. When a buyer in Covington has five homes to look at in their price range instead of two, your home has to earn its keep. Pricing is how you get them in the door.

The communities in South King County — Kent, Auburn, Covington, Maple Valley — are still seeing solid demand, especially at the entry-level and move-up price points. But the tolerance for overpricing has shrunk considerably. For the full market picture, see the King County Real Estate Market Update May 2026.

The BPO Advantage: Why Professional-Grade Pricing Matters

Most agents price a home by pulling a few comps and applying general intuition. I do it differently.

As an active BPO (Broker Price Opinion) field agent, I assess property values professionally — not just for my own listings, but on behalf of lenders, banks, and servicers across the county, every single day. That means when I look at your home, I am applying the same methodology that financial institutions use when they need to know exactly what a property is worth in the current market.

I know which condition adjustments to make and which ones buyers will actually pay for. I know how to weight a comp that is slightly outside your neighborhood. I know when inventory is absorbing slowly in a specific price band and how that should affect your initial pricing position. This is not a guess — it is a professional assessment built on hundreds of valuations a year.

When You Should Consider Pricing Slightly Below Market

There is one scenario where pricing a touch below the comp average makes strategic sense — when your goal is to create urgency and maximize final sale price through multiple offers.

This works best when inventory in your price band is low, your home shows exceptionally well, and you have a realistic expectation of where offers will land. You are essentially setting the stage for buyers to compete rather than negotiate. A $10,000 to $15,000 under-ask on a well-presented home can result in multiple offers and a final price above what you would have gotten listing at market.

The choice is simple. The execution is where sellers need help.

What This Means If You’re Thinking About Selling

If you’re weighing whether to list this spring or summer, here is the straightforward version: pricing correctly in 2026 is more important than it has been in years, and the margin for error is smaller.

Start with an honest CMA from an agent who knows your specific neighborhood — not just your zip code. Get a condition assessment. Look at what is competing with you right now, and look at what sold in the past 60 days. If you are thinking about pricing above that range because of what you “need” from the sale or what a neighbor got two years ago, that is a conversation worth having before you list, not after.

The sellers who do well in the current King County market are the ones who commit to accurate pricing from the start, present their home well, and trust the process. They are still getting strong results. The sellers who struggle are the ones treating 2026 like it’s 2022.

Frequently Asked Questions About Pricing Your Home in King County

How do I know if my King County home is priced right?

If you have had 10 to 15 showings in the first two weeks and no offer, the price is almost certainly off. In the current King County market, a correctly priced, well-presented home generates activity in the first week. No traffic is a price signal, not bad luck.

Should I price high and leave room to negotiate?

In most situations in King County right now, no. Buyers are not offering above a price they believe is already above market. Pricing high typically means fewer showings, longer days on market, and a price reduction that draws lower offers than you would have gotten with accurate pricing from the start.

What happens if I need to reduce my price?

A reduction is not the end of the world, but go in with your eyes open. The first reduction should happen no later than three weeks in if you are getting no offer activity. Each week that passes without an offer makes the next buyer less likely to pay full price for the reduced number. Early and decisive is better than slow and small.

How much does condition affect price in King County?