Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Bellevue Condo Buyer’s Guide 2026: What to Know Before You Buy

The condo you can afford in Bellevue depends far more on the building’s paperwork than on the unit itself. Here is how to read both before you write an offer.

Bellevue is the one Eastside market where a condo can be the smart buy and the risky buy at the same time. The unit looks great. The view is real. Then you pull the HOA documents and find a reserve account that cannot cover the next roof, or a building that no lender will finance with a normal loan. I see this pattern constantly in my valuation work, and it is the single biggest reason Bellevue condo deals fall apart.

This Bellevue condo buyer guide walks you through what actually matters when you buy here in 2026: what you will pay by neighborhood, how to vet an HOA so you do not inherit someone else’s deferred maintenance, the financing trap that catches first-time buyers, and what to inspect that a standard home inspector will skip. The goal is simple. By the end, you should be able to look at a listing and a document packet and know whether it is a deal or a problem dressed up as a deal.

What You Will Actually Pay: Bellevue Condo Prices by Neighborhood

The first thing to understand is that “Bellevue condo prices” is almost a meaningless phrase. The spread between neighborhoods is enormous, and where you shop sets your budget more than anything else you decide.

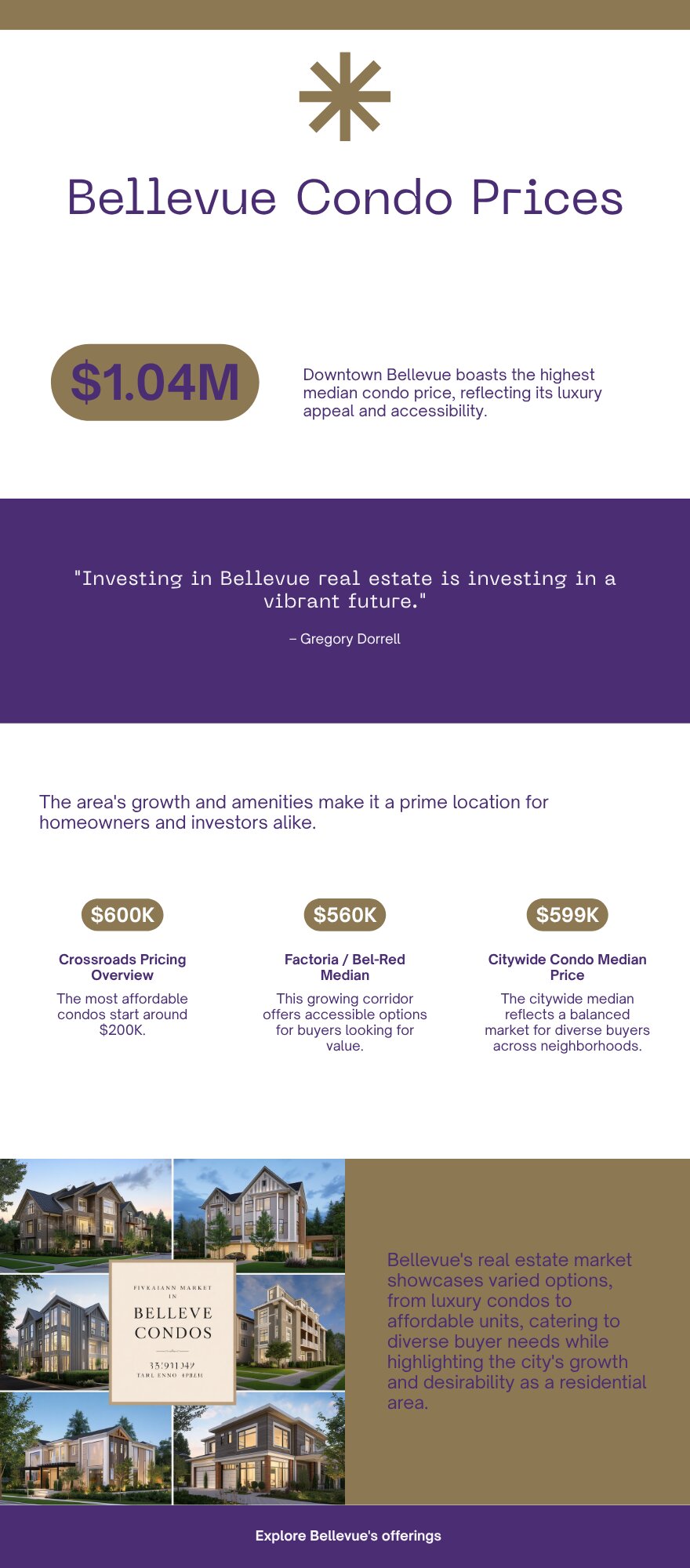

The citywide median condo list price sits around $599,000 in 2026, with roughly 38 days on the market. That number hides a wide range. Here is how the main areas break down.

Downtown Bellevue (98004)

Downtown is the premium play. Median condo list prices here run around $1.04 million, with one-bedroom luxury units near $874,000 and two-bedrooms around $1.65 million. You are paying for walkability, towers with concierge service, and being steps from the new light rail. The 2 Line is opening through downtown Bellevue in 2026, and buildings near the Bellevue Downtown and East Main stations are pricing that access in. What this means for you: downtown is where you go for lifestyle and transit, not for value.

Crossroads

Crossroads is the affordability story in Bellevue. Condos here start under $600,000, and you can still find units in the $200,000s through the $500,000s. For a first-time buyer who wants a Bellevue address and a Bellevue School District zone without a million-dollar mortgage, this is the most realistic entry point. What this means for you: if your budget is under $500,000, Crossroads is probably where your search starts and ends.

Factoria / Bel-Red

Factoria’s condo market starts around $560,000, which makes it another accessible door into the city. The Bel-Red corridor is changing fast as light rail and new development reshape the area, so this is a neighborhood where buying in early could pay off. What this means for you: Bel-Red and Factoria give you a middle path, more space than downtown for less money, with upside as the corridor builds out.

Where you shop sets your budget. Downtown runs near $1M while Crossroads starts under $600K.

One more number that matters: across all closed sales, the average Bellevue condo trades around $496,000. Listings often start higher than they close, especially downtown and in Crossroads where there is more room to negotiate and units sit longer. So do not treat a list price as the price. There is often room to work.

The HOA Is Buying You, Too: How to Vet the Association

Here is the part most first-time condo buyers underestimate. When you buy a condo, you are not just buying a unit. You are buying a share of a small business called the homeowners association, and that business has a balance sheet, debts, and risks. A beautiful unit inside a poorly run HOA is a bad buy.

In Washington, the law is now firmly on your side when it comes to information. Under RCW 64.90, every condo association that is not exempt must maintain a reserve study, update it annually, and get a full professional site inspection at least every third year. The reserve study has to include a 30-year projection, and reserve funds must sit in a segregated account. That is not optional. It is statutory. So if a seller or HOA cannot produce a current reserve study, that itself is a red flag.

When you go under contract, you receive a resale certificate package. Read it like your money depends on it, because it does. Here is what to pull and what to look for.

The reserve study

Confirm it was updated within the last three years and includes the 30-year projection. A reserve study that shows the account is badly underfunded is telling you a special assessment is coming. Someone is going to pay for that roof, those elevators, and that siding. If the reserves are not there, that someone is you.

Twelve to twenty-four months of meeting minutes

This is where the truth lives. Minutes reveal pending litigation, deferred maintenance the board keeps postponing, owner conflict, and any special assessment being discussed. A building can look pristine and still have a lawsuit or a six-figure repair hiding in the minutes.

The budget and delinquency rate

Look at how many owners are behind on dues. If more than 15 percent of owners are over 60 days past due, that alone can make the building hard to finance. High delinquency also means the working budget is stretched thin.

The master insurance policy

Confirm the building carries adequate hazard and liability coverage. Insurance costs have climbed across Washington, and underinsured buildings can face sudden dues increases or assessments.

The paperwork is the deal. Pull all of this before you write an offer.

There is also new protection worth knowing. Senate Bill 5686, effective January 1, 2026, added safeguards around special assessments and assessment-lien foreclosures, including a 30-day notice, a standstill period, and access to a meet-and-confer process. That is good news if you ever fall behind, but it does not change the basic homework. You still want to buy into a building that will never need to lean on those protections.

The Financing Trap: Warrantable vs. Non-Warrantable

This is the one that catches people off guard, and it can blow up a deal at the last minute. Not every condo can be bought with a normal loan.

A warrantable condo is a building that meets Fannie Mae and Freddie Mac standards. When a building is warrantable, you can use a standard conventional loan, including 3 percent down options, plus FHA and VA financing, at normal interest rates. A non-warrantable condo fails one of those tests. When that happens, conventional, FHA, VA, and USDA loans are off the table, and you are pushed into a specialty portfolio loan with a higher rate and usually a bigger down payment.

What makes a building non-warrantable? The common triggers are: a single owner or entity controlling more than 10 percent of the units; too many units owned by investors rather than occupied by owners, since lenders generally want at least 51 percent owner-occupied; reserves that are too thin; more than 15 percent of owners more than 60 days behind on dues; active litigation involving the association, which is common in newer buildings with construction defect claims; or too much of the building’s square footage used for commercial space.

So what this means for you is concrete: before you fall in love with a unit, ask your lender to confirm the building is warrantable. A good loan officer can check the project against Fannie Mae’s Condo Project Manager database quickly. If it comes back non-warrantable, you are not necessarily out, but you need to know going in that your financing, rate, and down payment all change. Walking into that surprise three weeks before closing is how people lose earnest money and homes.

What to Inspect That a Standard Inspector Will Miss

A normal home inspection covers your unit. It does not cover the building, and the building is where the expensive problems live. So your due diligence has to look in two directions at once.

Inside the unit, you want the usual: plumbing, electrical, appliances, windows, and signs of water intrusion, which matters more in our wet climate than almost anywhere. But the bigger questions are about the shared systems you are buying a fraction of. How old is the roof, and is it funded in the reserve study? What is the condition of the siding and the building envelope, which is the single most expensive thing a Pacific Northwest condo can face? When were the elevators, boilers, and shared HVAC last serviced or replaced?

The Local Angle: How Bellevue Condos Differ from the Rest of King County

If you have shopped condos in Kent, Renton, or Auburn, Bellevue will feel like a different sport. A few things set it apart.

First, the price floor is higher. The same dollars that buy a comfortable condo in South King County buy you a smaller unit, or a Crossroads or Factoria address, in Bellevue. That is the tradeoff for the schools, the jobs, and the Eastside location.

Second, HOA dues run higher, especially downtown. A luxury downtown building can charge anywhere from $800 to more than $1,500 a month once you factor in elevators, concierge staff, garages, and amenities. That dues figure is part of your real monthly cost, and it affects how much loan you qualify for. A $1,200 monthly HOA payment is the equivalent of carrying a much larger mortgage. So when you compare a Bellevue condo to a South King County townhome, compare the all-in monthly number, not just the price.

Third, light rail is reshaping value right now. With the 2 Line opening through downtown Bellevue in 2026 and the Bel-Red corridor building out, location relative to a station is becoming a bigger price driver than it has ever been on the Eastside. That cuts both ways. Transit-adjacent units may cost more today, but they also tend to hold value better. If you are buying to stay five to ten years, proximity to a station is worth paying attention to.

What This Means for You as a Buyer

Buying a Bellevue condo in 2026 comes down to three decisions, in this order.

Pick your neighborhood by budget first. If you are under $500,000, you are realistically looking at Crossroads or Factoria, and that is fine. Those are real Bellevue addresses with real Bellevue schools. Downtown is a lifestyle and transit decision, not a value one.

Vet the HOA before you vet the view. Get the reserve study, the minutes, the budget, and the insurance policy, and read them or have someone read them for you. A great unit in a broken HOA is the most common expensive mistake I see.

Confirm financing on the building, not just on you. Get your lender to verify the project is warrantable early. If it is not, decide whether the specialty loan terms still make the deal work before you are emotionally committed.

Do those three things in order and you will avoid almost every condo horror story out there. Skip them and you are gambling.

Read the reserve study before you fall for the view.

Frequently Asked Questions

How much do you need to buy a condo in Bellevue in 2026?

Plan around the citywide median of roughly $599,000, but your real number depends on neighborhood. Crossroads and Factoria condos start in the $500,000s and below, while downtown high-rises run near or above $1 million. Remember to budget monthly HOA dues, which range from a few hundred dollars to more than $1,500, into what you can actually afford.

What is a non-warrantable condo and why does it matter?

A non-warrantable condo is a building that fails Fannie Mae and Freddie Mac standards, often because of too many investor-owned units, thin reserves, high dues delinquency, or active litigation. It matters because you cannot use a standard conventional, FHA, or VA loan to buy one. You would need a specialty loan with a higher rate and larger down payment, so always confirm warrantability before you make an offer.

What HOA documents should I review before buying a Bellevue condo?

Pull the reserve study (updated within the last three years with a 30-year projection), 12 to 24 months of meeting minutes, the operating budget and delinquency rate, the master insurance policy, and any pending special assessments. Washington law requires associations to maintain a current reserve study, so a missing one is a warning sign.

Are Bellevue condos a good investment in 2026?

It depends on the building and the location. Transit-adjacent units near the new 2 Line stations and in the developing Bel-Red corridor are positioned to hold value well. A unit in a financially healthy, warrantable building is a reasonable buy. A cheaper unit in a building with thin reserves or pending litigation can cost you far more later through special assessments.

How much are HOA dues for a Bellevue condo?

Dues vary widely by building. Smaller, simpler buildings charge a few hundred dollars a month, while downtown luxury high-rises with elevators, concierge service, and amenities can run from $800 to more than $1,500 monthly. Always factor the dues into your total monthly housing cost, because lenders count them when calculating what you qualify for.

Should I buy a condo or a townhome in Bellevue?

Condos usually cost less up front and come with shared-building risk through the HOA. Townhomes often have lower or simpler dues but cost more. The right answer depends on your budget, how long you plan to stay, and how much shared maintenance risk you are comfortable taking on. Run the all-in monthly cost on both before deciding.

Your guide to life outside Seattle.

253-350-0045 ·

greg@livingoutsideseattle.com ·

www.livingoutsideseattle.com