Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Two agents. Same house. Two completely different prices. Here’s how to tell which one is right.

Most sellers in King County interview two or three agents before listing. They get a CMA from each one. And more often than not, those CMAs land in different places — sometimes by $20,000, sometimes by $80,000. Then comes the question nobody wants to ask out loud: which agent is actually right?

The answer isn’t always the highest number. And it isn’t always the lowest. It comes down to how each CMA was built, which comps were chosen, and whether the agent is telling you what the market says or what you want to hear.

This guide walks you through how to read a CMA the way a pricing analyst does — what to look for, what to question, and why the methodology behind the number matters as much as the number itself.

What a CMA Actually Is

A Comparative Market Analysis is a written report — sometimes a few pages, sometimes a full presentation — that estimates what your home would sell for on the open market today. An agent prepares it using data from the local MLS: recent sales, current active listings, and homes that went under contract but haven’t closed yet.

The CMA is not an appraisal. It doesn’t carry legal weight and isn’t prepared by a licensed appraiser. But a well-done CMA uses the same core methodology: find comparable sales, adjust for differences, and arrive at a defensible price range. The difference is in who does it and how rigorously.

A CMA is also not a Zestimate. Automated valuation tools are algorithmically generated from public records and don’t account for interior condition, recent renovations, or hyperlocal factors that move prices in King County. They’re a starting point for curiosity, not a basis for pricing your home.

What you’re looking for in a CMA is a specific kind of precision: recent sales that are genuinely similar to your home, adjustments that reflect real market behavior, and a price recommendation with logic you can follow.

The Anatomy of a Good CMA

A complete CMA has five parts — recent closed sales, price adjustments, active listings context, a price range, and days-on-market data. Missing any one of these is a yellow flag.

The Comparable Sales Section

This is the heart of the analysis. A solid CMA uses 3–6 closed sales — homes that actually sold and recorded with the county, not just homes that were listed. Active listings show you the competition; they don’t tell you what buyers actually paid.

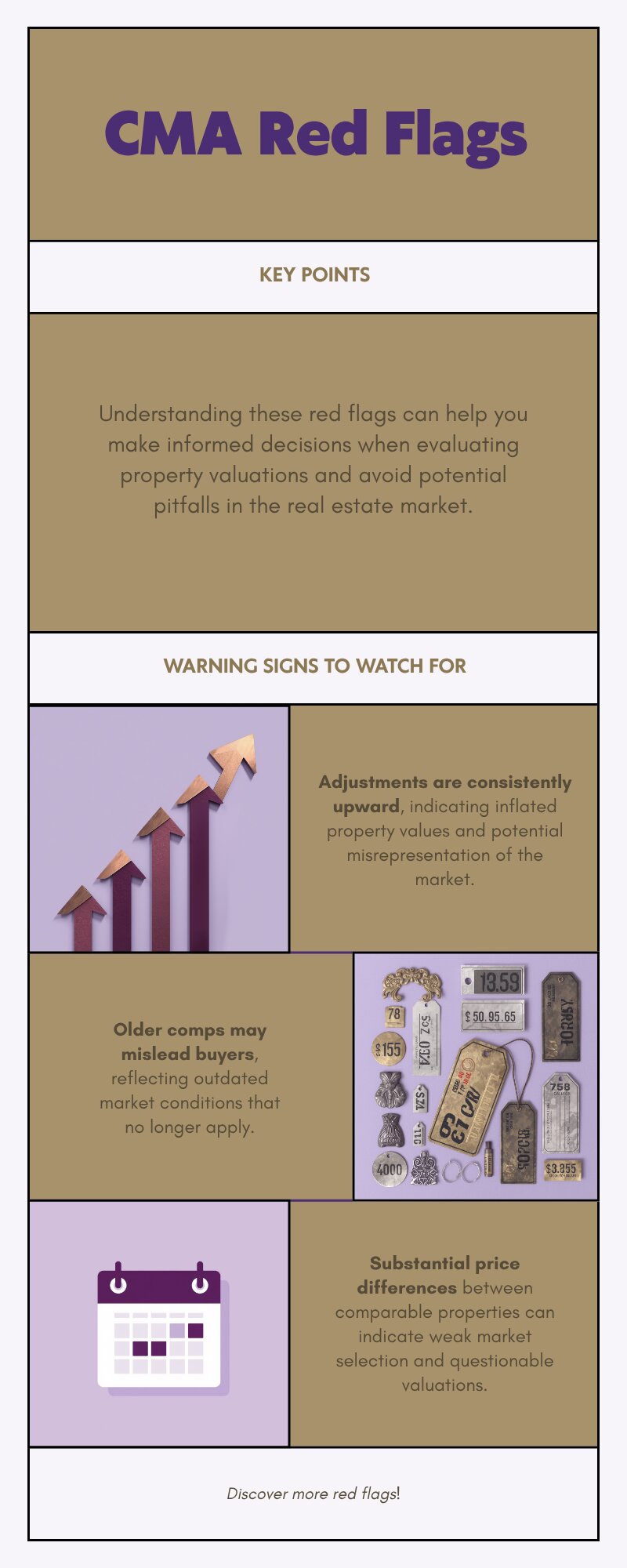

Strong comps are sold within the past 90–180 days, within roughly half a mile in dense neighborhoods, similar in size (within 20%), similar in age and style, and similar in condition. The more adjustments required to bridge the gap between a comp and your home, the less reliable that comp is as an anchor.

The Adjustment Section

Here’s where CMAs diverge. Every comp is adjusted up or down to match your home. If the comp had a three-car garage and yours has one, the agent reduces that comp’s adjusted value. If your home has a finished basement the comp didn’t, an upward adjustment goes in. These adjustments should reflect what buyers in your market actually pay for those features — not round numbers made up on the spot.

Check: Are the adjustments reasonable in proportion to the sale price? Do the comps include some that are better than your home (requiring downward adjustments), or are all adjustments upward? If every adjustment inflates the comp’s value, the CMA may be padded.

Active, Pending, and the Price Range

A complete CMA includes the current competition — what’s on the market now and what’s pending. If similar homes have been sitting for 45 days at your proposed price, that’s a data point worth knowing before you list.

The final output should be a price range, not a single number. Within that range, your agent recommends a specific list price based on your goals and market conditions — and that recommendation should come with a clear explanation. “We can always come down” is not an explanation.

Why Two Agents Give You Different Numbers

Two agents can produce legitimately different CMAs because pricing involves judgment calls — which comps to use, how much to adjust for condition, whether the market is moving up or flat. Reasonable professionals can disagree within a range.

But the real reason sellers often see large gaps between CMAs has nothing to do with analytical disagreement. It’s called buying the listing — when an agent inflates their CMA to win your business. They know you’ll be more excited about the higher number. They sign you up at that price, the home sits, and three weeks later they start asking for a price reduction.

By then, you’ve already lost the prime marketing window — the first two weeks when a new listing gets the most attention from buyers. Homes that require price reductions consistently sell for less than they would have if priced correctly from day one. Buyers notice price cuts. They wonder what’s wrong with the house.

If you see these patterns in a CMA, ask questions before you sign a listing agreement.

The BPO Difference: Why Daily Pricing Work Matters

Most agents prepare CMAs occasionally — when they’re pitching a listing. That means they’re doing this analysis once every few weeks, or less.

My background is different. As an active BPO field agent, I assess property values professionally every single day for banks, lenders, and investment portfolios. That means I’m running the same comp analysis — pulling recent sales, making adjustments, arriving at a reconciled value — on multiple properties every morning. Not when a listing appears on my desk. Every day.

What that produces is calibration. I know what buyers in Renton paid for a renovated kitchen last month because I priced three homes in Renton last month. I know how much a lot size premium is worth in Kent right now because I’ve been tracking it continuously, not revisiting it once a quarter.

When I prepare a CMA for a seller, I’m using the same methodology a lender’s appraiser will use when a buyer’s loan comes through. That alignment matters: a home priced with institutional-grade rigor is much more likely to appraise cleanly at contract price — which means fewer renegotiations and a smoother path to closing. For more on how appraisals interact with your list price, see our guide to how to price your home to sell in King County.

The difference isn’t just credentials — it’s frequency. Daily pricing work produces calibration that occasional CMA preparation can’t match.

What a CMA Can’t Tell You

A CMA is backward-looking. It tells you what buyers paid for comparable homes in the past 90–180 days. It doesn’t tell you what the market will do next month, and it doesn’t account for factors that haven’t shown up in closed sales yet — like a shift in mortgage rates, a wave of new inventory, or a major employer making news in your area.

This is why the agent’s current market knowledge matters as much as the data itself. A CMA prepared by someone who isn’t actively watching the King County market day-to-day will miss signals that a daily practitioner picks up on. Always ask the agent: “Has anything happened in the past 30 days that your comps don’t reflect?” Their answer will tell you whether they’re watching the market or just pulling data.

The King County Specifics Worth Knowing

Sub-market pricing is everything. King County covers an enormous range of price points and market conditions. Renton, Kent, Auburn, Covington, and Maple Valley each behave differently from each other and from the Eastside. A good CMA uses comps from the same sub-market — not comps from a neighborhood three cities over that happens to have similar square footage.

Median prices shifted in early 2026. The April 2026 King County median home sale price came in around $835,000 — down roughly 7.5% year-over-year at the county level, though South King County remained more competitive than average. Comps from 12+ months ago may overstate what your home will actually trade for today. An agent who’s pulling year-old data to support a high price isn’t serving your interests.

Days on market is now a meaningful signal. King County homes are averaging around 12 days on market — up from 7 days a year ago. That shift means the “price it high and wait for the right buyer” strategy is riskier than it was in 2022. Buyers have more options, and a home that sits past 30 days starts raising questions that a price cut can’t fully answer.

School district boundaries move prices. In cities like Newcastle that straddle multiple school district zones, a half-mile difference in location can produce a meaningful price difference. Your agent needs to know which side of those lines your home is on — and make sure the comps are on the same side. For more on what goes into getting your home ready to sell, see our guide on how to prepare your home for sale in King County.

Questions to Ask at Your Listing Appointment

When you sit down with an agent to review their CMA, bring these questions:

On the Comps

Why did you choose these specific sales and not others? How recent are they — and are there more recent sales you considered and rejected? How similar is this comp in size, condition, and location to my home?

On the Adjustments

How did you arrive at the adjustment amounts? Are any of your comps adjusted up by more than 20%? Are there any comps where you made downward adjustments, or are all adjustments upward?

On the Pricing Recommendation

What’s your recommended price range, and where do you suggest we list within it? What happens to our negotiating position if we list at the top of your range and don’t get an offer in two weeks? How does your recommended price compare to what a buyer’s lender will appraise it at?

On the Agent

How many pricing analyses have you done in the past 30 days in this specific sub-market? Have you seen any recent shifts in buyer behavior that your closed comps don’t yet capture?

The agent who answers these questions clearly — without hesitation, without pivoting to their marketing plan — is the agent who did the work.

Frequently Asked Questions

How much does a CMA cost?

A CMA from a real estate agent is free. Agents prepare them as part of their listing pitch. If you want an independent opinion not tied to a listing relationship, a licensed appraiser will charge $600–$900 for a formal appraisal.

Is a CMA the same as an appraisal?

No. A CMA is prepared by a real estate agent and used to set a listing price. An appraisal is prepared by a state-licensed appraiser, required by lenders, and used to determine the maximum loan amount. A home can be listed above its likely appraisal value — which creates problems at closing when the buyer’s lender won’t fund the gap.

How many comps should a good CMA include?

Typically 3–6 closed sales, plus 2–4 active or pending listings for competitive context. Fewer than 3 sold comps is a thin basis for a pricing recommendation. More than 8 often means the agent is padding with weak matches to justify a predetermined number.

What if two CMAs are far apart?

Ask each agent to walk you through their comps side by side. The differences usually come down to which comps were selected and how adjustments were applied. If one agent can’t explain their methodology clearly, that tells you something about how they prepared the analysis.

Should I always list at the top of the CMA range?

Only if your goals and market conditions support it. In a market where homes are selling in 7–12 days, pricing at the midpoint of the range often generates more competing offers than pricing at the top — and can produce a higher net sale price. Your agent should walk you through the trade-offs before you decide.

Getting a CMA is easy. Getting a CMA you can actually trust — one built with the same rigor a lender’s appraiser will apply to the same property in 60 days — takes a different kind of preparation. And knowing how to read one puts you in a position to tell the difference.

Your guide to life outside Seattle.

253-350-0045 ·

greg@livingoutsideseattle.com ·

www.livingoutsideseattle.com