Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

The Real Cost of Waiting to Buy a Home in King County in 2026

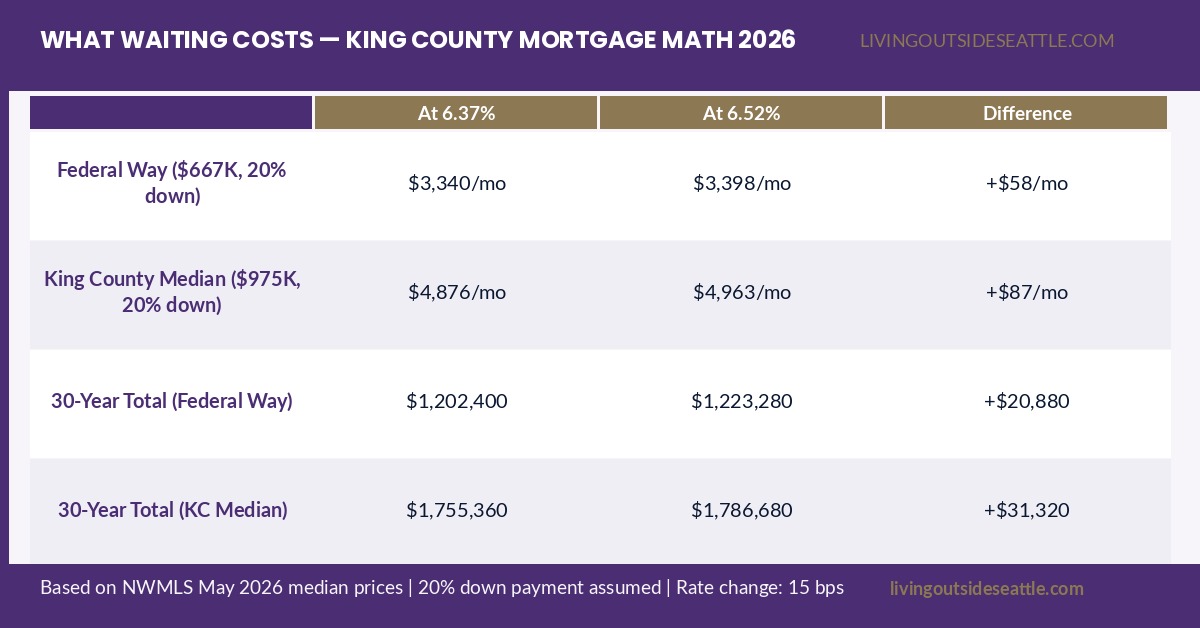

Mortgage rates were 6.37% in early May. As of the first week of June they’re at 6.52%.

That’s a 15-basis-point increase in one month. If you’ve been waiting for rates to drop before buying a home in King County, the math on that decision has gotten worse, not better.

Here’s what the numbers actually look like.

The Monthly Payment Math at Today’s Rates

Let’s use Federal Way as the example, because it’s the most relevant market for buyers who are rate-sensitive and making value-driven decisions. Federal Way’s residential median in May 2026 was $667,475.

With 10% down, your loan is approximately $600,727.

On a $975,000 King County residential median with 20% down ($780,000 loan): at 6.37% that’s $4,874/month; at 6.52% that’s $4,943/month — $69 more per month, $2,070 per year.

These numbers sound small. They’re not. At already-stretched affordability levels, every basis point matters for buyers right at the edge of qualification. And this is a one-month move.

What Waiting Six Months Actually Costs

The “wait for rates to drop” calculation has to account for three things that most buyers don’t put together at the same time: what rates might do, what prices might do, and the rent you continue paying while you wait.

The rate outlook. No major forecaster is projecting the 30-year fixed below 6% before late 2026, and even that assumes a Fed cut in September that isn’t guaranteed. Wells Fargo, Fannie Mae, and the Mortgage Bankers Association all have consensus projections in the 6.2% to 6.5% range through Q3. Waiting six months and finding rates are still at 6.4% is a real possibility.

The price outlook. The King County residential median is $975,000, up 1.2% from a year ago even in this environment. County-wide prices have not collapsed despite all the inventory building and national headline anxiety. Waiting for prices to fall while paying rent is a bet that may not pay off. If prices hold flat and rates hold flat, the only thing waiting costs you is rent.

The rent clock. The median asking rent in King County for a two-bedroom unit is approximately $2,200 to $2,600 depending on location. If you’re paying $2,400 a month in rent and you wait six months to buy, that’s $14,400 out the door with nothing to show for it on a balance sheet.

The buyer who waits six months hoping for a rate drop that doesn’t come has spent $14,400 in rent, is now looking at the same or slightly higher rates, and has the same or slightly higher purchase price to deal with.

The Federal Way Math Specifically

Federal Way is where the cost-of-waiting conversation is most acute right now. Here’s why.

The city’s +5.1% year-over-year price growth in May is being driven in part by buyers who are migrating south from Renton and Kent because Federal Way gives them more house per dollar. That migration trend is active right now. The buyers who wait six months to see if that trend reverses may be walking into a market where Federal Way inventory has tightened further and prices have continued their upward move.

At $667,475 with 10% down and a rate of 6.52%, your monthly payment on principal and interest is $3,814. Add property taxes (approximately $5,500 to $7,000 per year in Federal Way, so $458 to $583 per month), homeowner’s insurance ($125 to $175 per month), and you’re looking at a total monthly housing cost of approximately $4,400 to $4,570.

If you’re currently renting at $2,200 to $2,400 a month, the buy side is meaningfully more expensive on a monthly basis. That’s the honest picture. Buying is not automatically cheaper than renting in today’s market. What it gives you is equity accumulation, inflation protection on your housing cost, and a locked-in payment that doesn’t increase when rents go up.

See also: Rent vs Buy in Federal Way WA 2026: The Real Cost Breakdown.

What Waiting Does Make Sense

I’m not arguing that every renter in King County should buy immediately regardless of circumstances. There are real situations where waiting is the right call.

If your employment situation is uncertain, this is not the time to lock in a $4,000+ monthly commitment. Job stability matters more than rate optimization.

If you haven’t saved a down payment and closing costs, you’re not ready to buy yet regardless of rates. Rushing into a purchase without adequate reserves is one of the most common and painful financial mistakes first-time buyers make.

If you’re planning to move within three years, the transaction costs of buying and selling within a short window often erase any equity gains. The three-year rule of thumb still applies: you need to plan to stay at least three years for buying to make financial sense over renting.

But if you’re stably employed, have your down payment ready, and plan to stay for five or more years, the cost-of-waiting math is working against you right now. Not dramatically. But consistently.

Frequently Asked Questions

Should I buy a home now or wait for rates to drop in King County?

If you’re stably employed, have a down payment ready, and plan to stay 5+ years, the math currently favors buying. Rates rose from 6.37% to 6.52% in one month. Every month you rent at $2,200 to $2,600 is money that builds no equity. Rate forecasts for Q3 2026 project 6.2% to 6.5%, not a dramatic drop. Waiting makes sense if your job is uncertain, you haven’t saved reserves, or your timeline is under 3 years.

How much does mortgage rate impact monthly payment in King County?

On the $975,000 King County SFR median with 20% down (a $780,000 loan), every 0.25% change in rate is approximately $135/month. Going from 6.25% to 6.5% costs $1,620 more per year. On a Federal Way home at $667,475 with 10% down ($600,727 loan), each 0.25% swing is about $97/month.

Are King County home prices expected to drop in 2026?

County-wide, the residential median is $975,000, up 1.2% year over year as of May 2026. A dramatic price collapse is not in the forecast — Washington State’s structural housing undersupply limits how far prices can fall even in a softer environment. The declines visible in Sammamish and Issaquah are luxury-segment corrections, not a county-wide collapse.

What is the minimum down payment to buy a home in Federal Way WA?

Conventional loans typically require 3% to 20% down depending on the loan type. On Federal Way’s $667,475 median: a 3% down payment is $20,024 (plus PMI); a 10% down payment is $66,748; a 20% down payment is $133,495. First-time buyers in Washington may also qualify for WSHFC Home Advantage down payment assistance programs.

Ready to Run Your Numbers?

The “should I buy now or wait” question is worth doing with a real calculator and real local data, not a national article. I’m happy to run a side-by-side analysis for your situation: what buying looks like today versus what waiting six or twelve months might cost.

Your guide to life outside Seattle.

253-350-0045 ·

greg@livingoutsideseattle.com ·

www.livingoutsideseattle.com