Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

When you’re paying $2,800 a month in rent, the question gets loud: wouldn’t I be better off putting that toward a mortgage in Federal Way?

Rent disappears. A mortgage builds equity. The math should be simple.

It’s not simple. But it’s not complicated either. Here’s what the numbers actually look like, using real Federal Way prices and March 2026 mortgage rates.

Federal Way Home Prices 2026: Condo vs. Mortgage Cost Breakdown

Start with a Federal Way condo. The median price in March 2026: $637,500.

Monthly payment with 10% down, which is realistic for a first-time buyer:

Down payment: $63,750. Loan: $573,750. At 6.38% (the rate as of late March 2026), principal and interest runs roughly $3,580 per month.

That’s not your full housing cost. Add:

Property taxes: King County annual property tax runs roughly 0.94% of value. On a $637,500 condo, that’s about $5,990 per year, or $475 per month.

HOA fees: Federal Way condos typically run $300 to $400 per month. Call it $350.

Homeowners insurance: roughly $100 to $150 per month.

Total: $3,580 (P&I) + $350 (HOA) + $475 (taxes) + $125 (insurance) = approximately $4,530 per month.

Your rent: $2,800.

Month one, you’re spending more as an owner. Noticeably more.

The Common Mistake When Comparing Rent to Buy in Federal Way

Most renters stop at that monthly gap and decide buying is too expensive.

Month one, two, three — you are spending more. That part is true.

But you’re not just spending that money. You’re building something with it.

How Federal Way Home Equity Builds While You Pay Rent

At 6.38% on a $573,750 loan, roughly $814 of your first payment goes toward principal. By end of year one, you’ll have paid down roughly $9,768. That’s money you get back when you sell. A renter gets zero.

Over 30 years, the vast majority of that $3,580 P&I payment becomes equity. Your rent payment? Gone every month. Forever.

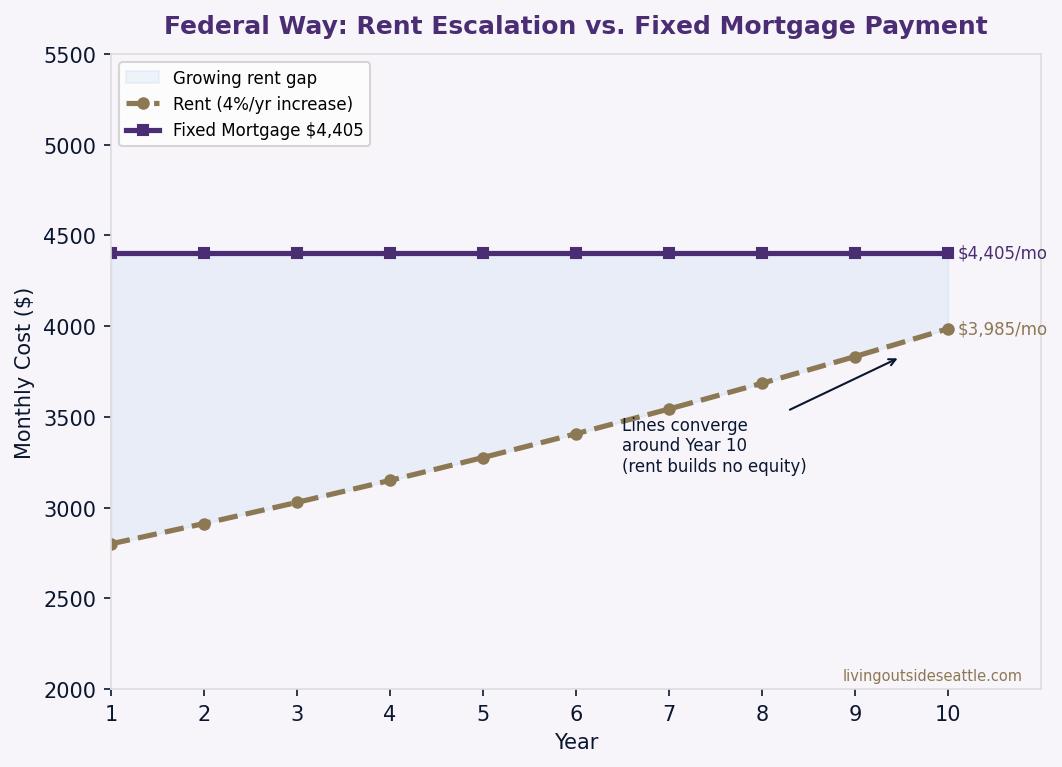

Federal Way Rent Increases vs. a Fixed Mortgage Payment

Here’s what actually shifts the math for long-term renters.

Federal Way rent increases 3% to 5% per year. Here’s what that looks like at 4% annually:

By year 10, you could be paying $4,149 in rent with nothing to show for it. A Federal Way homeowner at that same point has paid down roughly $80,000 in principal and owns an asset worth more than $637,500.

Buying a Single-Family Home in Federal Way: A Cheaper Path

What if you buy a house instead of a condo?

The Federal Way single-family median in March 2026: $686,500. Put 20% down to avoid PMI. That’s $137,300 down, leaving a $549,200 loan.

Principal and interest: roughly $3,425 per month. Property taxes: about $490 per month. Insurance: roughly $130 per month. No HOA. No PMI.

Total: $4,045 per month.

Cheaper than the condo path, and you get a single-family home. Still more than $2,800 rent, but the gap is narrower. The trade-off: you need $137,300 down instead of $63,750.

For a full picture of Federal Way neighborhoods and what each area offers buyers, see the Living in Federal Way WA: 2026 real estate and lifestyle guide.

Should You Rent or Buy in Federal Way? Who Should Buy Now

Buying makes sense if you’re planning to stay 5 or more years, have a stable income and sufficient down payment, and want to build equity instead of paying someone else’s mortgage. The monthly gap between renting and owning narrows as rent increases each year.

Renting still makes sense if you’re moving in 3 years or less. Closing costs and transaction fees on both sides of a sale can eat your equity on a short hold.

One more comparison worth making: Seattle one-bedroom apartments in decent neighborhoods run $3,200 to $3,500 per month. Against those numbers, a $4,530 Federal Way mortgage looks a lot closer to what you’d already be paying.

Federal Way Rent vs Buy FAQs

Is it cheaper to rent or buy in Federal Way WA in 2026?

Month-to-month, renting at $2,800 is lower than the $4,045 to $4,530 mortgage payment. But rent typically increases 3% to 5% annually while your mortgage stays fixed. By year 10, Federal Way rent at 4% annual growth reaches $4,149 per month, while your mortgage hasn’t moved. And each mortgage payment builds equity. Rent builds nothing.

What is the typical mortgage payment on a Federal Way home in 2026?

Based on March 2026 rates of 6.38%, a $637,500 Federal Way condo with 10% down runs roughly $4,530 per month including principal, interest, HOA, taxes, and insurance. A single-family home at $686,500 with 20% down costs approximately $4,045 per month with no HOA. Both figures use King County property taxes of roughly 0.94% annually.

How much equity do you build in the first year of a Federal Way mortgage?

In year one, approximately $814 per month of your $3,580 P&I condo payment goes toward principal. By end of year one, you’ve paid down roughly $9,768. Renters get nothing back. Over time, equity compounds as your loan balance shrinks and home value grows.

What are the hidden costs of buying in Federal Way that renters don’t pay?

Beyond your monthly mortgage, expect property taxes (roughly $5,990 per year on a $637,500 condo), homeowners insurance ($1,200 to $1,800 per year), maintenance and repairs (budget 1% of home value annually), HOA fees for condos ($3,600 to $4,800 per year), and PMI if putting down less than 20%. Total annual costs beyond principal and interest can run $15,000 to $25,000. Renters avoid most of these, which is why the 5- to 10-year picture matters more than the monthly comparison.

What’s the median home price in Federal Way WA in 2026?

The median single-family home price in Federal Way as of March 2026 is $686,500. The median condo price is $637,500. Prices are up roughly 6.7% compared to early 2025.

Your guide to life outside Seattle.

Coldwell Banker Bain | WA License #111862

253-350-0045

·

greg@livingoutsideseattle.com

·

www.livingoutsideseattle.com

Gregory Dorrell is a REALTOR® with Coldwell Banker Bain specializing in East and South King County. This post is for informational purposes and not an offer of real estate services. All market data as of March 2026.