Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Capital Gains on Home Sales in Washington State: What King County Sellers Need to Know

Most King County sellers I work with are sitting on a lot of equity. A home bought in Sammamish for $450,000 in 2015 might be worth $850,000 today. That’s $400,000 in gains. The first question I get when we start talking about selling is almost always: “How much of that do I owe in taxes?”

The answer depends on a few specific things. Here’s exactly how capital gains work on a home sale in Washington state, in plain language, including the one tax every seller pays that most people forget about.

What Capital Gains on a Home Sale Actually Means

Capital gains are the profit you make when you sell an asset for more than you paid for it. On a house, that means the sale price minus what you originally paid, minus the cost of improvements you made, minus selling costs.

If you bought your Kent home for $520,000 and sold it for $780,000, your gross gain is $260,000. But before you panic, there is a federal exclusion that wipes out most or all of that for the majority of sellers.

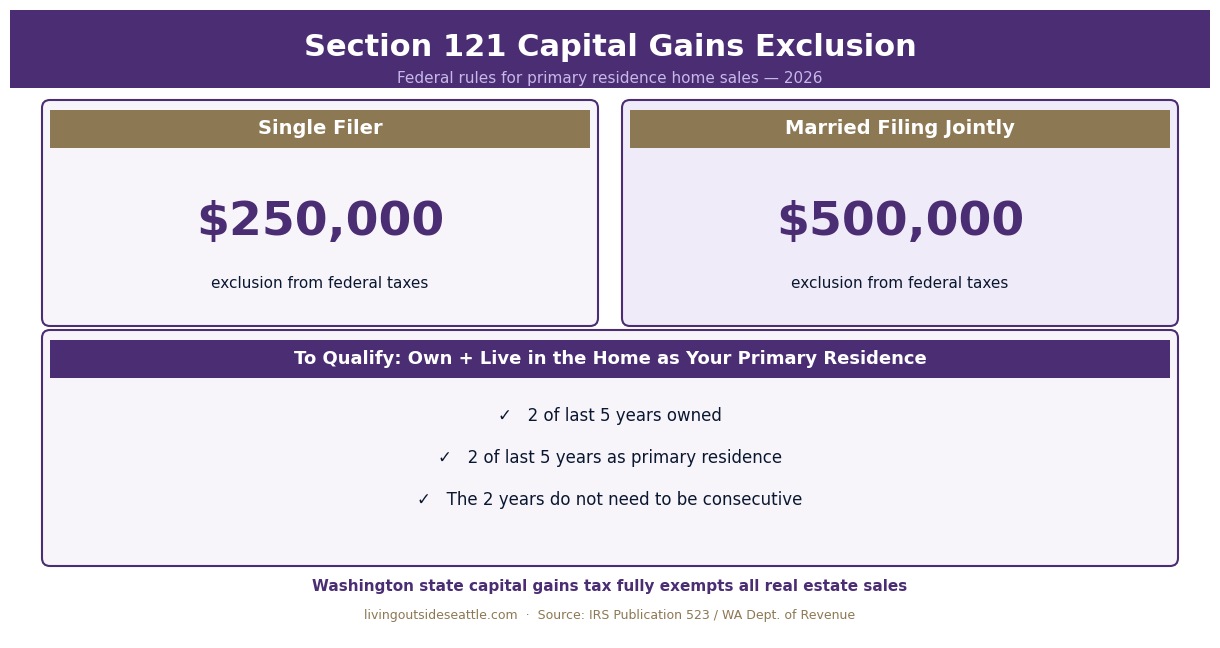

The Section 121 Exclusion: The $500,000 Rule

The IRS gives homeowners a major break called the Section 121 exclusion. Here’s how it works.

If you’re married filing jointly, you can exclude up to $500,000 in capital gains from your taxable income. If you’re single, the exclusion is $250,000.

To qualify, you need to meet two tests:

- Ownership test — You must have owned the home for at least two of the last five years before the sale.

- Use test — You must have lived in the home as your primary residence for at least two of the last five years. Those two years don’t have to be consecutive.

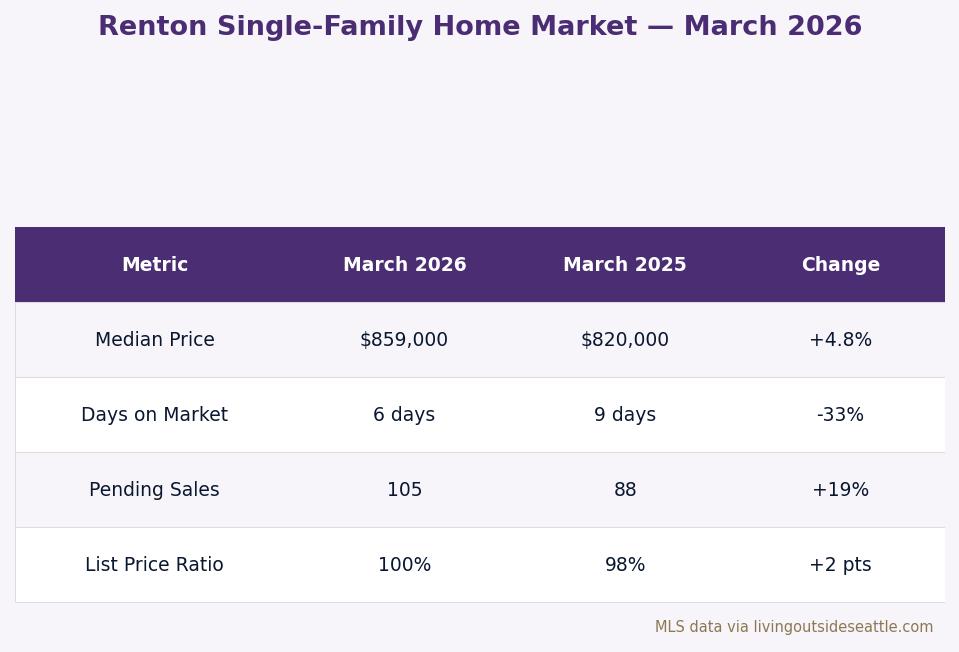

Most long-term King County homeowners qualify easily. If you’ve lived in your Renton home for five years, you almost certainly clear both tests.

What this means practically: if you bought your Auburn home for $400,000, made $30,000 in improvements, and sold for $750,000, your gain is $320,000. If you’re married and file jointly, you exclude all $320,000 under the $500,000 cap. You owe zero federal capital gains tax on the sale.

What Counts as Your Cost Basis

Your cost basis is not just the purchase price. It includes several things that reduce your taxable gain.

The original purchase price is the starting point. Add to that any capital improvements you made over the years. A new roof, an addition, a kitchen remodel, a finished basement, new HVAC — these all increase your basis. Routine maintenance and repairs do not count, but anything that adds value or extends the life of the home does.

You can also add your original closing costs from when you bought the house. Title insurance, loan origination fees, and legal fees paid at purchase are all part of your basis.

On the selling side, your agent commission, title and escrow fees, staging costs, and any seller-paid closing costs reduce your net proceeds, which lowers your effective gain.

Washington State Capital Gains Tax: What You Need to Know

Washington passed a 7% capital gains excise tax on long-term gains above $250,000, effective January 1, 2022. But here’s the key detail most sellers don’t realize: real estate is fully exempt from Washington’s capital gains tax.

That means when you sell your primary home in King County, you owe no Washington state capital gains tax — not just on primary residences, but on all real property. The state capital gains tax targets stocks, bonds, and other capital assets, not real estate.

This is important news for King County sellers. You do not need to factor the 7% state capital gains tax into your home sale math at all.

For more on what you’ll net from the sale after all costs: selling a home in King County — costs and net proceeds breakdown

Washington’s Real Estate Excise Tax: The Tax Every Seller Pays

Here is the one tax that often surprises sellers because it’s separate from capital gains entirely. Washington state charges a Real Estate Excise Tax (REET) on every property sale. This is a tax on the transaction itself, not on your profit.

Washington’s REET uses a graduated rate structure based on the sale price:

| Sale Price Range | State REET Rate | King County Local |

|---|---|---|

| Up to $525,000 | 1.10% | + 0.50% |

| $525,001 – $1,525,000 | 1.28% | + 0.50% |

| $1,525,001 – $3,025,000 | 2.75% | + 0.50% |

| Above $3,025,000 | 3.00% | + 0.50% |

Source: Washington Department of Revenue. Rates current as of 2026.

On a $800,000 home sale in King County, your combined REET bill works out to roughly $11,000 to $12,000. This comes out of your proceeds at closing. It is not optional and it does not depend on whether you made a profit.

When You Might Owe Federal Capital Gains Tax

For most King County sellers, the Section 121 exclusion eliminates the federal tax bill. But there are situations where you could owe something.

Your gains exceed the exclusion. If you’re single and your gain is $400,000, you owe tax on $150,000 — the amount above the $250,000 exclusion. In King County’s high-appreciation market, this is more common than people expect, especially for long-term owners in Bellevue, Sammamish, or Issaquah who bought in the early 2000s.

You don’t meet the use-and-ownership tests. If you haven’t lived in the home as your primary residence for at least two of the last five years, you don’t qualify for the exclusion. This comes up with rental properties that were previously a primary residence, or vacation homes.

You’re selling an investment property. The Section 121 exclusion does not apply to rentals or investment properties. You’d owe federal capital gains tax at 0%, 15%, or 20% depending on your income and holding period.

Depreciation recapture on rentals. If you converted a primary residence to a rental at some point, any depreciation you claimed gets recaptured as ordinary income when you sell. This catches people off guard.

For inherited property situations: inherited home King County — what to do with an inherited property

Short-Term vs. Long-Term Capital Gains Rates

Federal capital gains rates depend on how long you owned the property before selling.

If you owned the home for one year or less, gains are taxed as ordinary income — potentially 22%, 24%, or higher. This rarely applies to primary residence sales but matters for investors who flip quickly.

If you owned the home for more than one year, gains qualify for long-term rates: 0%, 15%, or 20% depending on your taxable income. For most middle-income King County households, the rate is 15%.

Nearly every homeowner selling a primary residence after living there for two-plus years is in long-term territory.

A Practical Example for a King County Seller

Here’s how this plays out for a scenario I see often. A couple bought their Sammamish home in 2014 for $620,000. They’ve lived there since and are now looking to downsize. The home is worth $1,100,000 today.

| Item | Amount |

|---|---|

| Sale Price | $1,100,000 |

| Cost Basis (purchase + improvements) | $665,000 |

| Gross Gain | $435,000 |

| Section 121 Exclusion (married filing jointly) | $500,000 |

| Federal Capital Gains Tax Owed | $0 |

| WA State Capital Gains Tax Owed | $0 (real estate exempt) |

They will still owe REET at closing — approximately $16,000–$17,000 on a $1.1M sale in King County.

What to Do Before You Sell

Talk to your CPA or tax advisor before you list, especially if you’re near or above the exclusion thresholds, have ever rented the home, or inherited the property. Every situation is different.

What I can do is help you understand your equity position and what you’re likely to net from the sale based on current market values. I assess property values across King County every day as part of my BPO work for institutional clients — that same analysis tells me exactly where your home stands in today’s market before we set a price.

For timing guidance: best time to sell a house in King County — timing the market

Frequently Asked Questions

Do I have to pay capital gains tax when I sell my house in Washington state?

Most sellers don’t. If you’ve owned and lived in your home for at least two of the last five years and your gain is under $500,000 (married) or $250,000 (single), the Section 121 exclusion eliminates your federal capital gains tax. Washington state’s capital gains tax fully exempts real estate, so there’s no state capital gains tax on home sales regardless.

What is Washington’s Real Estate Excise Tax and do I have to pay it?

Yes. REET is a transaction tax paid by the seller on every property sale in Washington state. It is calculated on the sale price using a graduated rate structure ranging from 1.1% to 3.0% at the state level, plus a local rate in King County cities of 0.50%. There is no exemption for primary residences — every seller pays it at closing.

How do I calculate my cost basis for a home sale?

Start with your original purchase price. Add capital improvements (renovations, additions, major systems replacements) and your original closing costs from when you bought. The total is your adjusted basis. A higher basis means a lower taxable gain.

What if my home sale gain is more than $500,000?

You’d owe federal long-term capital gains tax — typically 15% for most households — on the amount above the exclusion. A married couple with a $650,000 gain would owe tax on $150,000. Talk to a CPA about strategies like documenting additional improvements to increase your basis before listing.

Does Washington’s 7% capital gains tax apply to my home sale?

No. Washington’s capital gains excise tax fully exempts all real estate transactions. It applies to stocks, bonds, and other capital assets — not to property sales of any kind.

Gregory Dorrell is a licensed real estate broker (WA License #111862) with Coldwell Banker Bain. He is not a tax attorney, CPA, or licensed tax advisor. The information in this post is provided for general educational purposes only and does not constitute tax or legal advice.

Every seller’s tax situation is different. Before making any decisions based on the information in this post, please consult a licensed CPA or tax attorney about your specific situation — including any tax consequences of your home sale and strategies that may help minimize the amount you owe.

Tax laws change. The information above reflects general rules as of 2026 and may not account for changes in federal or state tax law, your individual income, filing status, or other factors specific to your situation.

Your guide to life outside Seattle.

Coldwell Banker Bain | WA License #111862

253-350-0045

greg@livingoutsideseattle.com

www.livingoutsideseattle.com