Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

You’ve been pre-approved. Now the lender is asking which loan type you want. Suddenly the decision feels a lot bigger than you expected.

Most first-time buyers in King County hear the words “FHA” and “conventional” and assume they’re basically the same thing with different names. They’re not. The loan type you choose affects your monthly payment, how much cash you bring to closing, how competitive your offer looks to sellers, and how much you pay over the full life of the loan. In a market where the median home price in Renton, Kent, and Auburn is pushing $600,000, those differences add up to real money.

I’ve helped buyers work through this decision dozens of times. Here’s what actually matters for King County buyers specifically, not just a generic national comparison.

What FHA and Conventional Loans Actually Are

FHA loans are insured by the Federal Housing Administration. Because the government backs them, lenders can offer them to buyers with lower credit scores and smaller down payments than they’d otherwise accept. You’re not borrowing from the government. You’re borrowing from a regular lender, but that lender has a government safety net if you default.

Conventional loans have no government backing. They’re sold to Fannie Mae or Freddie Mac after closing, which means they follow stricter underwriting rules. That strictness cuts both ways: harder to qualify for, but cheaper to carry over time if you do qualify.

The most important thing to understand is that these two loan types are not interchangeable. They’re designed for different financial situations.

The Down Payment Reality in King County

Both loan types have low down payment options, but they work differently.

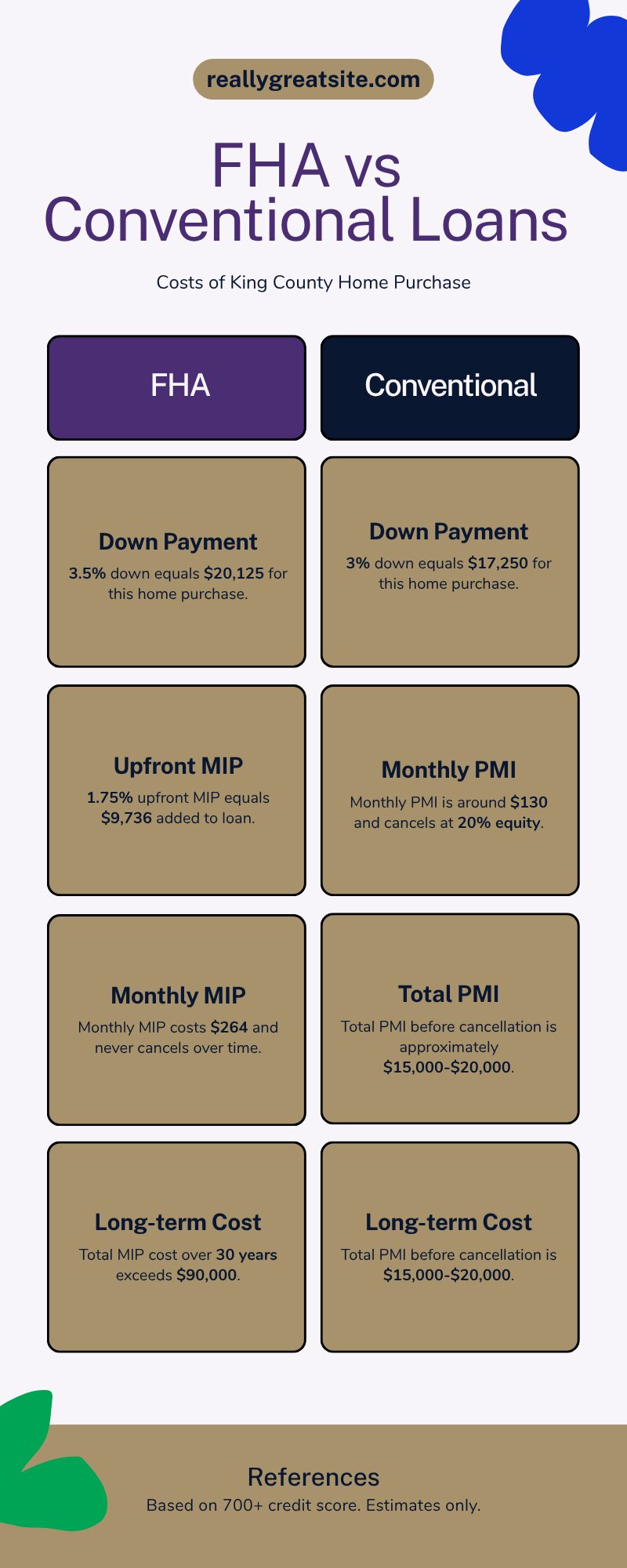

FHA requires 3.5% down if your credit score is 580 or above. On a $575,000 home — a realistic entry-level price in South King County right now — that’s about $20,125 down. If your score is between 500 and 579, you need 10% down.

Conventional loans have a 3% down option through the Fannie Mae HomeReady or Freddie Mac Home Possible programs. On that same $575,000 home, 3% down is $17,250. The catch: you generally need a credit score of 620 or higher to qualify at all, and the best conventional PMI rates kick in at 700 and above.

So on paper, conventional actually asks for less at closing. But the mortgage insurance story is where the real cost difference shows up, and it’s significant.

FHA mortgage insurance stays for the life of the loan. Conventional PMI cancels at 20% equity — a difference of $70,000+ over 30 years on a typical King County purchase.

Mortgage Insurance: This Is Where the Numbers Diverge

This is the part most buyers don’t understand until it’s too late to change their loan type.

FHA Mortgage Insurance

You pay two premiums. First, there’s an upfront MIP of 1.75% of the loan amount. On a $575,000 purchase with 3.5% down, that’s about $9,736 rolled into your loan balance. Then you pay a monthly MIP for the life of the loan (roughly 0.55% annually on most King County FHA loans).

It does not go away when you hit 20% equity. To eliminate it, you’d have to refinance into a conventional loan.

Conventional PMI

You only pay it if your down payment is under 20%. Once you reach 20% equity through paying down the balance, appreciation, or some combination, you can request cancellation. The lender is required to cancel it automatically at 22% equity. PMI rates for borrowers with 700+ credit scores typically run 0.25%–0.50% annually.

In King County’s appreciating market, PMI commonly cancels within 7–10 years.

Here’s what that means in real numbers on a $555,000 loan (3.5% down on a $575,000 purchase):

FHA: Total MIP over 30 years = approximately $90,000+ including upfront and monthly premiums

Conventional (5% down, 700 credit): Total PMI before cancellation = approximately $15,000–$20,000

That difference is not a rounding error. It’s a second car. It’s a college fund start. For a buyer with a 700+ credit score, conventional wins by a wide margin over any hold period longer than 5 years.

Credit Score: The Practical Dividing Line

Here’s the simplest way to frame the credit score question. For a deeper look at what your payment actually looks like at current rates, see King County Mortgage Rates 2026: What Buyers Are Actually Paying — it walks through the real payment math before you commit to either loan type.

Below 620

FHA is likely your only realistic option. Conventional lenders rarely approve below 620, and when they do, the rates and PMI costs are punishing.

620–700: The Gray Zone

You can qualify for conventional, but your PMI rate will be higher than for buyers with stronger scores. Run the actual numbers with your lender for both options. FHA may still win in the short term, but conventional saves money if you stay put.

700 and Above

Conventional wins, almost without exception. PMI rates at this tier are low (often 0.30%–0.35%), cancel within 7–10 years in King County’s appreciating market, and you avoid the permanent FHA MIP entirely.

I see this play out constantly in my BPO work. I’m assessing home values in Renton, Kent, and Covington every week, and the buyers who positioned themselves for conventional financing at purchase are the ones who refinanced without drama and built equity fastest. The upfront credit work pays off.

Loan Limits in King County: More Room Than You Think

One of the biggest misconceptions about FHA loans is that they’re only for “affordable” homes. In King County, that’s not true.

For 2026, the FHA loan limit in King County is $1,063,750 for a single-family home. That covers the vast majority of purchase prices in Renton, Kent, Auburn, Covington, Maple Valley, and most of the South King County communities I work in regularly. You don’t have to be buying a starter home to use FHA financing here.

The conventional conforming loan limit in King County for 2026 is $1,063,750, also well above the local median price. Both loan types give you plenty of room in this market.

If your loan amount exceeds either of those limits, you’re looking at jumbo financing, which is a separate conversation entirely.

Both loan types cover the vast majority of purchase prices in South and East King County. You don’t need to buy a starter home to use FHA financing here.

How Each Loan Type Plays With Sellers

This is a real consideration in King County’s competitive pockets, and I want to be honest with you about it.

FHA offers historically faced more seller skepticism than conventional offers, for two reasons. First, FHA appraisals have stricter condition requirements. The appraiser flags health and safety issues that can hold up or kill a deal. Second, FHA loan closings occasionally take longer than conventional.

In 2025 and into 2026, the market in South and East King County has moderated from the frenzy of prior years. In many neighborhoods, Kent, Auburn, Covington, and Maple Valley among them, sellers are no longer in a position to pick and choose between five cash offers. An FHA offer paired with a strong pre-approval letter, a fast lender closing commitment, and solid earnest money is competitive.

That said, if you’re targeting a specific high-demand price point where multiple offers are common (certain Renton zip codes, for example), your agent should discuss this with you before you go in with FHA. In those situations, conventional financing strengthens your position.

The King County Angle: Stacking DPA With Either Loan Type

Here’s something that can change the whole picture for South King County buyers: the Washington State Housing Finance Commission (WSHFC) offers down payment assistance programs that work with both FHA and conventional loans.

The Home Advantage DPA program provides up to 4% of the loan amount as a 0% interest, deferred second mortgage. There are no payments until you sell, refinance, or pay off the home. That’s potentially $22,000–$38,000 on a typical King County purchase, which can cover your entire down payment and a chunk of closing costs. If you’re on a conventional loan, the DPA steps up to 5% of the loan amount.

The Opportunity DPA program offers up to $15,000 at 1% interest, also deferred for 30 years.

Both programs have income limits (typically $145,000–$180,000 for King County depending on household size and program), and both require completion of a homebuyer education course.

The practical question most buyers don’t ask: if you use DPA to cover your down payment, does FHA or conventional end up cheaper on a monthly basis? The answer depends on your credit score. With DPA covering the down payment, a buyer with 700+ credit on a conventional loan still comes out ahead on monthly costs. The PMI rate is low and cancels eventually. FHA MIP doesn’t.

A buyer with a 640 credit score using DPA might find FHA keeps their monthly payment more manageable, even accounting for the longer MIP duration.

Run the numbers both ways with your lender. Ask them to show you the total cost of ownership at 5 years, 10 years, and 30 years for each scenario. That comparison will give you your answer faster than any online calculator. If you’re still deciding whether now is the right time to buy at all, First-Time Home Buyer in Kent WA: Buy Now or Wait? runs through the timing math that applies across most of South King County.

What This Means for You

Here’s the practical decision tree:

Credit score below 620

Start with FHA. Focus on improving your score if you can. Even a 40-point gain can change which loan type makes more financial sense.

Credit score 620–700

Get quotes for both FHA and conventional. Ask your lender to compare total MIP/PMI costs over your expected hold period, not just the monthly payment.

Credit score 700+

Conventional almost always wins. The monthly savings from lower PMI and eventual cancellation add up to tens of thousands of dollars over a 10–30 year hold.

Concerned about down payment

Ask about WSHFC DPA programs. They work with both loan types and can cover your entire down payment if you qualify.

Planning to stay under 5 years

Conventional makes even more sense here. You won’t reach MIP removal with FHA anyway, so you’re paying insurance the whole time you own.

Planning to put down 20% or more

Conventional is the clear choice. You pay no PMI at all and skip FHA’s upfront MIP entirely.

Frequently Asked Questions

Can I use FHA financing to buy a home in Renton, Kent, or Auburn?

Yes. The 2026 FHA loan limit in King County is $1,063,750 which covers virtually every home in South King County. FHA is fully available in all King County cities.

What credit score do I need for a conventional loan in King County?

The minimum is generally 620, though some lenders go to 580 with specific programs. For the best PMI rates and lowest long-term costs, you want 700 or above.

How much does FHA mortgage insurance cost in King County?

On a typical King County FHA loan, you’ll pay 1.75% upfront (rolled into the loan) and roughly 0.55% annually as a monthly premium. On a $575,000 purchase with 3.5% down, that’s about $810 per month all-in for principal, interest, and MIP at current rates — though your actual rate will vary.

Will an FHA offer hurt my chances in a competitive King County market?

It can in very hot price ranges. But in most South King County markets in 2026, a well-structured FHA offer with a strong pre-approval is fully competitive. Talk to your agent about the specific neighborhood and price point before worrying about this.

Can I stack down payment assistance with an FHA loan in Washington?

Yes. WSHFC’s Home Advantage and Opportunity DPA programs both work with FHA loans. The DPA is a deferred second mortgage with no payments until you sell or refinance.

When does it make sense to just wait and improve my credit before buying?

If you’re within 3–6 months of crossing from 680 to 720, and your local market isn’t moving aggressively upward, it can be worth waiting. The PMI savings over 10 years on a $550,000+ King County loan easily justify 6 months of credit work. Ask your lender to model both scenarios.

Your guide to life outside Seattle.

253-350-0045 ·

greg@livingoutsideseattle.com ·

www.livingoutsideseattle.com