Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

A standard home inspection only covers your unit. Here’s how to check everything else — so you don’t inherit someone else’s financial mess.

If you’re shopping for a condo in King County, you already know the appeal. The $400K to $550K price range gets you into cities like Renton, Kent, Auburn, and Federal Way where single-family homes now regularly push past $700,000. Condos let first-time buyers get into the market with a lower entry point and no yard to maintain.

But buying a condo isn’t the same as buying a house. When you buy a condo, you’re not just buying the unit. You’re buying into the association that owns everything outside your four walls — the roof, the parking structure, the elevators, the exterior siding. You’re signing on as a stakeholder in the financial health of an organization you probably know nothing about yet.

That’s where most first-time condo buyers get burned. They fall in love with the unit, get excited about the price, and skip the due diligence that would tell them whether the building is a smart buy or a costly surprise waiting to happen. I’ve done BPO assessments on condo buildings across King County for years. The difference between a well-run community and a poorly-run one shows up in the documents — if you know what to look for.

Here’s what you need to check before you write that offer.

The Reserve Study: Your Most Important Document

The reserve study is an independent engineering report that tells you two things: what major components the association owns (roof, siding, pavement, elevators, common area systems) and how much money the HOA needs to set aside right now to cover those replacements when they come due.

Think of it like a maintenance budget projected out 20 or 30 years. A well-funded reserve means the HOA has been saving consistently and won’t need to hit owners with a surprise bill when the roof fails. An underfunded reserve means the opposite.

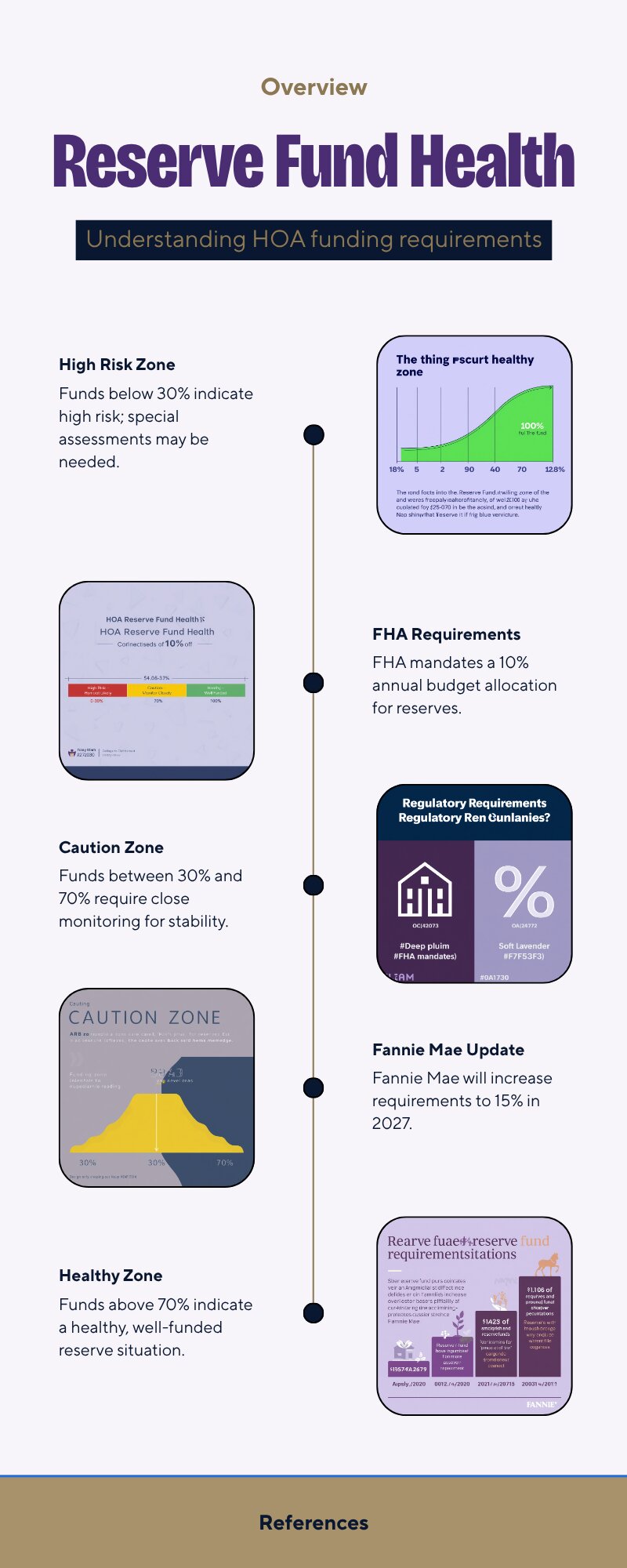

Here’s the number that matters most: the funding percentage. Most reserve studies show this as a percentage of “full funding.” Anything above 70% is generally healthy. Below 30% is a serious red flag. According to the Community Associations Institute, more than 70% of HOAs nationally are considered underfunded. That’s not a comfort — it’s a warning about how common the problem is.

In Washington state, as of 2026, HOAs must include reserve fund information in resale certificates. Still, don’t rely on what the HOA tells you in summary form. Ask for the full reserve study report and read the section on reserve component status yourself.

Anything above 70% is generally healthy. Below 30%, a special assessment is likely — not a matter of if, but when.

Special Assessments: What They Are and How to Spot the Risk

A special assessment is an extra charge the HOA levies on every unit owner to cover a large expense the reserve fund can’t handle. They’re not uncommon. What makes them dangerous is that they can hit without much notice and they don’t care when you bought your unit.

An older 50-unit building might face a $200,000 roof replacement with nothing saved. That works out to $4,000 per unit — potentially due in a lump sum or in payments spread over a couple of years. Special assessments in King County can run $60,000 to $80,000 per unit when major structural or mechanical work has been deferred for years.

Before you make an offer, ask for the last five years of special assessment history. If there’s been one large assessment or multiple smaller ones in that window, ask why. The answer tells you a lot about how the board manages the property. Also ask whether any special assessments have been approved but not yet levied. Washington’s WUCIOA law requires this to be disclosed in the resale certificate — but only for assessments already approved by the board. A vote that hasn’t happened yet won’t show up anywhere except in the board minutes.

Which brings me to the board minutes.

Read the Board Meeting Minutes

Board minutes are a window into everything the summary documents won’t tell you. Most buyers never ask for them. That’s a mistake.

You’re looking for a few things specifically. First, any discussion of upcoming major repairs or capital projects. Second, any mention of litigation — whether the HOA is suing a contractor or a homeowner is suing the HOA. Third, any talk of raising dues significantly, levying a special assessment, or adjusting the reserve contribution downward to balance the operating budget. That last one is a classic sign of financial stress.

Under Washington’s WUCIOA updates effective January 1, 2026, condo associations must now hold open board meetings and provide better documentation to buyers. The resale certificate that comes with any condo sale must include 26 specific items and can only cost you up to $275. You also have a 5-day cancellation right after receiving all required documents. That window is your formal due diligence period — use it.

The Warrantable vs. Non-Warrantable Problem

This is the one that trips buyers up most often, and it has nothing to do with the unit itself. It has to do with the building.

A condo building is considered “warrantable” when it meets Fannie Mae and Freddie Mac lending standards. A warrantable building means you can get a conventional mortgage, FHA financing, or a VA loan — whatever you qualify for. Normal rates, normal down payments.

A non-warrantable building doesn’t meet those standards, and you lose access to the most competitive loan products. You’re looking at higher rates and larger down payments — often 20% or more — because portfolio lenders are taking on more risk. For a $500,000 condo, the difference between a warrantable and non-warrantable rate at current levels can easily add $200 to $250 to your monthly payment.

What Makes a Building Non-Warrantable?

The most common triggers in King County:

Single entity owns 25%+ of units — often an investor who bought in bulk during slower markets.

More than 35% commercial square footage — common in mixed-use buildings in downtown Renton or Federal Way.

Short-term rental policies — buildings that allow Airbnb-style rentals trigger automatic non-warrantable status.

Active or pending litigation — even a small dispute can knock a building out of warrantable status.

Ask your lender to run a condo project approval check before you get emotionally invested in a unit.

Many King County condo buildings — especially older mid-rises in Renton, downtown Kent, and Federal Way — fall outside warrantable guidelines. Knowing this upfront shapes your financing strategy before you’re already under contract.

For a full look at what mortgage rates look like right now for King County buyers, see our King County Mortgage Rates 2026 guide. If your condo ends up in the non-warrantable category, a mortgage rate buydown negotiated into the deal can help offset the higher rate.

Rental Cap Rules: What They Mean for Your Investment and Resale

Some condo associations limit how many units can be rented out at any given time. This is a rental cap, and it matters in two ways.

First, if you’re buying as an investor or might need to rent your unit down the road, a rental cap could block you entirely if the cap is already at its limit. Second — and this affects every buyer — a tight rental cap can make your building non-warrantable, which reduces your future buyer pool when you go to sell.

In Washington state, a rental cap must be written into the Declaration (the CC&Rs), not just the rules and regulations. Washington courts have ruled that caps can’t be created by the board alone — they need a supermajority vote to amend the Declaration. Check the current governing documents to see whether a cap exists, what the limit is, and whether it’s currently at capacity.

What a Standard Inspector Won’t Check

Here’s what a lot of condo buyers don’t realize: Washington state home inspectors are not required to inspect common elements, shared structural systems, or common area amenities. The inspector looks at your unit. The roof, the parking structure, the building envelope, the elevators, the main plumbing stack — those fall outside the standard inspection scope.

That means the structural and mechanical health of the entire building you’re buying into rests entirely on the HOA documents, not on any physical inspection you can order.

This is why the reserve study and the board minutes matter as much as they do. They’re the closest thing you have to a building inspection. If the association has been commissioning regular reserve studies and following the funding plan, you can feel reasonably confident. If the last reserve study is eight years old and nobody can find the financials, that’s your answer.

Washington’s new WUCIOA rules (effective 2026) cap the resale certificate fee at $275 and give you a 5-day cancellation window after receiving all required documents.

The Local Angle: What Makes King County Condos Different

King County’s condo market is concentrated in a handful of cities. The sub-$500K inventory you’ll find in Renton, Kent, Auburn, and Federal Way tends to be in older mid-rise buildings — think 1980s and 1990s construction. Some of these buildings have been well-maintained. Many have deferred capital work for years because the HOA fees were kept artificially low to attract owners.

As of the May 2026 King County market update, condo inventory is elevated relative to last year. That’s actually good news for buyers doing due diligence — you have more options and more negotiating room if a building’s documents reveal problems. You can move to the next building rather than feeling pressured to overlook red flags. For more on current conditions, see the King County Real Estate Market Update May 2026.

One thing I always watch from a pricing standpoint: HOA fees relative to market rates for the building’s age and amenities. An older building with fees significantly below market isn’t a deal — it’s a warning sign that the board has been cutting corners on reserves or maintenance to keep fees low. That cost shows up later. Often all at once.

If you’re weighing a condo against a townhouse or a single-family home in the same price range, the Condo vs. Townhouse vs. Single-Family Home in King County comparison guide can help you think through the tradeoffs before you commit to any one property type.

What This Means for You as a Buyer

Getting a condo offer right comes down to this: the unit is the easy part. Every agent will show you the finishes and the view. The due diligence that protects you happens in the documents.

Request the full resale certificate as soon as you’re seriously interested in a building — Washington law now limits the fee to $275 and gives you five days to review after receiving all required items. Use those five days. Read the reserve study funding percentage. Scan the last two years of board minutes for anything that sounds expensive. Pull the special assessment history. Have your lender check the project for warrantability before you fall in love with the floor plan.

If any of those documents are hard to get, incomplete, or missing entirely — that’s important information. A well-run HOA has nothing to hide.

Frequently Asked Questions

How do I get the reserve study and HOA financials as a condo buyer in Washington?

Request them in writing through your real estate agent as part of the offer or as a pre-offer document request. Under Washington’s WUCIOA law, the resale certificate is a required disclosure and must be provided within a set timeline. Your agent can request the full reserve study separately — not all associations include the full report in the standard resale package.

What reserve fund percentage should I look for when buying a condo in King County?

A funding level at or above 70% of “full funding” is generally healthy. Below 50% warrants a deeper conversation with the HOA or your agent. Below 30% is a serious red flag for near-term special assessments. FHA requires HOAs to allocate at least 10% of their annual budget to reserves — Fannie Mae is moving toward 15% effective January 2027.

What makes a condo non-warrantable in Washington state?

The most common triggers are high investor ownership (one entity owning 25%+ of units), active or pending litigation, short-term rental policies, and high commercial space concentration. Your lender can run a condo project approval check to confirm status before you’re under contract.

Can I use an FHA loan on a condo in King County?

Yes, if the building is FHA-approved or spot approval is available. FHA has its own approval process separate from conventional warrantability. Your lender will know whether the specific project is on FHA’s approved list or whether spot approval is an option for that building.

What should I look for in condo board meeting minutes?

Look for any discussion of deferred repairs, upcoming capital projects, special assessment votes (including proposed but not yet approved), litigation, significant dues increases, or decisions to reduce reserve contributions. Any of these can signal financial stress in the association.

Is a condo’s rental cap in the CC&Rs or the rules?

In Washington state, rental caps must be in the Declaration (CC&Rs) to be enforceable — not just the rules and regulations. If you see a rental cap only in the R&Rs and it’s not in the Declaration, its enforceability may be questionable under current Washington case law. Still, treat it as a real restriction until a real estate attorney tells you otherwise.

Buying a condo in King County can be a smart move. The entry-level price points in South King County are some of the last affordable options for first-time buyers in the region. But the savings on purchase price can disappear fast if you walk into a building with underfunded reserves, pending litigation, or a non-warrantable status nobody mentioned upfront.

The documents tell the story. Take the time to read them.

Your guide to life outside Seattle.

253-350-0045 ·

greg@livingoutsideseattle.com ·

www.livingoutsideseattle.com