Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

A plain-English look at what lenders actually check before they hand you a loan, and how to know your real number before you start shopping homes in King County.

Most people think mortgage qualification is about one thing: your income. It is not. A lender looks at four things, and your salary is only one of them. I watch this play out every week with first-time buyers in Renton, Kent, and Auburn. Someone makes good money, assumes they will qualify for plenty, and then learns their car loan and student debt cut their buying power by a hundred grand. That surprise is avoidable.

Here is the part that matters for you. Knowing how mortgage qualification works in Washington State before you tour a single home means you shop in the right price range from day one. You write stronger offers because your pre-approval is solid. And you do not fall in love with a house you were never going to get. This guide walks through exactly what a lender measures, how they do the math, and what to do if the answer is “not yet.”

The Four Things a Lender Actually Checks

When you apply for a loan, the lender is answering one question: will this person pay us back every month? To get there, they look at four areas. Miss the mark on any one and your approval can stall, even if the other three are strong.

The first is income, but not the way you might think. Lenders use your gross monthly income, the amount before taxes come out. They also need to see that it is stable and likely to continue. A two-year track record is the standard. The second is your debt-to-income ratio, which is the single most important number in the whole process. The third is your credit score and history. The fourth is your down payment and the cash reserves you have left after closing. Each one tells the lender something different about your risk as a borrower.

So what does this mean for you? You can have a great salary and still get turned down if your debt load is too high. And you can have a modest income and qualify comfortably if you carry almost no debt. The mix matters more than any single number.

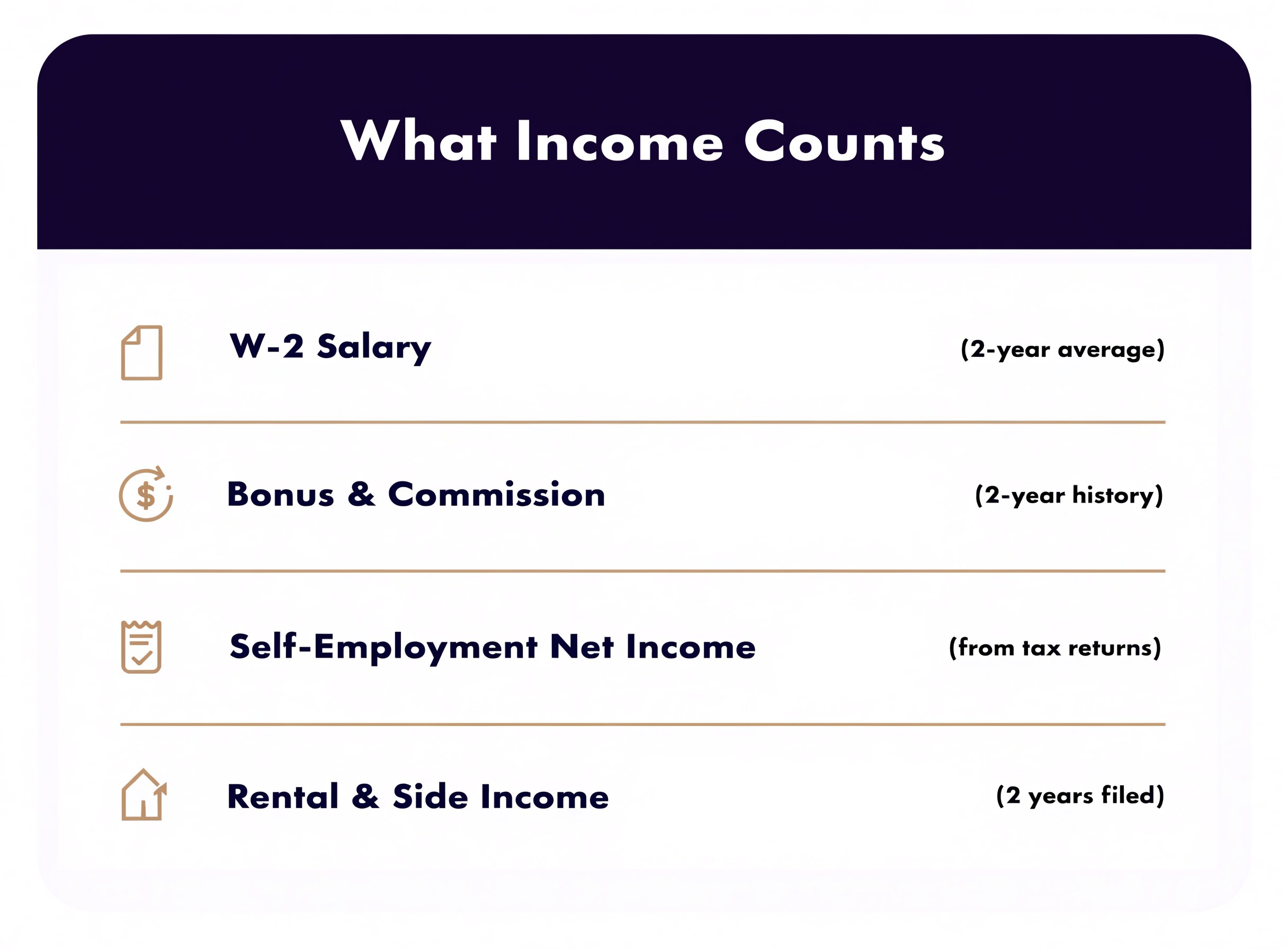

Income: What Counts and What Does Not

Lenders want income they can rely on. A steady paycheck from a W-2 job is the easiest kind to document. They average your pay over the last two years, and they want to see that you have stayed in the same line of work. Switching from nursing to nursing at a new hospital is fine. Switching from nursing to opening a food truck six months ago is a problem, because there is no track record yet.

Bonus, commission, and overtime income count too, but only if you have a history of earning it. A lender will usually average two years of bonus pay and use that figure. One big bonus last quarter does not count if the year before showed nothing. Side income from a rental property or a second job can also help, as long as you have filed taxes on it for two years.

Lenders want a two-year track record on most income types before they will count it.

Self-Employed Buyers: The Rules Are Different

If you own a business or work as a 1099 contractor, the math changes. Lenders do not use the money your business brings in. They use your net income after expenses, pulled straight from your tax returns. They add up your net profit from the last two years, then divide by 24 to get a monthly figure. So if you netted $110,000 one year and $104,000 the next, that is $214,000 divided by 24, or about $8,917 a month in qualifying income.

Two wrinkles trip up self-employed buyers. First, if your second year was lower than your first, many lenders stop averaging and use only the lower year. They want to see income holding steady or rising, not falling. Second, lenders add some paper deductions back in. Depreciation, for example, is a tax write-off that never actually left your bank account, so a lender adds it back to your qualifying income. That can work in your favor.

Debt-to-Income Ratio: The Number That Decides Everything

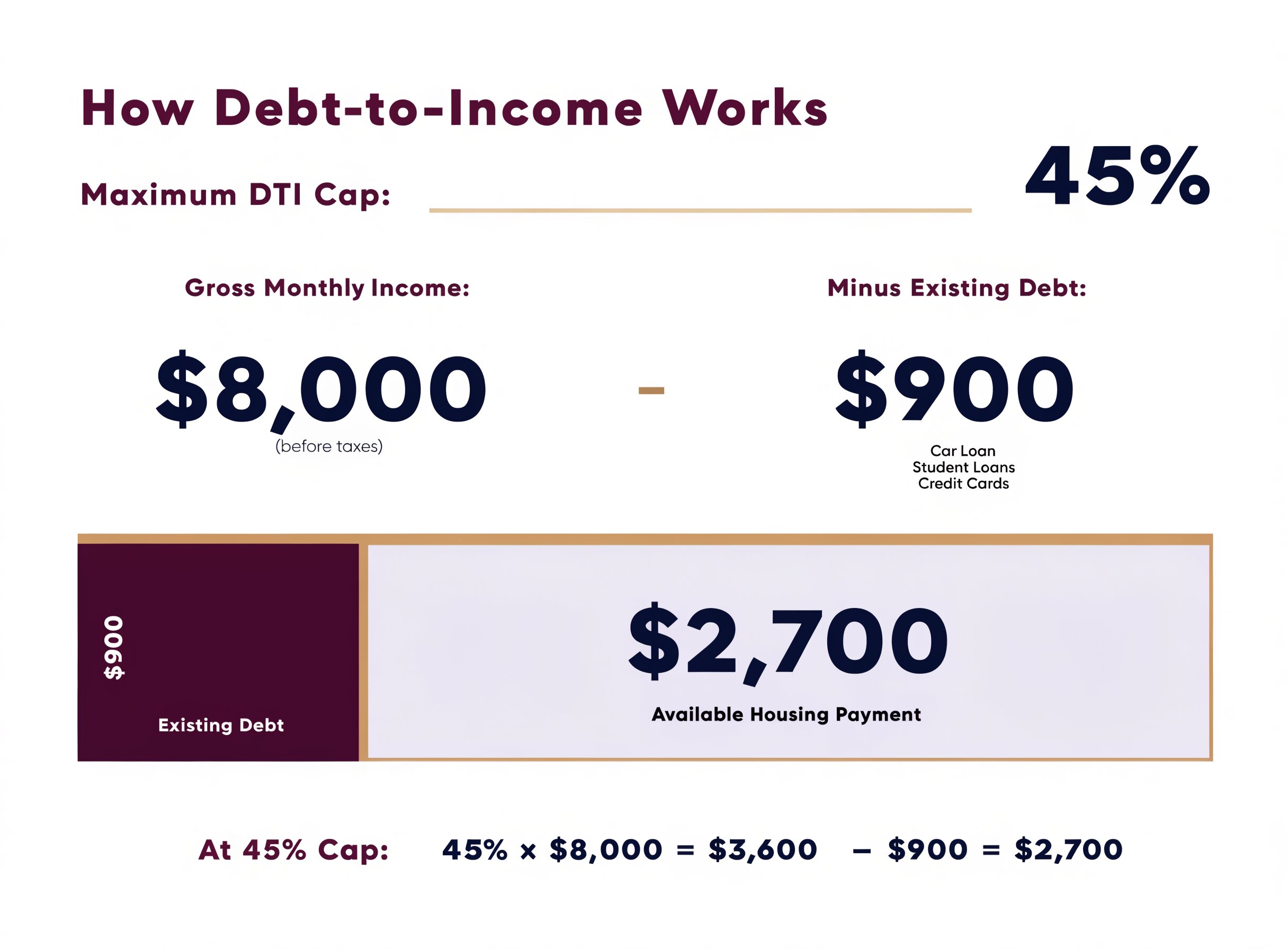

Your debt-to-income ratio, or DTI, is the percentage of your gross monthly income that goes toward debt payments. It is the number that makes or breaks most applications, so it is worth understanding well.

There are two versions. Your front-end ratio is just your future housing payment divided by your gross monthly income. Your back-end ratio adds in everything else: car loans, student loans, credit card minimums, personal loans, and the new mortgage. Lenders care most about the back-end number.

Here is how it works in practice. Say you earn $8,000 a month before taxes. You have a $450 car payment, a $300 student loan payment, and $150 in credit card minimums. That is $900 in monthly debt before any mortgage. If a lender caps your back-end DTI at 45 percent, your total debt can be $3,600 a month. Subtract the $900 you already owe, and you have $2,700 left for a mortgage payment, including taxes and insurance. That single calculation sets your price range.

Paying off one car payment can raise your buying power by tens of thousands of dollars.

The caps vary by loan type. Conventional loans usually want a back-end DTI at or below 45 percent, though strong credit and a bigger down payment can push that to 50. FHA loans officially target 31 percent for housing and 43 percent for total debt, but with automated underwriting approval and solid compensating factors, they can stretch to nearly 57 percent. VA loans for veterans and active-duty service members do not set a hard cap at all. They use a 41 percent guideline and focus on residual income, the cash you have left each month after your big bills are paid.

What does this mean for you? Pay down a credit card or knock out a small loan before you apply, and you can free up real buying power. I have seen buyers raise their price range by $40,000 to $60,000 just by paying off one car. If you want to understand how your full monthly cost breaks down once you do buy, our guide on the total cost of homeownership in King County walks through every line item.

Credit Score: What Lenders Want to See

Your credit score tells a lender how you have handled borrowed money in the past. Each loan program has a minimum. Conventional loans generally want a 620 or higher. FHA loans can go lower, sometimes down to 580 with a 3.5 percent down payment, or even 500 with a larger down payment. VA loans do not set a federal minimum, but most lenders want around 620.

Your score does more than open the door. It also sets your interest rate. A buyer with a 760 score gets a noticeably lower rate than a buyer with a 640 score on the exact same loan. Over 30 years, that gap is tens of thousands of dollars. If your score sits in a lower tier, a few months of on-time payments and lower card balances can move you up before you lock a rate.

If you are weighing FHA against a conventional loan and wondering which fits your credit and down payment, our breakdown of FHA vs. conventional loans in King County lays out the trade-offs side by side.

Down Payment and Cash Reserves

The down payment is the cash you put toward the purchase up front. Bigger is not always required. Conventional loans can go as low as 3 percent down for first-time buyers. FHA needs 3.5 percent. VA and USDA loans can require zero down for those who qualify. So the old idea that you need 20 percent is simply not true for most buyers.

A larger down payment still helps in two ways. It lowers your monthly payment, and once you cross 20 percent on a conventional loan, you drop private mortgage insurance, which can save a couple hundred dollars a month. Lenders also like to see reserves, meaning money left in the bank after closing. A few months of mortgage payments in savings makes your application stronger.

Down payment money is also where many King County buyers find help they did not know existed. Several programs can cover part or all of your down payment, with deferred repayment in some cases. Our full guide to King County down payment assistance programs breaks down who qualifies and how to stack programs.

The Local Angle: What Qualifying Looks Like in King County

National advice only gets you so far, because qualification numbers run into local prices. King County is an expensive market, and the federal government recognizes that with a higher loan limit. For 2026, the conforming loan limit here is $1,063,750 for a single-family home, far above the national baseline. Every city in the county shares that limit, from Renton and Kent to Auburn and Federal Way.

Why does that matter for you? Loans up to that amount follow standard conforming rules. Go above it and you enter jumbo territory, where lenders want bigger down payments, higher credit scores, and more reserves. Because South King County prices generally sit below that ceiling, most first-time buyers here qualify under the easier conforming guidelines. A $700,000 home in Kent or a $668,000 home in Auburn keeps you well inside the conforming box.

The first-time buyers I work with most often are dual-income couples in their early thirties earning somewhere between $90,000 and $160,000 a household. Many also have student loans and a car payment, which is exactly why DTI, not salary, ends up being the deciding factor. The good news is that South King County still offers homes priced where those households can qualify, especially in Auburn, Kent, and parts of Renton. If you want a real picture of what payments look like at current rates, our post on King County mortgage rates and what buyers are actually paying shows the monthly math.

What This Means for You as a Buyer

Start with a real pre-approval, not an online calculator. An online estimate does not pull your credit or verify your income, so it is a guess. A lender pre-approval gives you a hard number you can shop with and an offer sellers take seriously.

Before you apply, do three things. Pull your credit and fix any errors. Pay down a card or a small loan if you can, since every dollar of monthly debt you erase frees up room for a mortgage payment. And gather two years of tax returns, recent pay stubs, and bank statements so the process moves fast. If you are early in the journey and still deciding whether buying even makes sense yet, our look at buying now versus waiting in nearby Auburn runs the real math.

One honest note. Getting pre-approved does not mean you should borrow the full amount. The lender tells you the ceiling. Your budget and your comfort level should set the actual number. A payment that looks fine on paper can feel tight once property taxes, insurance, and life show up.

What to Do If You Do Not Qualify Yet

A “not yet” is not a “no.” Most buyers who get turned down are closer than they think. If your DTI is too high, the fastest fix is paying down revolving debt and avoiding new loans before you reapply. If your credit score is the holdup, a few months of on-time payments and lower balances can move you into a better tier and a better rate.

If your income is the issue, time and documentation usually solve it. A self-employed buyer who is one year into a business often just needs to reach the two-year mark. A buyer who recently switched careers needs to build a short track record in the new field. And if the down payment is the gap, assistance programs in King County exist for exactly that reason. The point is simple: find out where you stand now, fix the one thing holding you back, and reapply with a plan.

Frequently Asked Questions

How much income do I need to qualify for a mortgage in King County?

There is no single number, because it depends on your debt, your down payment, and current rates. Lenders care about your debt-to-income ratio, not your salary alone. As a rough guide, a household with little other debt buying a median-priced South King County home often needs somewhere in the low-to-mid six figures of household income, but a buyer with no car payment or student loans can qualify on less.

What is a good debt-to-income ratio to buy a home in Washington State?

Most loan programs want your total, or back-end, DTI at or below 43 to 45 percent, though FHA and VA loans can stretch higher with strong credit and compensating factors. Below 36 percent is considered strong and gives you the most options. The lower your DTI, the more house you can qualify for at the same income.

Can I qualify for a mortgage if I am self-employed in Washington?

Yes. Lenders use your net business income from the last two years of tax returns, averaged over 24 months, and add back certain paper deductions like depreciation. The catch is that aggressive tax write-offs lower the income a lender can count, so plan ahead if you intend to buy.

What credit score do I need to buy a home in King County?

Conventional loans usually want 620 or higher. FHA loans can go down to 580 with 3.5 percent down, or 500 with a larger down payment. VA loans have no federal minimum, but most lenders look for around 620. A higher score also earns you a lower interest rate.

How much do I need for a down payment in King County?

Less than most people assume. Conventional loans can require as little as 3 percent down, FHA needs 3.5 percent, and VA and USDA loans can be zero down for those who qualify. King County down payment assistance programs can cover part of that for eligible buyers.

Does getting pre-approved guarantee I get the loan?

Pre-approval is strong, but not a final guarantee. It is based on the information you provide and a credit pull. Final approval comes after the lender verifies everything and the home appraises. Avoid taking on new debt or changing jobs between pre-approval and closing, since either can change your numbers.

Know Your Number Before You Start Looking

Mortgage qualification in Washington State is not a mystery. It is four things a lender checks: income, debt-to-income ratio, credit, and down payment. Understand those, get a real pre-approval, and you walk into the King County market knowing exactly what you can buy and writing offers that hold up.

Your guide to life outside Seattle.

253-350-0045 ·

greg@livingoutsideseattle.com ·

www.livingoutsideseattle.com