Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

A step-by-step guide to HOA due diligence, warrantable financing, and what to inspect — written for first-time buyers entering the King County condo market.

If you are thinking about buying a condo in King County, 2026 is an interesting time to do it. Active condo listings on the Eastside are up more than 40% compared to last year. That means more options, more time, and more leverage than buyers had just 12 months ago. But the market shifting in your favor does not mean every condo is a good deal. The wrong one can cost you your financing, your down payment flexibility, and years of headaches tied to a poorly run HOA.

I have been pricing properties in East and South King County every day for over 9 years as a BPO field agent. I walk into condos that look great on Zillow and flag problems that would not show up until after you close. This guide covers everything a first-time condo buyer in King County needs to know before making an offer.

What Makes Condos Different to Buy (and Finance)

A condo is not just a smaller version of a house. When you buy a condo, you own your individual unit — usually defined as the “airspace” inside the walls — plus a fractional share of the common areas. The hallways, the roof, the parking structure, the elevators: you own a piece of all of it, along with every other owner in the building.

That shared ownership is why lenders treat condos differently. They are not just evaluating you as a borrower. They are evaluating the entire building and its homeowners association. A lender can approve your income, your credit score, and your down payment — and still decline your loan because the HOA has financial problems.

This is the part most first-time condo buyers do not expect, and it is why starting with the right questions matters.

Warrantable vs. Non-Warrantable: The Financing Split That Changes Everything

The single most important financing question in any condo purchase is whether the building is warrantable or non-warrantable. Here is what that means in plain terms.

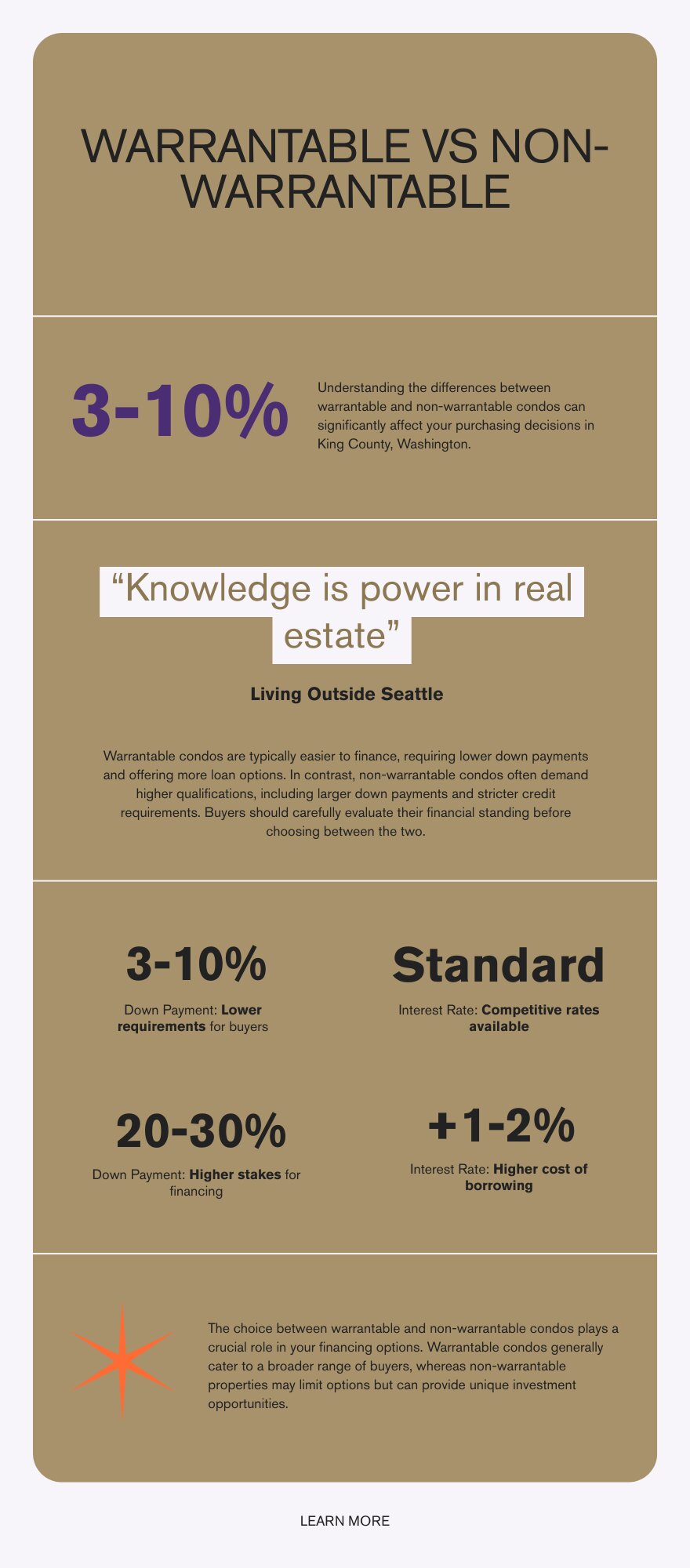

Warrantable condos meet the guidelines set by Fannie Mae and Freddie Mac. These are the government-sponsored enterprises that back most conventional mortgages in the United States. When a building qualifies as warrantable, buyers can use standard conventional loans, FHA loans, and VA loans. Interest rates are standard. Down payments can be as low as 3% with some programs.

Non-warrantable condos do not meet those guidelines. Buyers are pushed into portfolio loans — products held by the lender rather than sold to Fannie or Freddie. These typically require 20–30% down and carry interest rates 1–2 percentage points higher than conventional financing. On a $500,000 condo, that rate difference adds roughly $500–600 per month to your payment.

For 2026, there is a specific rule change worth knowing. By January 2027, HOAs must allocate at least 15% of their annual budgeted assessment income to their reserve fund — up from the longstanding 10% minimum. Buildings that fall short lose warrantable status. When you are shopping for a condo right now, you are evaluating buildings that may be in the middle of adjusting to this change, or ignoring it entirely.

Warrantable condos open the door to conventional and FHA financing — non-warrantable buildings push buyers into portfolio loans with higher rates and larger down payments.

What disqualifies a building from warrantable status? The main triggers include: the HOA reserve fund falling below 10% of the annual budget (now moving to 15%), more than 15% of owners being delinquent on dues, a single investor owning more than 20% of the units, more than 35% of the building being used for commercial purposes, and ongoing or threatened litigation against the HOA.

Ask your agent to request the condo questionnaire — also called the HOA certification or lender questionnaire — before you write an offer. This document discloses the reserve balance, delinquency rate, pending litigation, and owner-occupancy percentage. If a seller or listing agent resists providing it, treat that as a warning sign.

HOA Due Diligence: What to Actually Read

The HOA package — sometimes called the resale certificate, disclosure packet, or condo docs — is a stack of documents you will receive after going under contract. In Washington State, sellers are required to provide it, and you typically have a review period to back out if you find something concerning.

Most buyers skim it. That is a mistake. Here is what actually matters:

The Reserve Fund Study

This is a professional assessment of the building’s major systems — roof, elevators, parking structure, plumbing, windows — and how much money the HOA should have saved to replace them on schedule. A well-run HOA commissions one every three to five years. If the building is 20 years old and there is no reserve study, or if the study shows the fund is significantly underfunded, you are looking at the possibility of special assessments in your future.

Special assessments are one-time charges that all owners must pay when the HOA does not have enough reserves to cover a major repair. These can run $5,000, $15,000, even $30,000 per unit for things like roof replacements and elevator overhauls — and they happen regularly in buildings with underfunded reserves.

Meeting Minutes from the Past Two Years

Board meeting minutes are where you find the real story. Look for repeated complaints about the same issue, deferred maintenance discussions, arguments over raising dues, or mentions of legal action. A building with the same roof leak showing up in 18 consecutive meeting minutes has a problem the financials may not fully capture.

Two years of minutes gives you a solid picture of how the board actually operates — not just what they say in the official documents.

The Budget, Dues, and Rental Rules

Check whether the HOA has raised dues recently, and whether dues cover reserves adequately. Artificially low dues often mean the HOA is avoiding necessary increases — which leads to larger special assessments later. Compare dues to similar buildings in the area. A number that looks suspiciously low usually is.

Also check rental cap rules. Some buildings limit the percentage of units that can be rented at any time. If you ever plan to rent your unit, this matters. FHA loans also require the building to be on HUD’s approved condo list — your lender can check this quickly.

For a deeper dive on what to check in the HOA docs, the King County Condo Due Diligence Checklist goes through this line by line.

What a Condo Inspection Covers (and What It Misses)

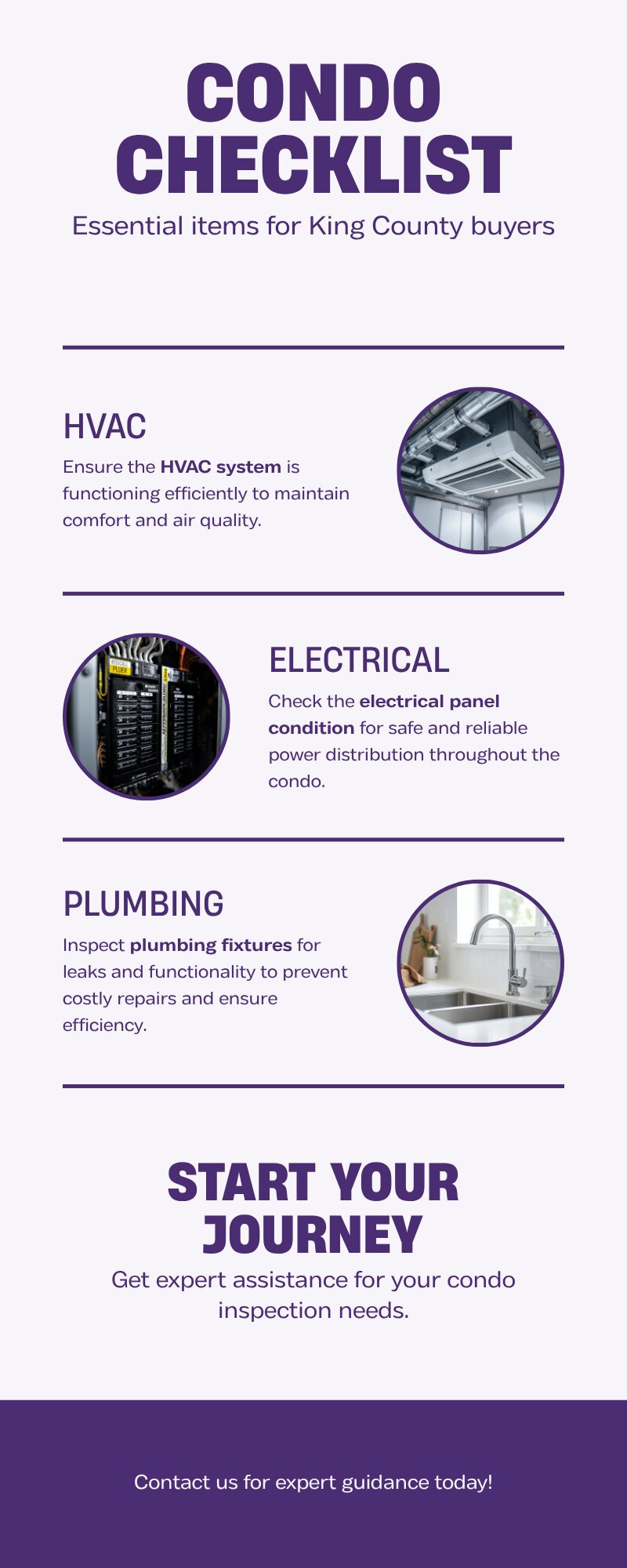

A standard home inspection is designed for a single-family house where the inspector can access the roof, crawl space, attic, and all the mechanical systems. A condo inspection is different — and more limited.

Your inspector will cover what is inside your unit: the HVAC (if it is individual to your unit), the electrical panel, plumbing fixtures, windows, doors, and visible water damage. They will typically inspect the balcony and any storage spaces assigned to your unit. What they cannot fully assess: the building’s shared systems, the roof, the structural elements, or common area mechanical equipment.

That is why the HOA documents and the reserve study matter so much. The inspection tells you about your unit. The HOA documents tell you about the building. You need both.

A few things worth flagging during your condo inspection specifically:

Soundproofing between units. This is not a safety issue, but it matters enormously to quality of life. Bring a friend, have them stomp around upstairs while you listen from below.

Water intrusion around windows and exterior walls. Condo buildings in the Pacific Northwest are prone to moisture issues. Look for staining, soft drywall near windows, or any history of water claims in the HOA meeting minutes.

HVAC type. Some older King County condo buildings use central HVAC controlled by the HOA. Others have individual mini-split or forced-air systems in each unit. If it is individual, it is your responsibility to maintain and replace. Know what you are buying before you close.

A standard home inspection covers your unit. The HOA documents cover the building. You need both before you close on a King County condo.

The King County Condo Market Right Now

King County condo prices have held more steady than single-family homes in 2026, but the market has shifted toward buyers. Active condo listings on the Eastside are up more than 40% year over year as of spring 2026. More supply means more negotiating room — on price, closing costs, and seller-paid concessions.

In South King County — Kent, Auburn, Renton — condos remain some of the most accessible entry points in the county. Depending on the city, you can find units in the $350,000–$500,000 range, well below the King County median of $835,000 for all residential property types. For buyers using down payment assistance programs, these price points make a real difference in what you can qualify for.

The current rate environment also affects condo buyers differently than house buyers. If you are using conventional financing on a non-warrantable building, your effective rate goes up significantly — which is why building status matters as much as your personal loan qualification. King County’s conforming loan limit for 2026 is $1,063,750, so most condo purchases in South King County fit comfortably within conventional limits.

First-Time Buyer Programs That Work for Condos

If you are a first-time buyer — meaning you have not owned a home in the past three years — several programs in Washington State work for condo purchases.

The WSHFC Home Advantage Program pairs a 30-year fixed-rate mortgage (conventional, FHA, VA, or USDA) with a below-market interest rate. It also offers down payment assistance up to 4% of the first mortgage amount as a 0% interest, 30-year deferred loan — repayable when you sell or refinance. Income limits apply: for King County, the cutoff is $180,000 for 2026. Minimum credit score is 620 (640 for some loan types). You must use a WSHFC-approved lender.

For a side-by-side comparison of condo versus single-family ownership costs — including what HOA dues do to your total monthly payment — the Condo vs. Townhouse vs. Single-Family guide covers the real numbers for King County buyers.

What This Means for You as a King County Condo Buyer

Buying a condo in King County in 2026 is genuinely doable — especially in South King County where price points are accessible and buyer leverage is higher than it has been in years. But it requires a different checklist than buying a house.

Start with the financing question before you fall in love with a unit. Get your agent to pull the condo questionnaire early. If the building is non-warrantable, run the math on what that does to your monthly payment before you invest time in inspections and negotiations.

Read the HOA documents yourself, not just the summary. The meeting minutes are where problems hide. If the reserve fund is below 10% of the annual budget — and especially below the new 15% target — build that risk into your offer price or walk away.

Hire an inspector who has experience with condos specifically. Ask them directly whether they check for water intrusion at the building envelope, not just inside the unit. And use state programs if you qualify — the WSHFC income limit is $180,000 for King County, which is higher than most people assume.

Frequently Asked Questions

What is the difference between a warrantable and non-warrantable condo in King County?

A warrantable condo meets Fannie Mae and Freddie Mac guidelines, which means buyers can use standard conventional or FHA financing with low down payments. A non-warrantable condo does not meet those guidelines — typically because of low HOA reserves, high investor concentration, or pending litigation — and buyers are limited to portfolio loans requiring 20–30% down at higher rates.

How much are condo HOA dues in King County?

HOA dues vary widely by building age, size, and amenities. In South King County, dues commonly run $300–$600 per month for a standard condo. Eastside buildings with more amenities often run $500–$900 or more. Always verify what dues cover — some include water, sewer, and garbage while others cover only exterior maintenance and reserves.

Can I use an FHA loan to buy a condo in King County?

Yes, but the building must be on HUD’s FHA-approved condo list, or you can apply for single-unit (spot) approval. Your lender can check FHA approval status in minutes. Not all King County condos qualify, so this is worth checking early in your search rather than after you find a unit you like.

What is a condo reserve study and why does it matter?

A reserve study is a professional assessment of a building’s major systems and how much the HOA should have saved to replace them on schedule. A well-funded reserve means lower risk of special assessments — unexpected lump-sum charges to all owners when the HOA needs money for a major repair. Ask for the most recent reserve study in the HOA documents.

Do condo buyers in King County qualify for down payment assistance?

Yes. The WSHFC Home Advantage Program works for condo purchases and offers DPA up to 4% of the loan amount as a 0% deferred loan. Income limits are $180,000 for King County buyers in 2026. The building still must meet standard financing requirements for the underlying loan type — DPA does not change warrantable status.

What should I look for in condo HOA meeting minutes?

Look for recurring complaints about the same issue, deferred maintenance discussions, disputes over raising dues, mentions of legal action against the HOA or individual owners, and references to upcoming special assessments. Two years of minutes gives you a solid picture of how the board actually operates versus what the official financials show.

A condo can be a smart first step into King County homeownership — especially in today’s market, where inventory is up and sellers are more willing to negotiate than they were two years ago. The key is knowing what you are actually buying: your unit, your share of the building, and your exposure to how the HOA is run.

Have questions before you make an offer? Reach Greg at greg@livingoutsideseattle.com or 253-350-0045.

Your guide to life outside Seattle.

253-350-0045 ·

greg@livingoutsideseattle.com ·

www.livingoutsideseattle.com