Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Is staying a Bellevue renter actually costing you more than a mortgage? The math is more complicated than your landlord thinks — here’s the honest breakdown.

If you’re renting in Bellevue right now, someone has probably told you that you’re throwing money away. And someone else has probably told you that buying a $1.5 million home at 6.5% is financial suicide. Both arguments have merit. Neither one gives you a complete picture.

I work in King County real estate every single day, and the rent vs. buy question in Bellevue is one of the most nuanced I get. The city has some of the highest home prices in Washington — and some of the highest rents too. That changes the math compared to a typical analysis. What I’ll walk you through here is the actual 2026 cost comparison: what you’re paying as a renter, what you’d pay as a buyer, where the break-even point actually sits, and what DPA programs exist for buyers at Bellevue price points.

What Bellevue Renters Are Actually Paying in 2026

Bellevue rents have softened slightly from their peak — but they’re still among the highest in Washington State. Here’s where the market sits right now:

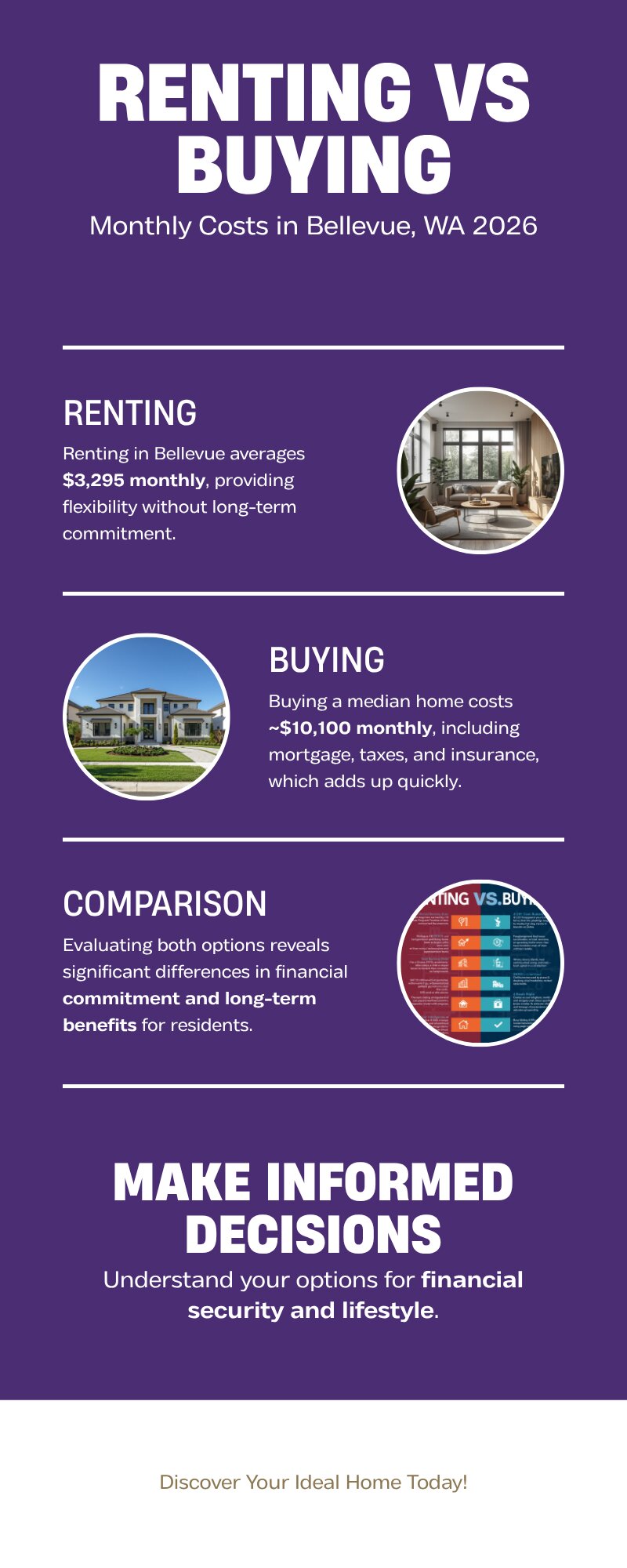

A one-bedroom apartment in Bellevue runs roughly $2,485–$2,889/month depending on the neighborhood and building. A two-bedroom ranges from $3,135 to $4,389/month. The city-wide average across all unit types is around $2,717/month, down about 1.25% from last year.

Downtown Bellevue and the Bel-Red corridor sit at the top of that range. You’ll find more affordable options on the Bellevue-Redmond border or near Factoria, but even those aren’t cheap. Bellevue rents run roughly 54% above the U.S. average.

For a renter in a two-bedroom apartment paying $3,295/month, that’s $39,540 per year going to a landlord. Over five years, that’s $197,700. Over ten years, that’s $395,400 — and rent almost certainly increases at least 2–3% per year, so the real ten-year number is closer to $440,000–$460,000.

That number sounds alarming. But before you run out and make an offer, let’s look at what ownership actually costs.

What Buying in Bellevue Actually Costs in 2026

The median sale price in Bellevue is approximately $1.45–$1.6 million depending on the data source and month. For this comparison, I’ll use $1.5 million as a workable midpoint — which is consistent with recent Redfin data.

Here’s the monthly ownership math on a $1.5M home with 20% down ($300,000):

Monthly Cost Breakdown: Owning a $1.5M Bellevue Home

Loan amount: $1,200,000 (after 20% down)

Principal + Interest at 6.5%: ~$7,585/month

Property taxes (0.75–1.0% effective rate): $937–$1,250/month

Homeowner’s insurance: ~$200–$250/month

Maintenance reserve (1% of value/year): ~$1,250/month

Total estimated monthly cost: $9,972–$10,335/month

Monthly cost breakdown based on $1.5M median home, 20% down, 6.5% 30-year fixed rate, plus property taxes and maintenance reserve. Source: Redfin, King County Assessor, 2026.

That’s a significant gap from what most two-bedroom Bellevue renters are paying. Even if you’re in a premium $4,400/month two-bedroom, you’re looking at nearly $6,000 less per month than full ownership costs on the median Bellevue home.

What If You Put Less Down?

Most first-time buyers in Bellevue can’t put $300,000 down. If you put 10% down ($150,000) instead, your loan becomes $1,350,000 and your P+I payment climbs to approximately $8,534/month — plus you’d pay PMI (roughly $200–$300/month) until you reach 20% equity. Total monthly cost: $10,200–$10,800+.

The 5% down scenario is even more expensive on a monthly basis, which is why a lot of Bellevue renters who could technically qualify for a mortgage decide to keep renting while they save.

The Break-Even Question: When Does Buying Win?

Here’s the honest answer: at current Bellevue prices and mortgage rates, the break-even horizon is long.

The price-to-rent ratio in Bellevue tells a lot of the story. Take the median home price of $1.5M and divide it by annual rent for a comparable space — say $48,000/year for a two-bedroom. That’s a price-to-rent ratio of about 31. Financial analysts generally say ratios above 25 favor renting. Bellevue is well above that.

Studies of comparable high-cost West Coast markets (Seattle, Portland, Los Angeles) put the typical break-even timeline at 16–23 years when factoring in total costs — mortgage interest, property taxes, maintenance, transaction costs on both ends, and lost investment returns on the down payment. In Bellevue, where prices are higher even than broader Seattle, the honest break-even is likely on the longer end of that range for buyers who aren’t putting at least 20% down.

Down Payment Assistance for Bellevue Buyers

One factor that changes the math: down payment assistance. Bellevue buyers have access to real programs — though at Bellevue price points, most DPA programs hit their purchase price limits quickly.

Here’s what’s available right now:

ARCH East King County DPA

The most Bellevue-specific program available. Provides up to $50,000 in deferred-loan down payment assistance for first-time buyers in East King County — including Bellevue and Kirkland. Income limits are set at 80% of Area Median Income. Given Bellevue’s high AMI, many buyers qualify on income even with solid salaries.

WSHFC Home Advantage

Washington State’s primary DPA program offers up to 4% of the loan amount as a second mortgage for down payment and closing costs. On a $1.2M loan, that’s up to $48,000 — meaningful, but it doesn’t close the gap on a 20% down payment.

WSHFC Opportunity DPA

Up to $15,000 for buyers under the income limits. More targeted toward the $400K–$750K purchase price range; income limits may restrict eligibility at median Bellevue prices.

Down payment assistance programs available to Bellevue-area buyers as of June 2026. Income and purchase price limits apply. Contact a WSHFC-approved lender for current eligibility.

The honest reality: most DPA programs work best in the $400K–$750K purchase price range. Bellevue’s median is double that. But for buyers targeting condos or smaller attached homes in the $650K–$900K range — which do exist in Bellevue — DPA can be a genuine option. Check out our full breakdown of King County down payment assistance programs for current eligibility details.

The King County Angle: Condo Entry Points in Bellevue

If the $1.5M median feels out of reach, Bellevue condos are a different conversation. The King County condo median sits around $550,000–$650,000 citywide, and Bellevue has options in that range — particularly in the Bel-Red corridor and parts of East Bellevue.

At $650,000 with 10% down ($65,000), the monthly P+I at 6.5% is approximately $3,700. Add property taxes (~$406/month), insurance (~$100/month), HOA (varies — budget $400–$700/month for a newer building), and you’re looking at roughly $4,600–$5,000/month total. That compares much more closely to what a two-bedroom apartment costs in Bellevue.

The break-even timeline on a Bellevue condo is shorter — likely in the 6–10 year range depending on appreciation — and DPA programs are more likely to apply at this price point.

Understanding what rates are doing right now is important to this math. If you haven’t looked at current King County mortgage rates, that post walks through what buyers are actually paying in 2026. Before committing to either path, it’s also worth running through the total cost of homeownership breakdown — most buyers underestimate the non-mortgage costs by 20–30%.

What the Right Answer Actually Looks Like

The rent vs. buy decision in Bellevue isn’t one-size-fits-all. Here’s a practical framework based on what I see working for buyers in this market:

Lean Toward Continuing to Rent If:

You expect to move within 5 years. You haven’t saved at least 10% down plus closing costs (3–4% of the purchase price). Your debt-to-income ratio would be stretched at current payment levels. You’re not fully qualified yet — understanding mortgage qualification requirements first is a good use of 20 minutes.

Lean Toward Buying If:

You’re planning to stay 10+ years. You have at least $150K–$300K saved for a down payment (or can qualify with DPA assistance at a lower price point). The monthly payment fits comfortably — no more than 28–30% of gross income. You want stability: a fixed mortgage doesn’t go up every year the way rent tends to.

One variable that tilts the analysis more toward buying than the raw monthly numbers suggest: rent inflation. Bellevue rents have historically increased 3–5% per year over time. A fixed-rate mortgage, by contrast, locks your P+I payment permanently. The gap between renting and owning narrows significantly over 10–15 years when you factor in rent escalation.

FAQ: Rent vs. Buy in Bellevue 2026

How much does it cost to buy a home in Bellevue WA in 2026?

The median sale price is approximately $1.45M–$1.6M. A 20% down payment on a $1.5M home is $300,000. At 6.5% on a 30-year fixed, monthly principal and interest is approximately $7,585. Total monthly costs including taxes, insurance, and maintenance typically run $9,500–$10,500/month for a median Bellevue home.

Is it cheaper to rent or buy in Bellevue right now?

Renting is cheaper on a monthly basis for most buyers at current prices and rates. A two-bedroom Bellevue apartment averages roughly $3,100–$4,400/month, compared to $9,500–$10,500/month to own the median home. The ownership case is built on equity accumulation and rate stability over a long horizon, not short-term payment savings.

How long do you need to stay in Bellevue for buying to make financial sense?

In high-cost markets like Bellevue, the break-even timeline is typically 10–16 years when factoring in transaction costs, maintenance, and the opportunity cost of the down payment. If you’re planning a 5-year stay or less, renting likely wins financially.

Are there down payment assistance programs for Bellevue buyers?

Yes. The ARCH East King County DPA program provides up to $50,000 in deferred-loan assistance for eligible buyers. WSHFC Home Advantage offers up to 4% of the loan amount. These programs work best for buyers targeting the lower end of the Bellevue price range — condos and attached homes in the $600K–$800K range.

What’s the price-to-rent ratio in Bellevue?

Bellevue’s price-to-rent ratio is approximately 30–35 based on current median home prices and average rents. Ratios above 25 generally favor renting over buying from a pure monthly-cost perspective.

Should I buy a condo in Bellevue instead of renting?

Bellevue condos in the $600K–$750K range have a more favorable rent-vs-buy comparison than single-family homes. Total monthly costs can be $4,500–$5,200/month — much closer to what two-bedroom apartments cost. If you’re a first-time buyer in Bellevue, this price point deserves a serious look before ruling out homeownership entirely.

Here’s what I tell Bellevue renters who come to me with this question: run your own numbers, not a national average. The right answer depends on your savings, your timeline, your income stability, and how much the idea of a fixed housing cost for 30 years is worth to you. The financial case isn’t as clean as either side makes it sound.

Your guide to life outside Seattle.

253-350-0045 ·

greg@livingoutsideseattle.com ·

www.livingoutsideseattle.com