Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Should I Downsize My Sammamish Home? A Local Agent’s Guide

One question I hear constantly from Sammamish homeowners: “Greg, I have a 3% mortgage rate. Am I crazy to sell?” The way the question gets asked tells me everything. There’s guilt in it. Like they’re about to throw money away.

Here’s what I know from 13+ years of field work evaluating properties across King County: the math is much closer than people think. And sometimes the right answer has nothing to do with the rate.

Let me walk you through how to actually think about this.

Why Sammamish Homeowners Are Downsizing Now (Hint: It’s Not the Rate)

First, context. New listings across King County are up 16.5% year-over-year as of March 2026. That’s not random. It’s rate-locked sellers finally making a move. Why now? Life happens. Kids graduate. Retirement calls. A job changes. And at some point, the rate you’re paying becomes less important than the life you’re living.

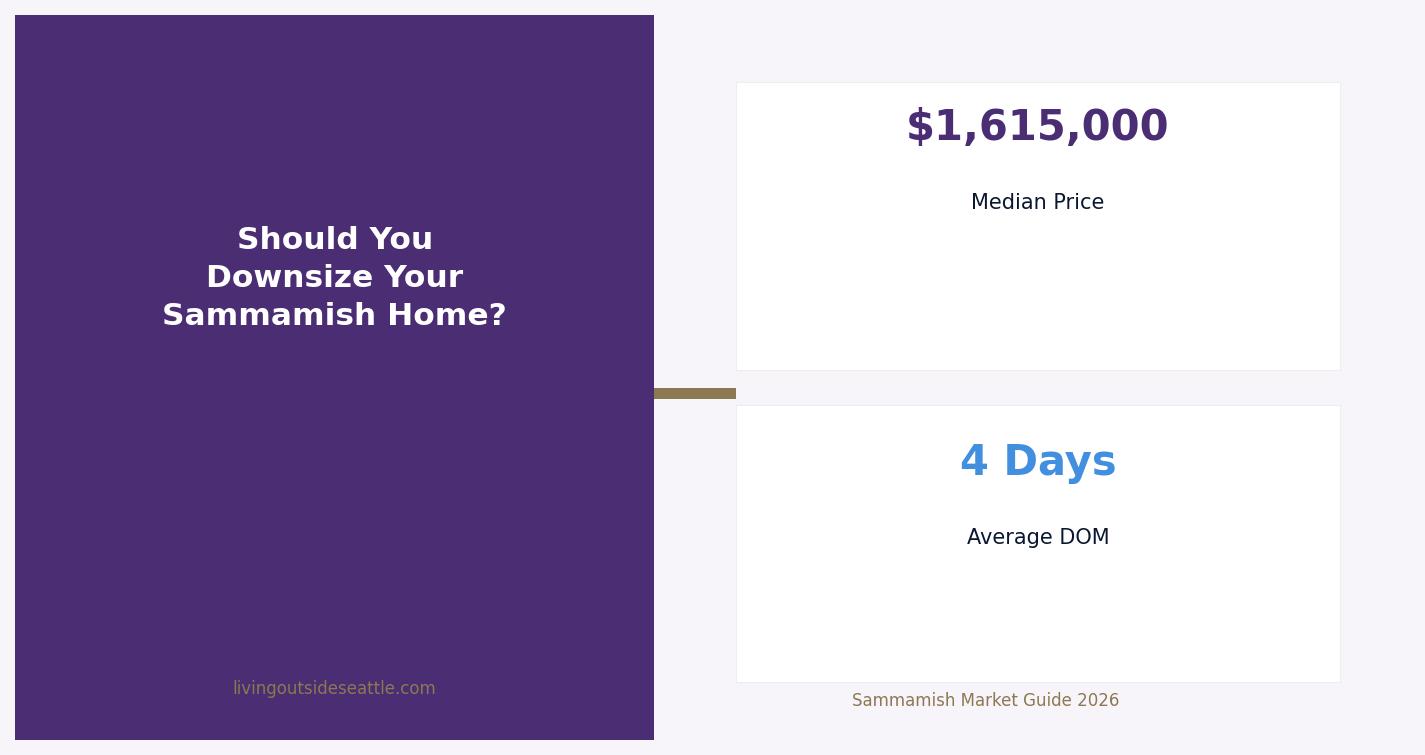

Sammamish inventory sits at 96 homes for sale with a median price of $1,615,000. Homes are moving fast here, too: median 4 days on market. If you’re thinking about downsizing, this is a strong moment to list.

The Financial Reality: What You’ll Actually Pocket Downsizing in Sammamish

Let’s use real numbers. Say you own a Sammamish home worth $1,615,000 today, the March 2026 median. Many of you bought between $800,000 and $1,000,000 when the market was softer. You likely have $600,000 or more in equity.

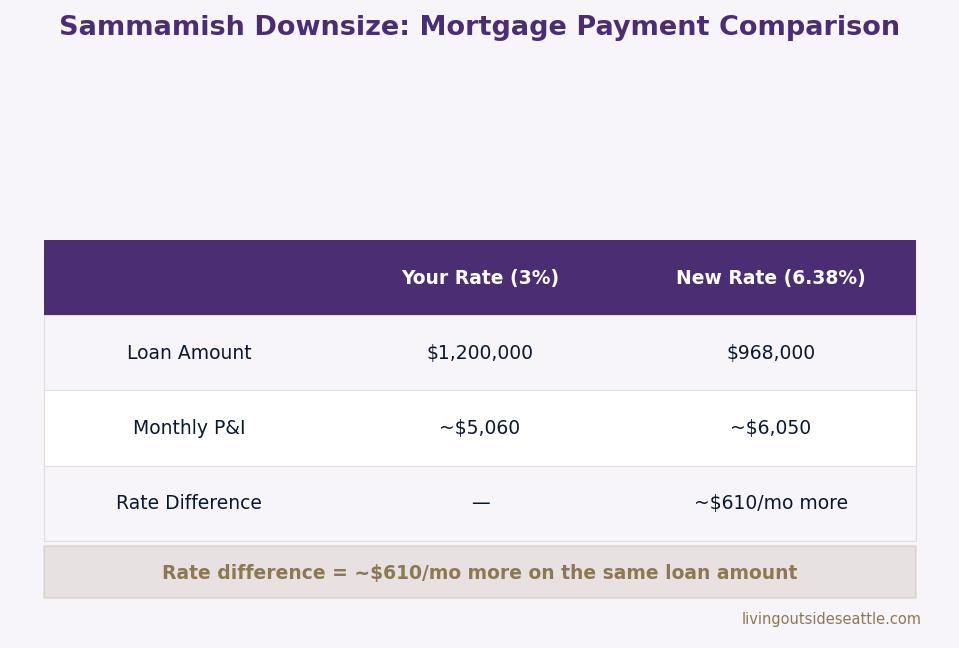

Your current mortgage is $300,000 at 3%. Monthly payment: about $1,265.

Now you sell. After real estate commissions, title, escrow, and loan payoff, you pocket roughly $1,100,000. Not $1,615,000. That’s the number that matters.

You buy a downsized home in Sammamish or nearby for $900,000. You put $600,000 down. Your new mortgage is $300,000 at today’s rate of 6.38%. Monthly payment: about $1,875.

So you pay roughly $610 more per month. Over 30 years, that’s about $220,000. Sounds bad.

But wait. Your old payment was $1,265. Your new payment is $1,875. You also own a home worth $900,000 instead of $1,615,000. You have $700,000 less in property debt. Your net worth shifted, not in dollars, but in flexibility.

Downsizing for the Right Reasons: Life Changes Trump Rate Lock-In

I’ll be honest: the rate differential stings. Going from 3% to 6.38% is real. But here’s what I see when I’m out evaluating homes five or six days a week in Sammamish: people aren’t staying for the payment. They’re staying because they’re afraid to move.

The actual reasons to downsize are not financial. They’re life. You want a single-story instead of managing a second floor with a knee issue. You want less yard to maintain. You want to be closer to downtown Sammamish or Eastside activity. You want to spend your equity on travel or grandkids instead of home maintenance.

Those reasons are worth the rate trade-off more often than the spreadsheet shows.

5 Key Factors Before You Downsize in Sammamish (Beyond the Mortgage Rate)

If you do sell, know this: Sammamish homes in excellent condition are moving at list price or above. The March 2026 list price ratio for Sammamish was 100%. That means homes priced right are getting what they’re listed for. Condition matters enormously. Buyers want move-in ready, even if they plan renovations later.

You’re also looking at capital gains exclusion, which matters. If you’ve lived in your Sammamish home as your primary residence for at least two of the last five years, you can exclude up to $250,000 in gains if you’re single, or $500,000 if you’re married. After 20+ years of ownership, that’s real money.

A 1031 exchange might apply if you’re thinking about investment property, but that’s worth separate analysis with your tax advisor.

The mortgage rate lock-in has felt permanent for a long time. It’s not anymore. Inventory is up, rates are what they are, and homes are still moving. If your reason for downsizing is life, not pure spreadsheet math, the financial piece will sort itself out.

Frequently Asked Questions About Downsizing in Sammamish

At what age should I downsize my Sammamish home?

There’s no “right age.” Most downsizers I work with are 55-70, but I’ve seen 45-year-olds move to single-story homes for simplicity and families with empty nests at any age. The trigger is usually a life change — retirement, health, an empty nest, a lifestyle shift — not a calendar date. Your situation is unique.

Will downsizing to a smaller home in Sammamish actually lower my taxes?

Property tax is assessed on the new home’s value, not savings from the old home. If your new Sammamish home is appraised lower, your annual property tax bill will be lower. You’ll also gain a capital gains exclusion ($250K-$500K depending on filing status) when you sell — that’s where the real tax savings usually come in. Talk to a CPA about your specific situation.

What’s the fastest way to sell my Sammamish home before I downsize?

The fastest option is a cash sale (7 days, but usually at a lower price). The smarter route is listing with an agent — Sammamish homes priced right sell at or above list price and close in 15-30 days. Since condition matters enormously here, a traditional sale often nets more even if it takes a little longer.

Can I do a 1031 exchange when downsizing my Sammamish home?

Only if you’re selling investment property and buying investment property of the same or greater value. If you’re selling your primary residence and buying a smaller primary residence, a 1031 exchange doesn’t apply. But you get the capital gains exclusion instead — often the better deal. Check with a tax advisor for your specific case.

Your guide to life outside Seattle.

253-350-0045 ·

greg@livingoutsideseattle.com ·

www.livingoutsideseattle.com

Gregory Dorrell is a licensed REALTOR® in Washington State (License #111862) with Coldwell Banker Bain. Market data sourced from NWMLS/MLS InfoSparks March 2026. This content is for informational purposes and not financial or tax advice. Please consult a tax advisor regarding capital gains, 1031 exchanges, or other tax implications specific to your situation.