Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

What buyers and sellers in King County need to know — before a low appraisal derails your deal.

The appraisal is one of the quietest steps in a real estate transaction — until it isn’t. Most buyers and sellers go weeks without thinking about it. Then a number comes back lower than the agreed price, and suddenly everyone is scrambling to figure out what happens next.

I’ve seen it go both ways. A clean appraisal that closes without a hiccup. And a deal that almost fell apart because neither the buyer nor the seller understood what options were on the table. Understanding how appraisals work in Washington state — who orders it, what the appraiser is actually measuring, and what you can do when the number doesn’t match — puts you in a much stronger position before you ever get to that moment.

This guide walks through the full process from both sides.

What an Appraisal Actually Is — and Isn’t

A home appraisal is a formal, written opinion of market value prepared by a state-licensed appraiser. It answers one specific question: what would a willing buyer pay a willing seller for this property today, assuming neither party is under pressure and both have full information?

That is not the same as the Zillow estimate. It is not the county assessed value. And it is not what your neighbor’s house sold for last spring, unless that sale is genuinely comparable. Appraisers follow the Uniform Standards of Professional Appraisal Practice (USPAP), a national framework that governs methodology and ethics. The goal is independence — the appraiser works for the lender, not the buyer, not the seller, and not the agent.

This matters because the lender has a direct financial interest in making sure the home is actually worth what they’re about to loan against it. If you borrow $850,000 to buy a house worth $800,000, the lender is immediately underwater. The appraisal is their protection.

As a seller, that means the appraisal isn’t something you control. As a buyer, it means you have a built-in check on whether you’re overpaying — which in competitive markets like South King County, is more useful than it might seem.

How the Appraisal Process Works Step by Step

Who Orders It and When

In a standard financed transaction, the lender orders the appraisal after the purchase agreement is signed and the loan application is underway. They typically assign a licensed appraiser through an Appraisal Management Company (AMC), which keeps the appraiser independent from everyone else in the deal.

You don’t get to choose the appraiser. Your agent doesn’t get to choose the appraiser. This independence is intentional. The appraisal is typically scheduled within one to two weeks of the executed contract, and the full report usually comes back within three to seven business days after the visit.

What Happens During the Visit

The appraiser walks the property, takes measurements, notes the condition of major systems — roof, foundation, HVAC, electrical, plumbing — and documents any updates or upgrades. They’re not doing a home inspection. They’re not looking for problems to flag; they’re forming an objective picture of the property’s physical characteristics and condition relative to the market.

They’ll also photograph the exterior and interior, assess the lot, note the neighborhood, and factor in anything that affects livability or desirability — a busy arterial road that backs up to the property, for example, or a view that doesn’t show up in the tax records.

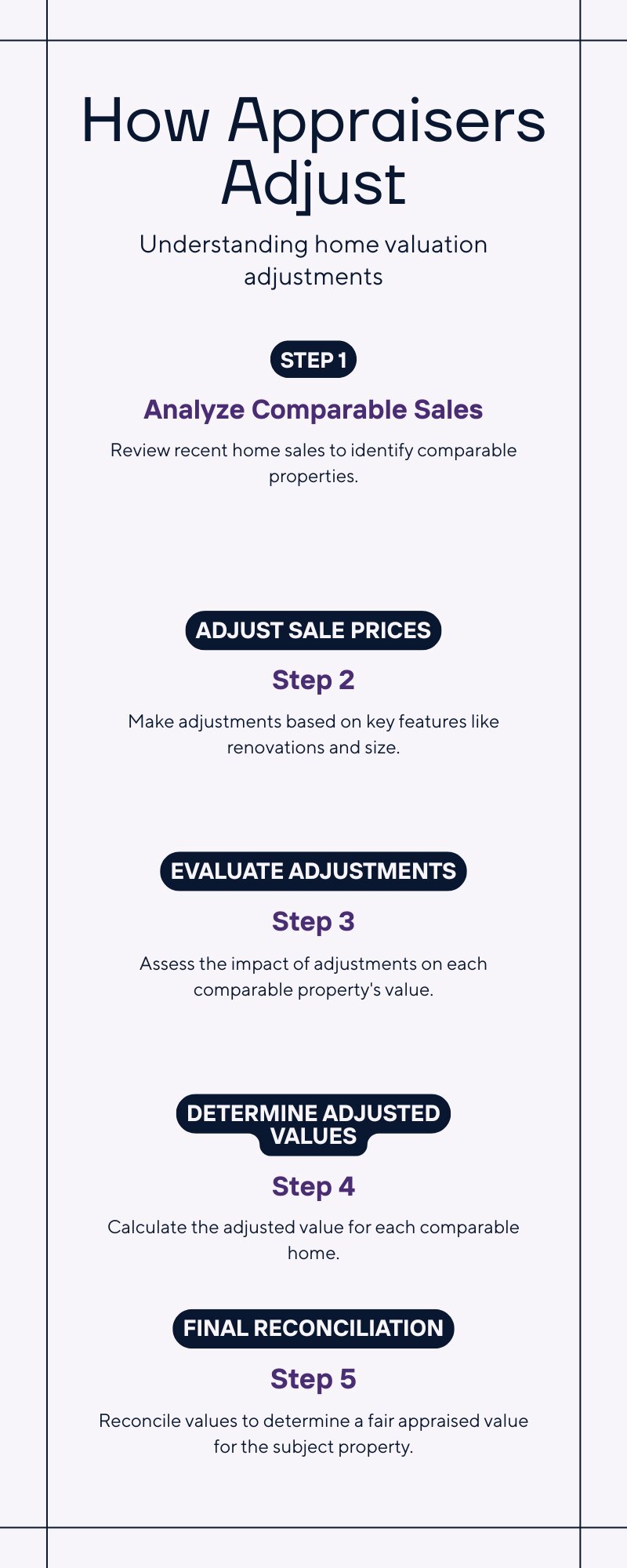

How Appraisers Determine Value

Most residential appraisals in Washington use the Sales Comparison Approach: the appraiser identifies three to five comparable homes (comps) that sold recently, nearby, and in similar condition. “Recently” means within the past six months. “Nearby” in dense King County markets might mean within half a mile; in rural areas like Black Diamond or Enumclaw, the radius might expand to several miles.

Then comes the adjustment process. If a comp sold with a renovated kitchen your home doesn’t have, the appraiser reduces that comp’s adjusted value. If your home has a finished basement the comp didn’t, an upward adjustment goes in. Square footage, lot size, bedroom count, garage, condition, location factors — all of these get adjusted line by line until the appraiser has a cleaned-up, side-by-side comparison. The final number they land on is the reconciled opinion of value.

Appraisers adjust each comparable sale up or down based on differences in size, condition, upgrades, and location — then reconcile a final value from the range.

The King County Context: Why Appraisals Get Complicated Here

King County has some specific dynamics that affect how appraisals play out, and if you’re buying or selling in this market, it helps to know them going in.

Price velocity creates gaps. In fast-moving sub-markets like Renton, Kent, and Auburn, homes sometimes go under contract above asking price quickly. The problem: appraisers can only use closed sales as comps, not active listings or pending contracts. If prices have moved up in the past 90 days, the closed comps the appraiser pulls may not reflect where the market actually is right now. That’s one of the most common reasons appraisals come in below contract price in competitive conditions — and it’s worth understanding before you’re in a multiple-offer situation. Check out the current King County mortgage rate environment for broader context on what buyers are navigating right now.

Appraisal waivers are a real offer strategy. In multiple-offer situations, buyers sometimes waive the appraisal contingency entirely, or offer an “appraisal gap guarantee” — a commitment to cover a certain dollar amount above the appraised value in cash. This is common enough in King County that sellers and their agents have come to expect it on competitive listings. If you’re a buyer competing for a home and you can’t or won’t waive the appraisal contingency, your offer may lose to one that does — even if your price is the same.

New Washington law (effective January 1, 2026) added a twist for off-market deals. Under RCW 61.40.010, if a buyer makes an unsolicited offer on a property that isn’t listed and the seller has no agent, the buyer must pay for an appraisal and the unrepresented seller has a four-day window to back out after receiving the results. This was designed to protect homeowners from being pressured into below-market off-market sales — a real pattern in King County’s investor landscape.

Appraised value vs. assessed value. King County assessors set assessed values for property tax purposes, and they often lag market value by six to eighteen months. Don’t confuse the assessed value on your property tax statement with what an appraiser will determine. They’re calculated differently and serve different purposes. A home assessed at $680,000 for tax purposes can absolutely appraise at $850,000 in today’s market. If you want to understand the broader tax picture when selling, see our guide to capital gains on home sales in Washington state.

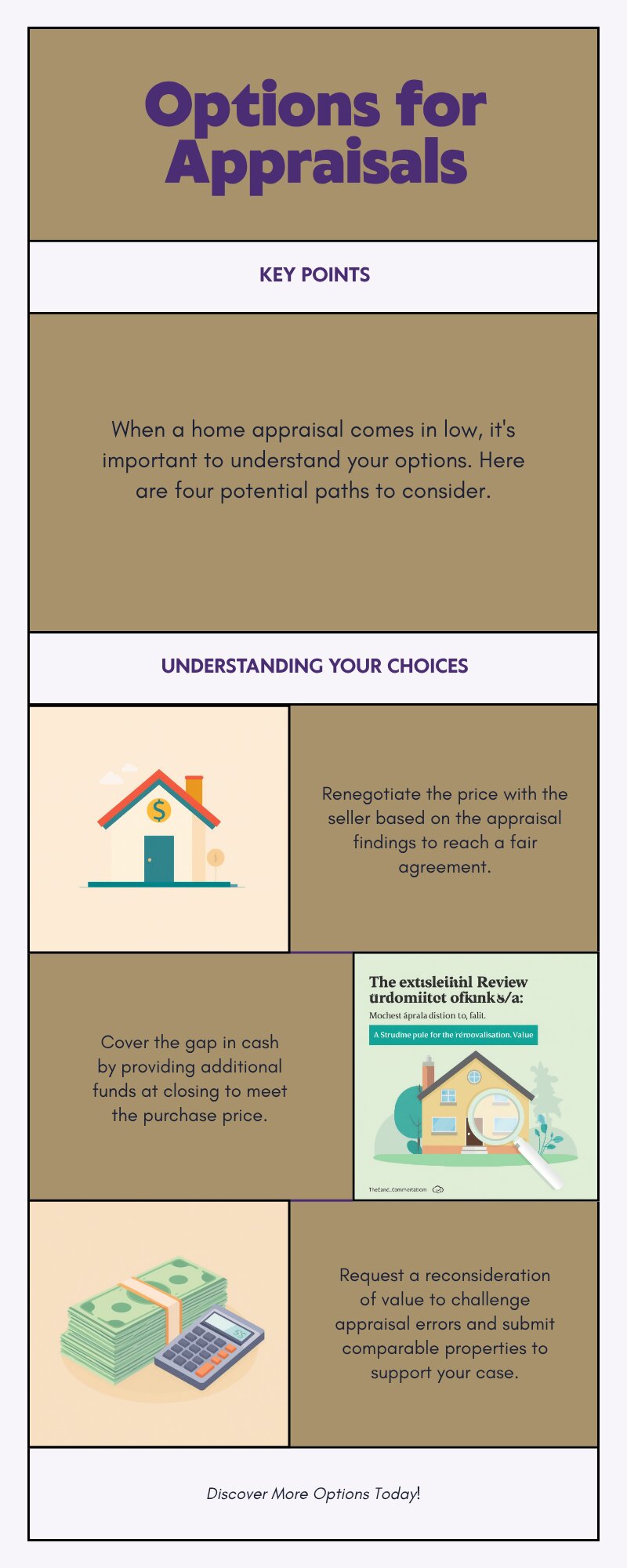

What Happens When the Appraisal Comes In Low

About 8.5% of appraisals come in below the agreed purchase price nationally. In fast-moving markets, that number is higher. When it happens, the lender will only loan based on the appraised value, not the contract price. So if you agreed to pay $900,000 and the appraisal comes in at $860,000, the lender will only underwrite a loan on $860,000. The $40,000 gap has to go somewhere.

Option 1: Renegotiate the Price

The buyer presents the appraisal to the seller and asks them to reduce the price to the appraised value. In a buyer-friendly market, sellers often agree. In a hot market where the seller has backup offers, they may not budge.

Option 2: Cover the Gap in Cash

The buyer brings an additional $40,000 to closing from their own funds to make up the difference. This is the “appraisal gap guarantee” in action. It requires the buyer to have the liquidity to do it.

Option 3: Challenge the Appraisal (ROV)

If the appraiser used weak comps, missed a recent comparable sale, or made a factual error about the property — wrong square footage, missed an update — the buyer’s agent can formally request a Reconsideration of Value (ROV) through the lender. This is not a guarantee of a different number, but legitimate errors do get corrected. Submit recent sales the appraiser missed, document discrepancies, and let the process work.

Cancel the contract. If the buyer has a standard appraisal contingency in place and the gap can’t be resolved, they can cancel and get their earnest money back. This is the protection the contingency provides — and it’s the only option that ends the deal.

A low appraisal doesn’t have to end the deal. Four paths exist — and only one of them means canceling the contract.

How to Protect Yourself as a Seller

A few things sellers can do before the appraiser even shows up:

Make sure the home is clean and accessible. Appraisers aren’t swayed by staging, but physical condition matters. A cluttered, poorly lit home can look worse than it is. An appraiser who can’t access the attic or crawlspace notes it.

Prepare a comp package. Your agent can pull relevant comparable sales and present them to the appraiser at or before the visit. This doesn’t influence the appraiser’s independence — they’ll do their own research — but it ensures they’re aware of strong comps they might otherwise miss, especially if they’re not hyperlocally familiar with your specific neighborhood. See our guide on how to price your home to sell in King County for more on the comp selection process.

Disclose major updates with documentation. New roof, HVAC, kitchen renovation, ADU added — document the dates and costs. Appraisers make upward adjustments for improvements, but they need to know about them. Don’t assume it’s obvious.

Consider a pre-listing appraisal. For higher-value or unusual properties where standard comps are hard to find, a pre-listing appraisal ($400–$900) gives you an independent data point before you price the home and before a buyer’s lender gets involved. For more on getting your home ready before listing, see how to prepare your home for sale in King County.

How to Protect Yourself as a Buyer

Keep the appraisal contingency in place unless you’re prepared to cover the gap. The contingency exists to protect you. Waiving it means you’re on the hook for the full purchase price no matter what the appraiser says. Only waive it if you’ve done the math on the gap you could realistically face and you’re prepared to cover it.

Understand the difference between appraised value and market value. If ten other buyers are willing to pay $900,000 and the appraisal comes in at $860,000, the market value is arguably closer to $900,000. Appraisals are backward-looking by design — they’re based on what sold, not what competing buyers are currently bidding. In fast-rising neighborhoods, this lag is real and it favors sellers.

Ask your lender about appraisal waivers before you make an offer. Some conventional loan programs (Fannie Mae, Freddie Mac) allow automated valuation models to stand in for a full appraisal under certain conditions — generally when the loan-to-value ratio is low and the data quality is high. If you qualify for a waiver, you avoid the process entirely. Your lender will know whether your specific loan profile qualifies.

Sellers and buyers face different appraisal risks. A few simple steps before the appraiser visits can make a meaningful difference in how the process goes.

What This Means for You in King County Right Now

The King County market in 2026 is more balanced than it was in 2021 and 2022, but it’s not uniform. South King County sub-markets — Renton, Kent, Auburn, Covington — are still moving faster than the county average, with median days on market well under 30. In those conditions, appraisal gaps remain a real possibility, especially on homes priced above $750,000 where comps thin out.

For sellers in those markets, pricing accuracy matters more than ever. A home priced right at market value has a much better chance of appraising at contract price. A home priced at the high edge of the range, hoping for a bidding war, risks the appraisal gap problem — which puts the deal back in negotiation right when you thought it was done.

Frequently Asked Questions

How much does a home appraisal cost in Washington state?

In King County, expect $400–$900 for a standard single-family appraisal. Complex properties, acreage homes, or homes in more rural areas (Black Diamond, Enumclaw) may run higher. The buyer pays the appraisal fee as part of closing costs.

How long does an appraisal take in Washington state?

The appraiser typically completes the site visit within one to two weeks of the purchase agreement being signed. The written report usually comes back three to seven business days after the visit. Total time from contract to receiving the appraisal: roughly two to three weeks.

Can a seller refuse to let an appraiser in?

Technically yes, but refusing the appraisal kills the buyer’s financing and ends the deal. Under the terms of most purchase agreements, the seller is expected to provide reasonable access. A refusal to cooperate is effectively a decision to blow up the transaction.

What is a Reconsideration of Value (ROV) in Washington?

An ROV is a formal request to the lender asking the appraiser to reconsider the value based on new information — comparable sales the appraiser missed, factual errors in the report, or evidence the adjustments were unreasonable. It does not guarantee a different outcome, but it is a legitimate tool when the original report contains real errors or omissions.

What’s the difference between appraised value and assessed value in King County?

Assessed value is set by the King County Assessor’s office for property tax purposes and typically lags market value by six to eighteen months. Appraised value is determined by a licensed appraiser for a lending transaction, using current comparable sales. They’re calculated differently and serve different purposes. Don’t use your property tax statement to set your list price.

Do appraisals expire?

Yes. Most lenders will only accept an appraisal completed within 120 days (four months) of the loan closing date. If your deal takes longer than expected, the lender may require a reappraisal or an update to the original report.

The appraisal doesn’t have to be the part of the transaction that surprises you. If you’re selling, a solid pricing strategy from the start gives you the best shot at a clean appraisal. If you’re buying, understanding your options before you’re in contract — not after the number comes back low — puts you in control of what happens next.

Your guide to life outside Seattle.

253-350-0045 ·

greg@livingoutsideseattle.com ·

www.livingoutsideseattle.com