Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Renting Out Your King County Home vs. Selling: A Financial Comparison

Should you become a landlord or cash out? Here’s the real math King County homeowners need before making this call.

If you’ve been sitting on a home in Renton, Kent, Auburn, or anywhere in South or East King County, you’ve probably had this thought: what if I just rented it out instead of selling? Especially with home values still holding strong — median prices around $859,000 countywide in spring 2026 — the idea of collecting rent every month while your property appreciates sounds appealing.

But the math is more complicated than it looks on paper. And Washington’s landlord-tenant laws changed significantly in 2025, adding rules most homeowners-turned-landlords don’t know about until it’s too late.

This post walks through both sides of the decision — actual rental income projections, net sale proceeds, tax implications, cash flow math, and the real-world landlord responsibilities that don’t show up in the rosy scenarios. By the time you’re done reading, you’ll know which option makes more financial sense for your situation.

The Rental Income Side: What King County Homes Actually Rent For

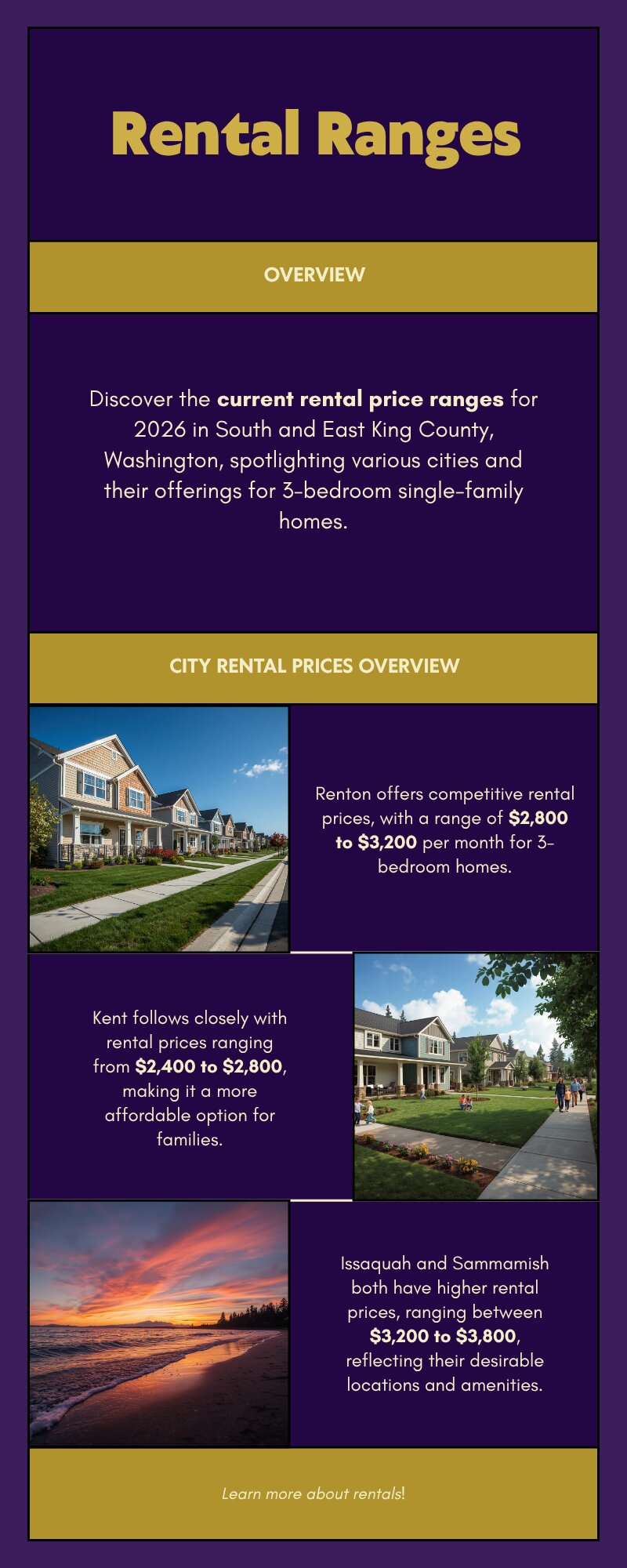

Let’s start with what you could realistically collect in rent. King County single-family rental rates in 2026 vary a lot by city and home size, but here are realistic ranges for typical South and East King County homes.

Three-bedroom single-family homes in Renton are pulling $2,800 to $3,200 per month. In Kent, the range is closer to $2,400 to $2,800. Auburn runs slightly lower, typically $2,200 to $2,600 for a comparable home. Move east to Issaquah or Sammamish, and a three-bedroom can fetch $3,200 to $3,800 monthly.

Sounds like solid money. But gross rent is not your income. Your net cash flow depends on what you owe and what it costs to run the property.

Here’s a real example. Say you own a three-bedroom home in Renton worth $700,000. You bought it five years ago, your current mortgage balance is $480,000, and your rate is 4.5%. Your monthly carrying costs look something like this:

Monthly Carrying Costs — High Mortgage Scenario

Mortgage P&I at 4.5% on $480K balance: ~$2,430

Property taxes (King County ~1.0% annually): ~$583/month

Landlord insurance (~15% more than owner-occupied): ~$150/month

Maintenance reserve (1% of value per year / 12): ~$583/month

Total carrying costs: ~$3,746/month

At $3,000 rent: -$746/month before vacancy or management fees

If you hired a property manager — which handles tenant screening, rent collection, and maintenance coordination — expect to pay 8% to 10% of gross rent, or another $240 to $300 per month on top of that negative.

That scenario doesn’t cash flow. It costs you money every month to keep it.

Now flip it. Same Renton home, but you paid it down to $300,000 and your rate is 3.0% from a 2021 refinance. Monthly P&I drops to approximately $1,265. Suddenly the same $3,000 rent gives you positive cash flow after all expenses. That’s the home where keeping it as a rental makes financial sense.

Two scenarios, same rent. The only thing that changes the outcome is what you owe. Run your actual numbers before deciding.

The Sale Side: What You Actually Walk Away With

When you sell, you get a lump sum. But net proceeds are not the same as your home’s sale price. Here’s what comes out.

Real Estate Excise Tax (REET) in King County runs approximately 1.78% of the sale price on a home in the $700,000 to $1.5 million range. On a $700,000 sale, that’s $12,460. Agent commissions typically run 5% to 6% total — on $700,000, that’s $35,000 to $42,000. Closing costs — title insurance, escrow, pro-rated taxes — add another $3,000 to $5,000.

So on a $700,000 sale, you might net $635,000 to $649,000 before any mortgage payoff. Subtract the $480,000 balance, and you walk away with roughly $155,000 to $169,000 in cash. That’s a down payment on your next home, a fully funded investment account, or two years of rental losses avoided.

If you’re in a lower-equity position — say $300,000 owed on a $700,000 home — the sale gives you approximately $355,000 to $369,000 cash in hand. Now the math shifts. Holding the property becomes more interesting because you have equity working for you every year.

Tax Implications: Where Things Get Complicated

This is the part most homeowners don’t think through carefully enough.

If you sell your primary residence, Washington’s $500,000 capital gains exclusion (for married couples; $250,000 for single filers) likely protects your gain from federal tax entirely, provided you’ve lived there two of the last five years. Washington state has no income tax, so there’s no state capital gains tax on primary residence sales either. You pay REET at closing and that’s largely it. For a full breakdown of how Washington taxes work on a home sale, see our guide to capital gains on home sales in Washington State.

If you convert to a rental and sell later, the tax picture changes. Once you stop living there as your primary residence, you start losing your exclusion eligibility. Sell after the two-year primary-residence window closes, and your gain becomes a taxable long-term capital gain at the federal level — 15% or 20% depending on your income bracket, plus potentially a 3.8% Net Investment Income Tax if your household income exceeds $250,000.

There’s also depreciation recapture to account for. Once you convert to a rental, the IRS lets you deduct depreciation each year — roughly 1/27.5 of the structure’s value annually. When you eventually sell, the IRS recaptures that depreciation at up to 25%. That can be a meaningful surprise at tax time.

The two-year primary residence window is the biggest tax variable in this decision. Once it closes, your sale proceeds become a taxable event.

Washington Landlord Law in 2026: What Changed

Before you decide to rent, you need to know that Washington’s landlord-tenant laws shifted significantly starting in 2025. These aren’t small tweaks — they meaningfully change what it means to be a landlord here.

Rent Stabilization (HB 1217)

Effective May 2025, annual rent increases are capped at 7% plus CPI, or 10%, whichever is lower. For 2026, the maximum is 9.683%. You cannot raise rent at all during the first 12 months of a tenancy. Any increase requires 90 days written notice using a state-standardized form sent via certified mail.

What this means for you: if rents rise faster than that cap, you can’t keep pace. If a great tenant moves in at below-market rent, you’re limited in how quickly you can adjust.

Just Cause Eviction Requirements

You can’t simply decide not to renew a lease at the end of the term. You need a legally recognized reason — nonpayment, lease violation, owner move-in, or a handful of other specific grounds.

Eviction timelines are not quick. Nonpayment requires a 14-day notice before you can file. Most violations require a 10-day notice to comply. Court processes add weeks or months. Evicting a non-paying tenant in King County can realistically take three to six months — during which you carry all costs with no rent coming in.

The Local Angle: King County Specifics That Change the Math

A few things about King County shift the calculus compared to national averages.

Property taxes here are real. King County’s effective property tax rate runs around 0.93% to 1.1% depending on city and levy district. On a $700,000 home, that’s $6,500 to $7,700 per year — a cost that doesn’t go away when you become a landlord. And unlike a primary residence, you can’t homestead-exempt your way to a lower bill.

Current King County mortgage rates sit around 6.4% in mid-2026. If you bought in the last two to three years at these rates, your P&I is substantially higher than someone who refinanced in 2021. That gap is often what separates a cash-flowing rental from a money-losing one.

The rental market is competitive but not unlimited. Rents have stayed strong in South King County, but they’ve also flattened. Rent growth has run around 4% year over year in the broader Seattle metro, but Washington’s new stabilization caps limit how much future increases can catch up.

Home appreciation is still the strongest long-term argument for the rental side. If your home appreciates 3% to 4% annually from a $700,000 base, that’s $21,000 to $28,000 per year in equity gain. Even if you’re slightly cash-flow negative on rent, appreciation can still make the investment pencil out — if you’re patient and prepared for the landlord role.

South King County in particular — Renton, Kent, Auburn, Covington — remains a strong long-term hold for landlords who are disciplined about tenant selection and maintenance. These are stable demand markets with diverse employment bases. But that’s a different conversation than “I’ll rent it out for a year and see how it goes.”

South King County rents are strong but not unlimited. Your specific city, neighborhood, and home condition determine the real number you’ll collect.

When Renting Makes Financial Sense

Based on the math and the landlord landscape, here’s when keeping the property and renting usually wins.

You have a low-rate mortgage (under 4%) that generates positive monthly cash flow after all expenses. Your principal balance is low relative to value — meaning the equity is working for you as an asset even if rent doesn’t fully cover costs. You’re planning to return and live in the home within three to five years, preserving your primary residence exclusion. Or you’re committed to building a rental portfolio long-term and understand that this first property is an investment, not passive income.

When Selling Makes More Sense

Selling wins when you have a high-rate or high-balance mortgage that won’t cash flow at current rents. When your equity is substantial and a lump sum now serves your goals better than monthly income later. When you want simplicity — no tenant calls, no maintenance surprises, no navigating the 90-day rent increase notice process. Or when you need to deploy that equity into your next home and you can’t do both.

If you decide to sell, you’ll want to prepare your home strategically and price it right from day one — two steps that consistently separate fast, full-price sales from drawn-out ones.

What This Means for You

If you’re weighing this decision right now, here’s a simple three-step filter before you call anyone.

First, run your actual monthly carry cost — mortgage P&I, taxes, insurance, and a 1% annual maintenance reserve divided by 12. Compare that to realistic rent for your specific home and neighborhood, not the top of the range.

Second, calculate your net sale proceeds. Look at your current loan payoff, subtract estimated closing costs and agent fees, and ask yourself whether that lump sum helps you more than the monthly difference between rent and expenses.

Third, get a real conversation with a tax professional about your gain and your exclusion window. If you’ve lived in the home two of the last five years, the clock is ticking on that federal exclusion. Don’t let it expire accidentally while you’re hoping the rental market improves.

I can walk you through the numbers on your specific home — no obligation, no pressure. If renting makes more sense, I’ll tell you that. If selling makes more sense, I’ll tell you that too.

FAQ: Renting Out vs. Selling Your King County Home

Can I rent out my King County home and still avoid capital gains tax when I sell later?

Only if you sell within the IRS’s primary residence window — you must have lived in the home two of the last five years when you sell. If you rent it out for more than three years before selling, you lose the $250,000/$500,000 federal exclusion. Washington state has no capital gains tax, but federal tax on investment property gains runs 15–20% plus potential Net Investment Income Tax.

What can I realistically charge for rent on a King County single-family home in 2026?

A three-bedroom home in South King County (Renton, Kent, Auburn) typically rents for $2,400 to $3,200 per month depending on condition, location, and size. East King County (Issaquah, Sammamish, Bellevue) runs higher, often $3,200 to $3,800 for a comparable home.

Does Washington state have rent control in 2026?

Yes, as of May 2025. Under HB 1217, annual rent increases are capped at 7% plus CPI, or 10%, whichever is lower. For 2026, the cap is 9.683%. You can’t raise rent in the first 12 months of a tenancy, and you must give 90 days written notice — certified mail, state-standardized form — before any increase.

How long does it take to evict a non-paying tenant in King County?

Realistically, three to six months from missed payment to vacant possession. You must issue a 14-day pay-or-vacate notice, file in court if they don’t comply, wait for a hearing, and execute the order. During that entire period you’re carrying costs with no rent. Landlord insurance with loss-of-rent coverage can offset some of this risk.

Should I hire a property manager if I rent out my King County home?

For most first-time landlords, yes. A professional property manager handles tenant screening, lease compliance under Washington’s updated laws, maintenance coordination, and the 90-day rent increase documentation process. Typical fees run 8–10% of gross rent monthly. That cost is real, but so is the protection it provides.

What’s the real estate excise tax (REET) on selling my home in King County?

REET is graduated in Washington. On homes selling between $700,000 and $1.5 million, the effective combined rate runs approximately 1.28% to 2.5% depending on the price tier. For a $700,000 sale, budget roughly $12,000 to $13,000 for REET at closing. It comes out of proceeds automatically at the title company.

The decision between renting and selling isn’t one-size-fits-all. It’s a math problem that looks different for every household depending on what you owe, what you’d net, and what you actually want your life to look like over the next three to five years. Run the numbers honestly — including the ones people usually skip — and the right answer tends to become obvious.

Your guide to life outside Seattle.

253-350-0045 ·

greg@livingoutsideseattle.com ·

www.livingoutsideseattle.com