Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

How first-time buyers in King County can get up to $45,000 — or more — toward their down payment right now.

The number I hear most from first-time buyers in King County is not the interest rate. It is the down payment. At a $700,000 median price, even a 5% down payment is $35,000 — and that is before closing costs. That is a lot of money to save on top of rent in one of the most expensive metros in the country.

What most buyers do not know is that there are programs specifically designed to close that gap. Some are state programs. Some are regional. A few are city-specific. And in many cases, you can combine them. I work with buyers across South and East King County every week, and the down payment question comes up in almost every first conversation. This guide breaks down every major program available right now, what they actually pay, and how to get the money working for you.

Understanding your financing options is the foundation. If you want to see how King County mortgage rates affect your monthly payment alongside these programs, read King County Mortgage Rates 2026: What Buyers Are Actually Paying first.

What Is Down Payment Assistance and How Does It Work?

Down payment assistance — DPA for short — is money that a government agency, housing authority, or nonprofit makes available to help first-time buyers cover the upfront cash required to purchase a home. It is not a gift in most cases. Most programs are structured as a deferred second mortgage: you borrow the money at zero percent or very low interest, and you do not make payments on it. You repay it when you sell, refinance, or pay off the home.

That structure matters. It means the money costs you almost nothing while you own the home. You are essentially borrowing from your future equity instead of draining your savings account today.

To use DPA, you pair it with a regular first mortgage — FHA, conventional, VA, or USDA. The DPA funds cover part or all of the down payment and sometimes closing costs. Your lender handles the mechanics. You apply through a participating lender, not directly through the DPA program.

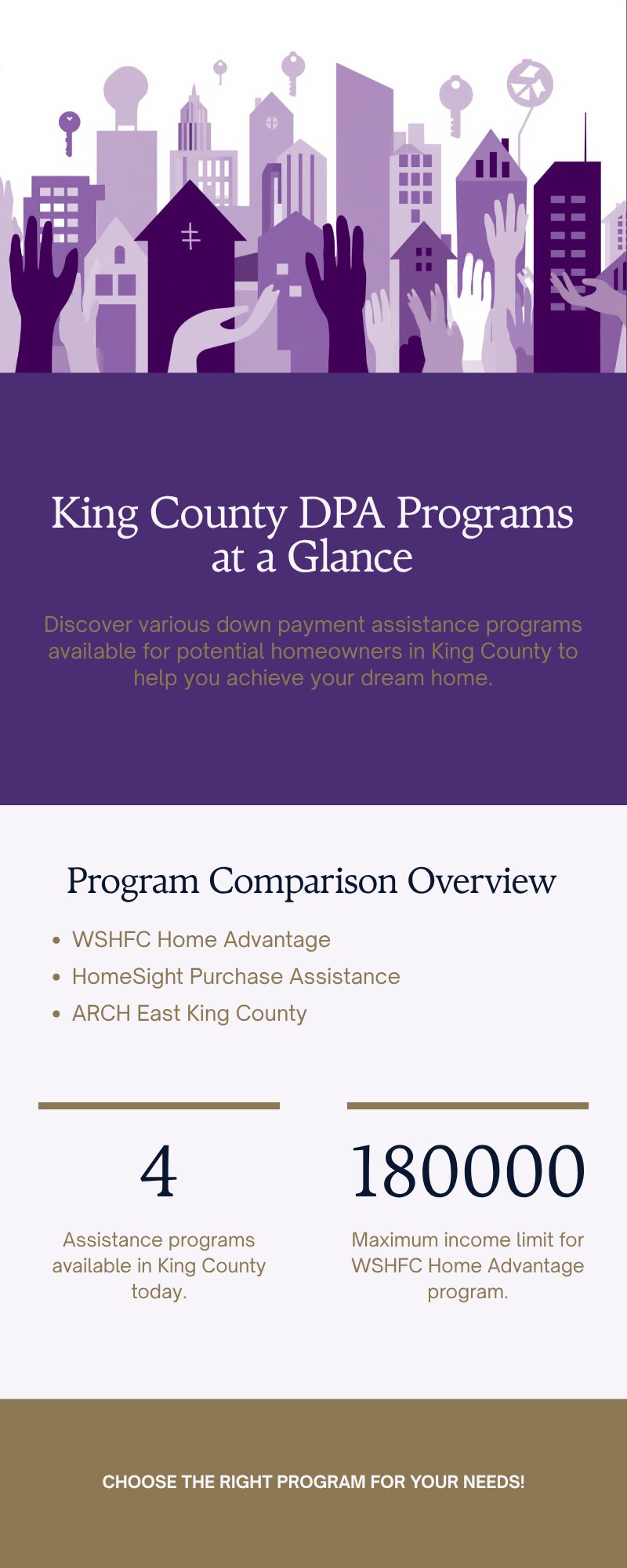

The Main Programs Available to King County Buyers

Four programs, four different income and geography profiles. Most buyers qualify for at least one — many qualify for two.

WSHFC Home Advantage

The Washington State Housing Finance Commission’s Home Advantage program is the most widely used DPA program in the state. It has the highest income limit — $180,000 for all household sizes in King County — which means a lot of buyers who assume they earn too much will actually qualify.

Here is how the down payment assistance piece works: you get up to 5% of the first mortgage loan amount as a second mortgage at 0% interest, deferred for 30 years. On a $700,000 home with a $665,000 mortgage, that is up to $33,250 toward your down payment. No monthly payment. No interest accruing. You pay it back when you sell or refinance.

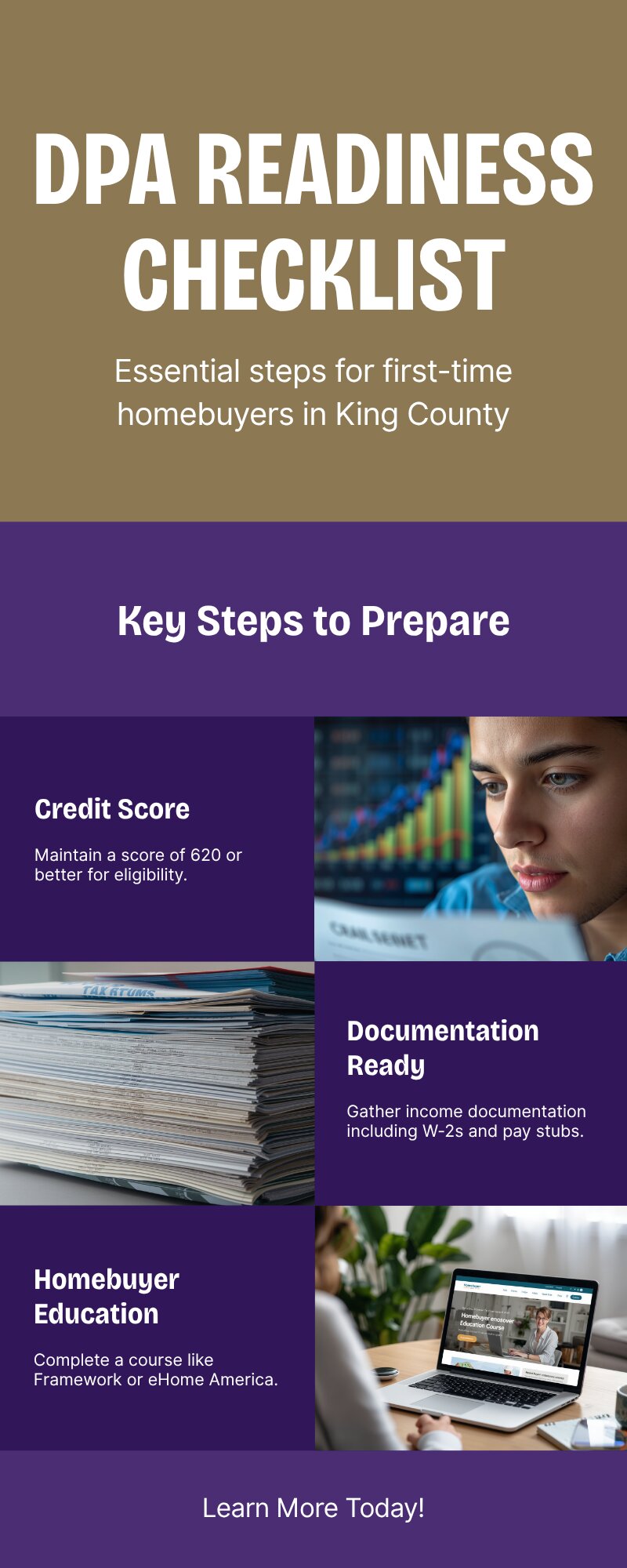

The first mortgage is a 30-year fixed rate through a participating lender. You must have a credit score of at least 620 and complete a five-hour homebuyer education course through Framework or eHome America. The course can be done online in a single afternoon.

HomeSight Purchase Assistance (South King County)

HomeSight is a Seattle-based nonprofit HUD-approved housing counseling agency, and their Purchase Assistance program is the most generous option for buyers in South King County cities. If you are shopping in Auburn, Federal Way, Tukwila, or unincorporated King County, this program can provide up to $45,000 in down payment assistance structured as a 3% deferred loan for 30 years.

The income limit is 80% of Area Median Income. For a family of four in King County, 80% AMI is approximately $112,000 in 2026. That is lower than WSHFC’s ceiling, but the dollar amount is higher — so buyers who fit within the income band can access substantially more cash up front.

HomeSight also offers homebuyer education and one-on-one counseling. Reach them at 206-723-4355 or homesightwa.org. Given that this program serves the exact cities where I work most — Federal Way, Auburn, Kent — it is worth a call early in your search, not after you have found a house.

ARCH East King County Downpayment Assistance

If you are buying in East King County, the ARCH program is what to look at first. ARCH member cities include Bellevue, Issaquah, Kirkland, Redmond, Sammamish, Kenmore, Bothell, Newcastle, Woodinville, and a handful of smaller communities.

The program provides up to $30,000 as a deferred loan at 4% simple interest. The income limits range from about $50,400 for a one-person household to $95,050 for a household of eight. The purchase price limit is $373,000 for the assisted unit, which limits this program to condos and lower-priced homes in the ARCH area rather than single-family houses at current market prices.

That price limit is the honest caution with ARCH: at current East King County prices, this program works best for condo buyers or buyers in specific affordable housing units the program designates. If you are looking at a $650,000 townhouse in Sammamish, WSHFC Home Advantage will likely be more useful.

WSHFC Opportunity Downpayment Assistance

The Opportunity program pairs with WSHFC’s House Key Opportunity first mortgage, targeted to buyers in certain income bands and geographic “targeted areas” — lower-income census tracts where the first-time buyer rule is waived. The DPA here is up to $15,000 at 1% simple interest, deferred for 30 years. It is a solid option for buyers in targeted areas of Kent, Auburn, and Renton who want a slightly larger fixed dollar amount than the Needs-Based program provides.

The King County Angle: Why These Programs Matter More Here

King County median home prices sit above $700,000 as of spring 2026. At that price point, a conventional 5% down payment is $35,000 — and that figure does not include the 2% to 3% in closing costs you will also owe at the table. Combined, a buyer needs $49,000 to $56,000 in cash just to close.

DPA programs cut directly into that number. A buyer using WSHFC Home Advantage on a $665,000 loan gets roughly $33,000 in down payment assistance, which means they need to bring approximately $2,000 to $5,000 of their own cash to close rather than $49,000. That is the difference between buying in 2026 and waiting another three years.

South King County matters particularly here. In cities like Federal Way, Kent, and Auburn, median prices are lower than the county overall — often in the $550,000 to $650,000 range — which means the income limits on programs like HomeSight are more accessible and the purchase prices are within reach. These are the markets where DPA programs do their best work because buyers have realistic targets and the assistance closes the gap meaningfully.

How to Stack Multiple Programs

You can combine certain DPA programs to increase your total assistance. This is called stacking, and it is legal and common when done correctly.

The most practical stack for King County buyers is WSHFC Home Advantage (5% DPA) plus WSHFC Needs-Based assistance ($10,000 fixed) if you qualify for the lower income tier. A participating lender can structure both as simultaneous second mortgages on the same transaction.

Buyers in HomeSight’s service area may be able to combine HomeSight assistance with a first mortgage that has its own DPA feature — ask your lender specifically about this before assuming the programs can be combined, because some programs prohibit layering.

One thing to know: the more DPA you layer, the more important it is to work with a lender who has experience with these specific program combinations. A loan officer who has never done a stacked WSHFC transaction will slow everything down. Ask upfront: “Have you closed stacked WSHFC loans before?”

What Buyers Get Wrong About DPA

The biggest misconception I see is that buyers think these programs are for people in financial trouble. They are not. They are for people who have income, credit, and stable employment but have not had enough years to save a down payment at King County prices. Most DPA recipients are working professionals — nurses, teachers, city employees, tech workers at smaller firms — who earn good incomes but have been renting while prices outran their savings rate.

The second misconception is that applying for DPA slows down the purchase or makes your offer look weak to sellers. It does not affect the timeline in any significant way — DPA is financed through the same closing process as any other transaction. Sellers do not see your financing source, only your terms and your pre-approval letter.

The third thing buyers miss: the homebuyer education requirement is not a hoop to jump through. The five-hour Framework course covers budgeting, loan types, the offer process, and what happens at closing. Every first-time buyer I work with who has taken it says it reduced their stress level. Do it early in the process, before you start touring homes.

Run through this checklist before contacting a lender. Having these items ready speeds up the pre-approval and DPA approval process.

What This Means for First-Time Buyers in King County

If you are renting right now and thinking about buying in South or East King County, the first practical step is not finding a house. It is finding a WSHFC-approved lender, telling them your income and credit score, and asking which DPA programs you qualify for. That conversation takes 20 minutes and tells you exactly how much assistance you can access.

After that conversation, you will know your real buying budget: not just what you qualify to borrow, but how much cash you actually need to bring to closing. In most cases, that number is much smaller than buyers expect.

Once you know your DPA amount, you will have a much clearer picture of what you can afford and where. If you are still deciding between a condo and a house, check out Should I Buy a Condo or House in King County Right Now? — it breaks down the cost, lifestyle, and financing differences at current prices.

Frequently Asked Questions

Do I have to be a first-time buyer to use these programs?

Most DPA programs define “first-time buyer” as someone who has not owned a home in the past three years. If it has been more than three years since you last owned, you qualify. There are also exceptions for targeted geographic areas where the first-time buyer rule is waived entirely.

Can I use down payment assistance with an FHA loan?

Yes. WSHFC Home Advantage is compatible with FHA loans. FHA requires 3.5% down with a 580+ credit score, and the DPA can cover that amount. The two programs work together through the same lender and close at the same time. If you are deciding between FHA and conventional, see FHA vs. Conventional Loan in King County: Which Is Right for First-Time Buyers? for a side-by-side breakdown.

What happens to the DPA loan if I sell my home?

You repay the deferred second mortgage from your sale proceeds, just like you would repay any other lien on the property. If your home has appreciated, you are repaying a fixed dollar amount from a larger equity pool — most sellers find this is a very manageable part of the transaction.

How long does it take to get approved for a DPA program?

The DPA approval runs in parallel with your first mortgage approval — it does not add extra time as long as you are working with an experienced participating lender. The only real time commitment is the homebuyer education course, which you can complete in a single day online.

Are there income limits I need to know about?

Yes, and they vary by program. WSHFC Home Advantage has the highest limit at $180,000 for King County. HomeSight caps at 80% AMI (roughly $112,000 for a family of four). ARCH has lower limits ranging from $50,400 to $95,050 depending on household size. Your lender will check your income against each program you might qualify for.

Does using DPA affect my interest rate?

The WSHFC Home Advantage first mortgage rate is set by the Commission and is typically very close to market rates — sometimes slightly better because it is a bulk-purchased rate. The DPA second mortgage is at 0%, so it does not affect your monthly payment at all.

Your guide to life outside Seattle.

253-350-0045 ·

greg@livingoutsideseattle.com ·

www.livingoutsideseattle.com