Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Rate Buydown Explained: What King County Buyers Need to Know

A plain-English look at how a mortgage rate buydown works, what it costs, and when it beats negotiating a lower price in King County.

If you have shopped for a home in King County lately, you have probably heard someone mention a “rate buydown.” Maybe your loan officer brought it up. Maybe a listing said the seller would help with one. And maybe you nodded along while quietly wondering what it actually means.

You are not alone. A rate buydown is one of the most useful tools a buyer has right now, and it is also one of the most misunderstood. With 30-year fixed rates sitting in the mid-6% range here in Washington this summer, a buydown can knock real money off your payment in the early years of your loan. If you want to see where rates have been running locally, my breakdown of King County mortgage rates in 2026 lays out the payment math. The catch with a buydown is that it only helps if you understand what you are getting and who pays for it.

Let me walk you through the whole thing the way I would explain it to a client sitting across my desk. By the end you will know the difference between a temporary and a permanent buydown, what each one costs, and how to ask a Renton or Kent seller to pay for it.

What a Rate Buydown Actually Is

A rate buydown means you pay money at closing to get a lower interest rate. That is the whole idea in one sentence.

The money can come from you, the seller, or sometimes a builder. In exchange, your monthly payment drops. The size of the drop and how long it lasts depends on which kind of buydown you choose. There are two main types, and they work very differently.

So why does this matter to you? Because a lower rate means a lower payment, and a lower payment is what gets a lot of King County buyers across the finish line. When a $650,000 home feels just out of reach, a buydown can be the difference between qualifying and walking away. If you are still figuring out what you can borrow in the first place, start with how mortgage qualification works in Washington State.

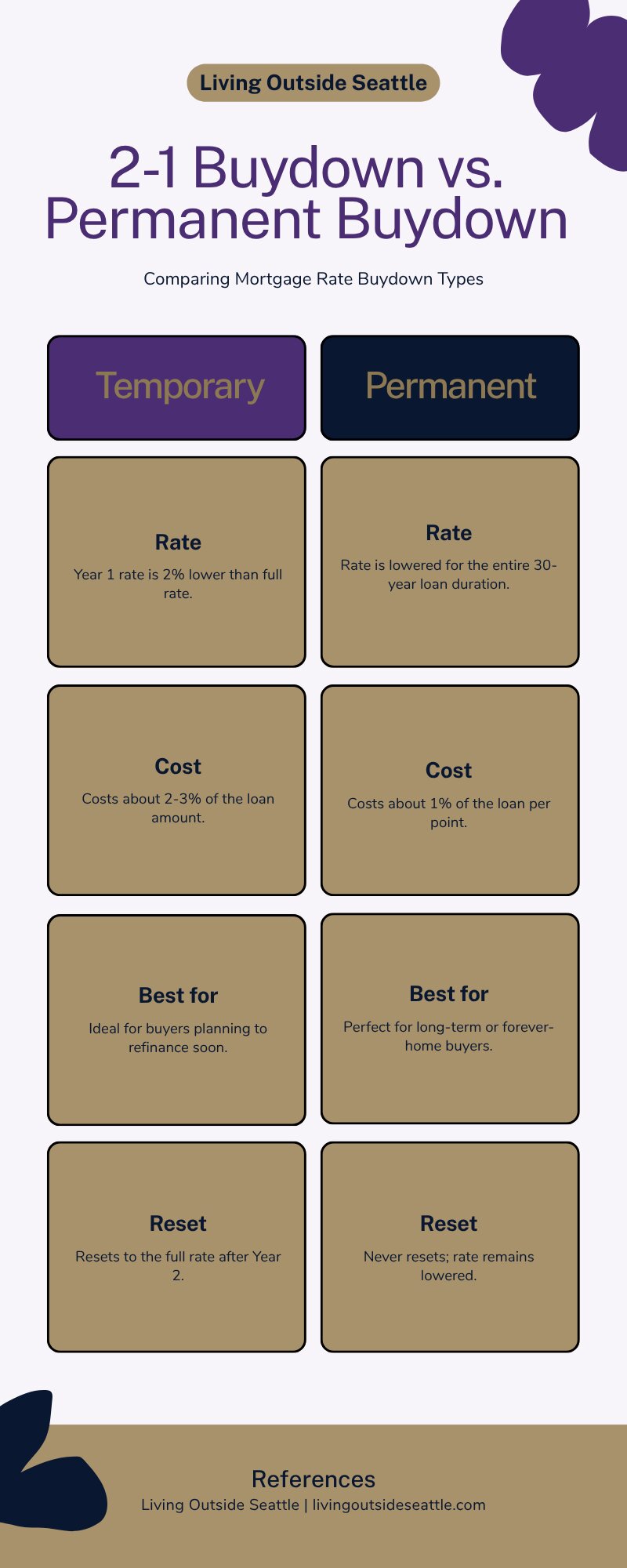

The Temporary Buydown: The 2-1 Explained

The most common temporary buydown is called a 2-1. The name tells you how it works. Your rate drops 2 percentage points in the first year, 1 point in the second year, then returns to the full rate for the rest of the loan.

Say your note rate is 6.5%. With a 2-1 buydown, you pay as if your rate were 4.5% in year one and 5.5% in year two. In year three you go back to paying 6.5% for the remaining 28 years. On a $400,000 loan, that first-year discount can cut your payment by around $400 a month.

The money to cover that gap gets parked in an escrow account at closing. Each month, that account chips in the difference between your full payment and your discounted payment. You do not get a bill for the buydown. It is already paid for and sitting there ready to go.

Temporary buydowns front-load the savings. Permanent points lower the rate for the whole loan.

The Permanent Buydown: Paying Points

A permanent buydown works through what lenders call discount points. You pay points upfront, and your rate goes down for the entire life of the loan. It never resets.

Each point costs 1% of your loan amount and usually lowers your rate by about 0.25%. On a $400,000 loan, one point costs $4,000 and might drop your rate from 6.37% to around 6.12%. That saves you roughly $60 a month, every month, for 30 years.

Here is the math that trips people up. Sixty dollars a month sounds small, but it adds up. The question is how long it takes to earn back the $4,000 you spent. In this example, that break-even point is about 67 months, or just over five and a half years. Stay in the home longer than that and the points pay for themselves. Sell or refinance sooner and you may not get your money back.

There is also a tax angle worth knowing. Discount points on a purchase loan are usually deductible in the year you pay them, under IRS rules. The cost of a temporary buydown is not. I am not a tax advisor, so check with yours, but it is one more reason permanent points can make sense for the right buyer.

Temporary vs. Permanent: Which One Is Right for You

The choice comes down to one question. How long do you plan to keep this loan?

Lean Temporary If You Might Refinance Soon

If you think you will refinance in the next two or three years because rates may fall, a temporary buydown often wins. You capture the biggest savings right away, during the exact years you have the loan, and you are not paying for a permanent rate cut you will not keep.

Many buyers in this market are betting on a refinance, and the data on how long people keep mortgages backs that up. The typical homeowner refinances or sells every five to seven years.

Lean Permanent If This Is the Forever Home

If this is your forever home and you expect rates to stay high, a permanent buydown saves more over time. You are buying down a rate you will actually live with for decades.

So what should you do? Run both numbers with your lender before you decide. Ask for the cost of a 2-1 buydown and the cost of one or two points, side by side, with the monthly payment and break-even for each. A good loan officer will have that ready in minutes. If they cannot produce it, that tells you something too.

The Local Angle: How King County Buyers Get Sellers to Pay

Here is where it gets interesting for buyers in Renton, Kent, Auburn, and the rest of South and East King County. You do not have to pay for a buydown yourself. You can ask the seller to.

This is called a seller concession, and it is common and negotiable in our market. Most loan programs let a seller cover somewhere between 2% and 6% of the purchase price toward your costs. In Washington, the average seller incentive runs around $12,000, or about 2% of the sale price. That is real money, and a buydown is one of the best ways to put it to work.

Think about what that means. Instead of asking a seller to drop the price by $12,000, you can ask them to put $12,000 toward a buydown. A price cut of $12,000 on a $600,000 home lowers your payment by maybe $70 a month. That same $12,000 spent on a 2-1 buydown can lower your year-one payment by $400 or more. Same money, very different result for your monthly budget. And remember that the payment is only part of the picture. Run the full total cost of homeownership in King County so the lower payment does not hide taxes, insurance, and upkeep.

The same concession dollars buy a much bigger monthly-payment drop as a buydown than as a price cut.

The key is to get your numbers first. Before you write the offer, have your lender calculate the precise buydown cost. Then you ask for that exact dollar amount. A specific, lender-verified request lands far better than a vague “can the seller help with my rate.” And bring a real pre-approval. Sellers take a concession request seriously from a buyer who is clearly qualified. Without one, the ask carries almost no weight.

What This Means for You as a Buyer

A rate buydown is not a gimmick. It is a legitimate way to make your payment work in a high-rate market. But it is only as good as the plan behind it.

Start by getting clear on your timeline. If a refinance is likely, lean temporary. If you are settling in for the long haul, run the permanent points math. Either way, get both quotes in writing before you fall in love with one option.

Then talk to your agent about who pays. In today’s King County market, a seller-paid buydown is often the single strongest negotiating move a buyer has. It can lower your payment more than a price cut for the same cost, and it gives sellers a reason to say yes. You just have to know how to ask, and you have to ask before you write the offer, not after.

Frequently Asked Questions

How much does a 2-1 buydown cost in King County?

A 2-1 buydown usually runs about 2% to 3% of your loan amount. On a $400,000 loan, that is roughly $8,000 to $12,000. Your lender can give you the exact figure based on your rate and loan size before you make an offer.

Can the seller pay for my rate buydown?

Yes. A seller-paid buydown is a common form of seller concession in Washington. Most loan programs allow sellers to contribute between 2% and 6% of the purchase price toward buydowns and closing costs. Confirm your program’s limit with your lender.

Is a buydown better than a lower purchase price?

Often, yes, for your monthly payment. The same dollar amount spent on a 2-1 buydown usually lowers your payment far more in the early years than an equal price cut. A price reduction helps your loan balance, while a buydown directly attacks the payment.

What happens after a temporary buydown ends?

Your payment goes up to the full note rate. With a 2-1 buydown, that happens in year three and stays there for the rest of the loan. This is why you should be comfortable with the full payment, not just the discounted one, before you commit.

Are mortgage points tax deductible?

Discount points on a purchase loan are generally deductible in the year you pay them, under IRS guidelines. The cost of a temporary buydown is not. Talk to a tax professional about your specific situation.

Should I do a buydown if rates might drop?

A temporary buydown can be a smart fit if you expect to refinance soon. You get the biggest savings in the years before you refinance, without paying for a permanent rate cut you would lose anyway. If a buydown still leaves the down payment feeling tight, take a look at King County down payment assistance programs before you rule yourself out.

Your guide to life outside Seattle.

253-350-0045 ·

greg@livingoutsideseattle.com ·

www.livingoutsideseattle.com