Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

How move-up sellers in King County use bridge loans to buy their next home before selling, and when a HELOC is the smarter play.

You found the next house. Bigger yard, better layout, the right school zone. There’s just one problem: your down payment is locked up in the home you’re still living in. This is the wall almost every move-up seller in King County hits, and a bridge loan is one of the main tools for getting over it.

I work with move-up sellers across Renton, Kent, Auburn, Covington, and Maple Valley, and this question comes up in almost every planning conversation: “How do I buy before I sell?” A bridge loan is often the first answer people hear. It can be a great tool. It can also be an expensive mistake if you use it in the wrong situation. Here’s how bridge loans actually work in Washington State, what they cost in 2026, and how to know if one fits your move.

How a Bridge Loan Works in Washington State

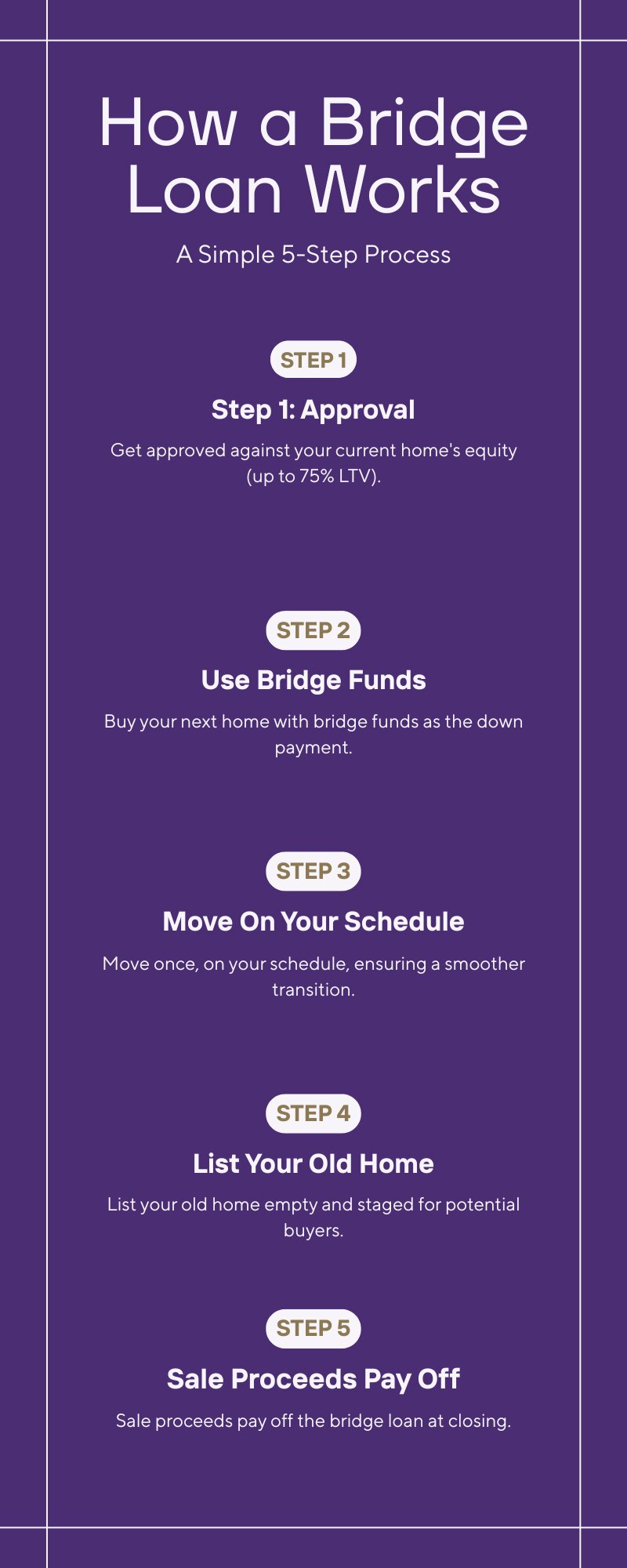

A bridge loan does exactly what the name says. It bridges the gap between buying your next home and selling your current one.

Here’s the typical sequence. You apply with a lender who writes bridge loans. The lender looks at the equity in your current home and approves a short-term loan against it, usually up to 70 to 75 percent of your home’s value minus what you still owe. You use that money as the down payment on your next home. You move once, on your schedule. Then you list your old home, and when it sells, the sale proceeds pay off the bridge loan in full.

Most residential bridge loans in Washington are interest-only. That matters because it keeps your monthly carrying cost down while you hold two properties. You’re not paying down principal. You’re buying time. The loan comes due either when your home sells or at the end of the term, whichever comes first. In my market, that exposure window is usually short. Well-priced homes in South King County have been selling in 6 to 14 days, so most bridge borrowers here are paying interest for two to four months, not a year.

The full bridge loan cycle. In fast South King County segments, most borrowers reach payoff in two to four months.

What a Bridge Loan Costs in 2026

This is where you need to go in with clear eyes. Bridge money is more expensive than mortgage money.

In 2026, standard 30-year mortgage rates have been sitting in the mid-6 percent range. Residential bridge loans from banks and credit unions are typically running about 8 to 10 percent. Private and hard-money bridge lenders charge more, often 9 to 12 percent. On top of the rate, most lenders charge origination points, commonly 1.5 to 2.5 percent of the loan amount, plus normal closing costs.

Let’s make that real. Say you borrow $200,000 against your Kent home to put down on a house in Covington. At 9 percent interest-only, that’s $1,500 a month. If your Kent home sells in three months, you’ve paid $4,500 in interest plus roughly $3,000 to $5,000 in points and fees. Call it $8,000 to $9,500 total for the ability to buy first, move once, and sell an empty, staged home at full strength.

Is that worth it? For a lot of my sellers, yes. An empty home shows better and often sells for more than the cost of the bridge. You also skip the misery of living in a staged house with kids and dogs while strangers tour it. But the math only works if your home actually sells inside the window. That’s the whole game with a bridge loan.

Bridge Loan vs. HELOC: Which One Fits?

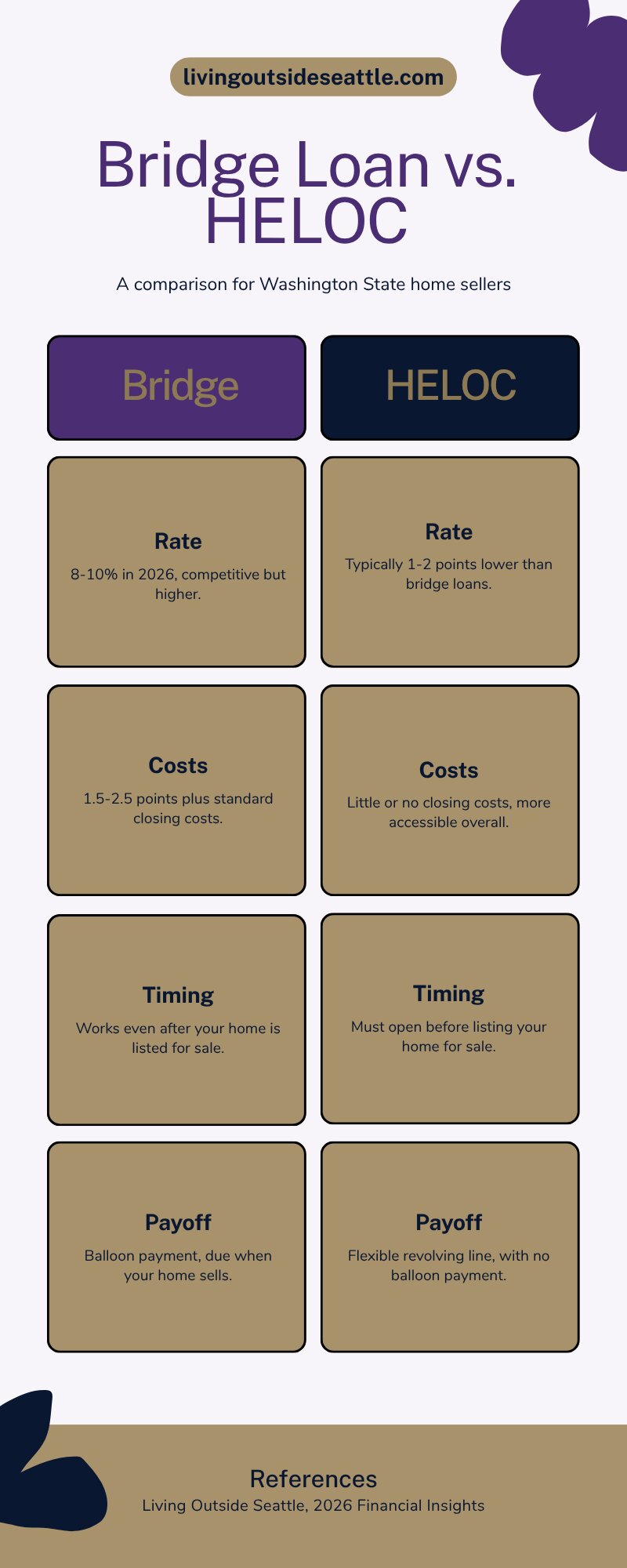

A home equity line of credit is the other common way to unlock your equity, and for some sellers it beats a bridge loan outright.

A HELOC is cheaper. Rates in 2026 are generally running a point or two below bridge loan rates, and most HELOCs have little or no closing costs. It’s also flexible. You draw what you need, when you need it, and there’s no balloon date forcing a payoff.

So why doesn’t everyone just use a HELOC? Timing. Here’s the trap I warn sellers about constantly: lenders will not open a HELOC on a home that’s already listed for sale, and many want it seasoned for months before you draw on it. A HELOC is a tool you set up six months to a year before your move, while you’re still just thinking about it. Once the sign is in the yard, that door is closed, and a bridge loan becomes the realistic option.

The other difference is qualification. With either tool, the lender needs to see you can carry the payments. Some bridge lenders will soften the math if your current home is already under contract. If you want to understand exactly how lenders count your income and debts, I broke that down in my guide to how mortgage qualification works in Washington State.

The deciding factor is usually timing: a HELOC must be opened before you list, a bridge loan works after.

Who Offers Bridge Loans in Washington State

Here’s something that surprises people: most big national banks got out of the consumer bridge loan business years ago. You won’t find one at most major retail banks.

In Washington, bridge loans come from three places. First, regional banks and credit unions. Several Washington-based institutions still write true bridge loans for their members, and this is usually the cheapest version of the product. Second, local mortgage companies. A handful of Puget Sound area lenders offer bridge programs designed specifically for buy-before-you-sell moves. Third, the newer “buy before you sell” programs. Seattle-based Flyhomes has rebuilt its whole business around this model, and national players like HomeLight offer versions of it here too. These programs package equity access, a non-contingent offer, and the sale of your old home into one product. Ask your real estate agent if they know a lender that offers this type of program.

Those programs can be slick, but read the fee structure carefully. Between program fees, loan costs, and pricing requirements on your departing home, the all-in cost can run well past what a straight bridge loan from a credit union costs. Convenience has a price tag. Sometimes it’s worth paying. Just know what it is before you sign.

The Local Angle: Why Bridge Loans Work Differently in King County

Bridge loans are unusually well-suited to South King County right now, and the reason is speed plus equity.

Start with equity. Homeowners who bought in Renton, Kent, or Auburn even six or seven years ago are sitting on six-figure equity positions. Kent’s median sale price has been running around $732,500 and Renton’s spring median hit $859,000. If you bought your Kent home for $450,000 in 2019, you likely have $300,000 or more in equity doing nothing. A bridge loan turns that trapped equity into a down payment without forcing you to sell first.

Now speed. The bridge loan’s biggest risk is a slow sale, and well-priced South King County homes simply aren’t selling slowly. Kent has been averaging about 8 days on market and Renton homes have been moving in about 6 days in spring. That means a typical bridge borrower here carries the loan for a couple of months, not a year. Compare that to a slower sub-market, like some Eastside condo segments, where months of supply are higher and a bridge gets riskier. Where your current home sits matters more than any national average.

One move, on your schedule. That convenience is what a bridge loan actually buys.

What This Means for You as a Move-Up Seller

Here’s the decision framework I walk sellers through.

A bridge loan makes sense when three things are true. You have strong equity, ideally enough to borrow your full down payment at 75 percent loan-to-value or less. Your current home sits in a fast-moving segment and will be priced to sell, not priced on hope. And you’ve found, or are about to find, a next home worth moving fast on. When all three line up, paying $8,000 to $12,000 for a clean, one-move transition is often money well spent.

A HELOC makes more sense when your move is six months or more away and you have the discipline to set it up early. Open it while your home is unlisted, let it sit at zero balance, then draw on it when you find the right house. Cheapest equity access there is.

And sometimes the answer is neither. If your equity is thinner or the numbers feel tight, a well-structured contingent offer can still win in the right situation. I wrote a full guide on how to write a contingent offer that sellers will accept in King County, and it pairs with this post. Whichever route you take, the first step is the same: know what your current home is worth and how fast it will sell. That’s a pricing question, and it’s the one I can answer with real data.

FAQ: Bridge Loans in Washington State

How long do you have to pay back a bridge loan?

Most residential bridge loans in Washington run 6 to 12 months, and the loan is paid off automatically from your sale proceeds at closing. In fast markets like Renton and Kent, most borrowers pay theirs off within two to four months. Most lenders charge no penalty for early payoff.

How much does a bridge loan cost in 2026?

Expect interest rates around 8 to 10 percent from banks and credit unions, or 9 to 12 percent from private lenders, plus origination points of roughly 1.5 to 2.5 percent of the loan amount. On a $200,000 bridge held for three months, total cost typically lands between $8,000 and $10,000.

Are bridge loans hard to get?

They’re more specialized than a standard mortgage, not necessarily harder. Lenders generally want a credit score of about 680 or better, combined loan-to-value of 75 percent or less on your current home, and a believable exit plan. The bigger challenge is finding a lender, since most national banks no longer offer them.

Can I get a bridge loan if my house is already on the market?

Usually yes, and this is a key advantage over a HELOC. Lenders won’t open a home equity line on a listed property, but bridge lenders expect your home to be listed or about to be. Some even offer better terms once you’re under contract.

Is a bridge loan better than a contingent offer?

A bridge loan makes your offer stronger because it removes the home-sale contingency, which matters in competitive segments of King County. A contingent offer costs nothing but is easier for a seller to pass over. If the home you want has multiple offers, the bridge-backed offer usually wins.

Bridge loans aren’t exotic anymore. In a market where most move-up sellers are equity-rich and good homes still move in days, buying before you sell is a real strategy, not a luxury. The key is sizing the loan against an honest number for your current home and a realistic timeline for your area.

Your guide to life outside Seattle.

253-350-0045 ·

greg@livingoutsideseattle.com ·

www.livingoutsideseattle.com