Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

How Move-Up Buyers in King County Use Home Equity Before They Sell

You own a home in Sammamish or Issaquah. You’re thinking about buying something else, a different size, different location, or just a fresh start. But you don’t want to sell first and move into a rental while you shop.

The question most move-up buyers hit at this point: how do I buy my next home without selling first? The main tools are a bridge loan, a HELOC, or a contingency offer. Each has real advantages and real costs. Here’s how they work in today’s King County market.

Why the “Sell First, Buy Second” Sequence Feels Risky

The instinct to avoid selling before buying is reasonable. If you sell your Sammamish home first, you have certainty about your proceeds but you’re now a buyer competing without your equity deployed. You’re likely renting month-to-month or negotiating a rent-back from your buyer while you search. In a market where the right home still sells in 7 days, searching without a home to sell feels safer.

The problem with this plan is that it often leads to rushed purchases or extended rental periods. And in King County, extended rentals at $2,400 to $3,500 per month are expensive holding patterns.

There are three tools that solve the sequencing problem. Each works differently.

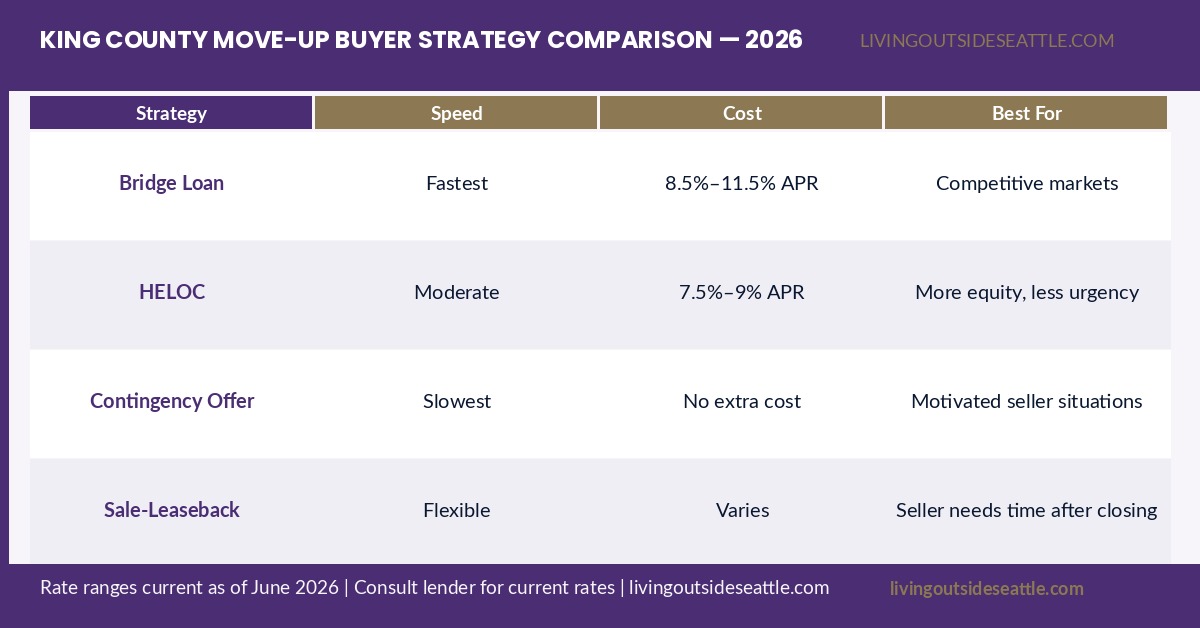

Option 1: Bridge Loan

A bridge loan is a short-term loan secured by your current home that gives you the cash to close on your next purchase before your current home sells.

How it works: a lender extends you a loan of 70% to 80% of your current home’s equity, short-term (typically 6 to 12 months). You use those funds as the down payment on your next home. You carry both loans simultaneously until your current home sells. When it does, you pay off the bridge loan from the proceeds.

Bridge loans right now are running 8.5% to 11.5% APR, significantly higher than the primary mortgage rate. On a $400,000 bridge loan at 9%, you’re looking at roughly $3,000 per month in interest-only payments during the bridge period.

The bridge loan works best when you have substantial equity in your current home, your current home will sell quickly (which in Sammamish or Renton at 7-day DOM is likely for a correctly priced property), and the cost of carrying two loans for 60 to 90 days is manageable.

The risk: if your current home takes longer to sell than expected, the bridge loan interest accumulates and the psychological pressure to accept a lower offer on your current home grows.

Option 2: Home Equity Line of Credit (HELOC)

A HELOC is a revolving line of credit secured by your current home’s equity. Unlike a bridge loan, you draw only what you need and pay interest only on what you’ve borrowed.

Current HELOC rates in Washington State are running approximately 7.5% to 9%, tied to the Prime Rate plus a margin. On a $300,000 draw for a down payment, that’s $1,875 to $2,250 per month in interest.

The HELOC has one key advantage over a bridge loan: you can often put it in place before you list your current home, giving you a standing line of credit that’s ready to deploy when you find the right property. Banks become reluctant to approve a HELOC once your current home is actively listed for sale, so the sequence matters. A HELOC typically takes 30 to 45 days to establish.

The HELOC also lets you be selective about how much you draw. If you can make the new purchase work with a smaller down payment and a slightly higher rate on the new mortgage, you can draw less from the HELOC and reduce your carrying cost.

The risk: your current home serves as collateral for both the primary mortgage and the HELOC. If the home doesn’t sell within 6 months, some HELOC agreements allow the lender to freeze or reduce the line.

Option 3: Contingency Offer

A contingency offer on your new home makes your purchase conditional on the sale of your current home. If your current home doesn’t sell within a specified period (typically 30 to 60 days), the contingency can be triggered and you can back out of the purchase.

This approach sounds simpler than a bridge loan or HELOC because it doesn’t involve additional financing. The significant downside in King County’s market is that sellers of desirable properties often won’t accept contingency offers, or they’ll counter with a kick-out clause that allows them to continue marketing the home and require you to remove the contingency or forfeit the deal within 24 to 72 hours if another offer comes in.

In a market where the right home sells in 7 days, a contingency offer puts you in a weaker negotiating position. Sellers prefer the certainty of a non-contingent buyer.

Contingency offers are most viable in softer segments: Issaquah above $1.5M, Sammamish right now, or the condo market broadly, where sellers have been sitting 20 or more days and have less leverage to decline. In these segments, a well-structured contingency offer from a qualified buyer is real currency.

The Sammamish and Issaquah Context

Both cities are in a price-correcting environment. Sammamish down 6.6% YoY, Issaquah down 14.3%, with months supply at 4.3 and 4.5 respectively. That combination creates an interesting dynamic for move-up buyers.

If you own a Sammamish or Issaquah home and you’re buying something different, you’re selling into a softening market and buying into one too, depending on your target. The correction that has reduced your current home’s value may also have reduced what you’re buying into.

This is where the financial modeling matters. Running the actual numbers on what your current home sells for versus what your next home costs, and how the bridge, HELOC, or contingency path affects the total, is what tells you which option makes sense.

Frequently Asked Questions

Can I use a HELOC to buy a home before I sell in King County?

Yes, but timing matters. You need to apply for and open the HELOC before you list your current home for sale. Most lenders will freeze or close a HELOC once the property securing it is actively listed. A HELOC typically takes 30 to 45 days to establish, so start the application well before you’re ready to list. HELOC rates in Washington are running approximately 7.5% to 9% currently.

What are current bridge loan rates in Seattle and King County?

Bridge loans in the Seattle area are running 8.5% to 11.5% APR as of June 2026, significantly higher than primary mortgage rates. On a $400,000 bridge loan, expect $2,800 to $3,800 per month in interest-only payments. The short loan term (typically 6 to 12 months) limits your total interest exposure, but the rate is the tradeoff for speed and flexibility.

Will sellers in Sammamish and Issaquah accept contingency offers right now?

More than they would have 18 months ago. With months supply at 4.3 in Sammamish and 4.5 in Issaquah, sellers who’ve been on the market 20+ days have less leverage to decline a well-qualified buyer with a contingency. Many will counter with a kick-out clause allowing them to keep marketing and requiring you to remove the contingency within 24 to 72 hours if another offer comes in.

What is the DTI limit for carrying two mortgages at the same time?

Most conventional lenders require a debt-to-income ratio of 43% or below accounting for both the existing mortgage and the new one simultaneously. This is the single biggest qualification hurdle for move-up buyers using a bridge loan or buying before selling. Work with your lender to model both payments before you make any offer.

Want to Model Your Specific Situation?

The move-up decision comes down to numbers: what your current home is worth, what your target costs, which financing bridge works best, and what your net equity position looks like on the other side. That’s a conversation worth having before you list anything.

Your guide to life outside Seattle.

253-350-0045 ·

greg@livingoutsideseattle.com ·

www.livingoutsideseattle.com